{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

San Diego home price soar, salaries lag

Hot competition for a slice of the American pie

In Grant Hill, “there’s still some affordability.” This house is listed at $475,000.

The median price for a single-family home in San Diego County at the end of 2016’s first quarter, according to the California Association of Realtors, stood at just over $554,000.

Assuming you’ve got access to a 20 percent down payment, sterling credit to qualify for a top-tier loan, and minimal other debt, it would require a household income in excess of $110,000 to afford such a property.

San Diego’s median income, meanFGrabt while, sits at $63,400 for a family of four. For potential homebuyers in this income range, the city’s own website recommends a purchase price no higher than $225,000. Seventy two percent of San Diegans, then, find themselves priced out of affordable ownership. Nationwide, the percentage of individuals who own the home they reside in is at its lowest point in more than 40 years.

Still, recent polling indicates more than four in five Americans believes owning a home is a good investment, ranking homeownership as an even more crucial investment than maintaining a retirement account.

Where, then, can aspirational homeowners turn to find their piece of the American Dream? Does such a place even exist in San Diego proper? Or within county lines, for that matter? I recently set off to find out.

“Clairemont is a good spot for families. Grant Hill, there’s still some affordability in the City Heights neighborhood, but it’s appreciating so fast,” opines local real estate agent Melissa Costa as we spend a Saturday afternoon nibbling pretzel bits and sipping craft beer in a Point Loma eatery near her home. “South Park, Normal Heights, those were great starter neighborhoods a few years ago that I think have now passed beyond the range of average buyer affordability. Golden Hill is getting there, too.”

Head east, advises agent Melissa Costa.

These seem promising — definitive neighborhoods within city limits where Costa says she’s recently worked with first-time buyers. I ask what, in her clients’ eyes, makes a neighborhood an ideal fit.

“I think walkable access to parks and restaurants, especially if you feel safe walking at night, makes a lot of the neighborhood,” says Costa. She’s also a big fan of renovating the existing Craftsman and adobe-style bungalows that line many of San Diego’s more established blocks. “People are revitalizing instead of tearing down these fantastic older homes, and I think that’s something that helps.”

But these urban traits — walkability, access to fine dining and nightlife, and historic preservation are ones that resonate mostly with younger, childless singles and couples. For the first-time family buyer, the situation is different.

“With family buyers, schools are by far the number-one thing they’re looking for. But they’re also interested in quieter neighborhoods with slower traffic, cul-de-sacs, almost a Wisteria Lane kind of feel,” Costa continues, referring to the supposed utopian namesake street that formed the setting of Desperate Housewives, which so far as I can glean from my wife’s obsession with the show was a prime-time soap opera about adultery, backstabbing gossip, and violence whose picturesque suburban landscape apparently made up for all the neighborhood’s drawbacks.

Still, I get what she means — a quiet neighborhood where kids can set up a basketball hoop or ride bikes and skateboards without traffic whizzing past, where the school system receives good reviews, and reported crime rates are relatively low.

Schools, in particular, are among the top concerns cited by a host of both buyers and real estate agents when selecting a community. A veritable smorgasbord of websites, chief among them GreatSchools.org, publish rankings of the most and least desirable schools and compile data on performance of both districts and individual sites for parents to pore over. They largely list schools in the north-of-I-8 communities of Rancho Bernardo and Scripps Ranch as top-ranking destinations, though with median home prices ranging from $665,000 to $929,000, these are well outside the realm of average affordability.

Costa explains that these buyers will sacrifice proximity to amenities and accept that they won’t be leaving the house on foot in exchange for lower traffic levels and stronger school rankings. Many leave the city proper to find what they’re looking for at an affordable price.

“There’s definitely a certain demographic that would benefit from going east — they’re not as concerned about proximity to the beach, they’re not looking for a trendy neighborhood necessarily. And there’s much more affordable property in Lemon Grove, Spring Valley, parts of La Mesa, and El Cajon, even Santee,” says Costa, though in my nearly two decades selling real estate I’ve heard the same desires echoed by buyers heading for North County, South Bay (eastern Chula Vista, in particular), and some even moving to southern Riverside County — Temecula, Murrieta, and surrounding cities— in search of the same suburban bliss.

Median price in Chula Vista is $425,000

We’ve established some baseline traits for what makes a neighborhood desirable. But we still haven’t established a connection with what makes those same neighborhoods affordable, at least to those of us who’d like to occupy homes there. This is where the discussion gets a bit wonkish.

Let’s take a look at some of the common first-time buyer neighborhoods Costa suggests, with numbers provided by Core Logic for average home sale prices as of June 2016.

First off, we’re going to have to sadly conclude that, unless you’re willing to travel to the far extremes of the county such as Boulevard (about 68 miles from downtown San Diego; average recent sales price $252,000) or Borrego Springs (86 miles; $188,000) and spend considerable hours and gas money in the name of ownership, the comfortable definition of affordability is going to need to be stretched a bit.

One way the government does this is by including households making up to 120 percent of an area’s median income (let’s call that $76,080/year) in the pool of buyers eligible for “affordable” housing. Another is the FHA loan-guarantee program, which allows buyers to put as little as 3.5 percent down when buying a home, as most prospective first-time buyers don’t have tens of thousands of cash on hand.

As a hedge against risk based on how little the buyer is investing as compared to a traditional buyer with 20 percent cash on hand, FHA charges both an upfront “mortgage insurance premium” of nearly 2 percent of the loan amount that’s tacked on to the total loan amount as well as “private mortgage insurance” of 0.85 percent, essentially added to the interest rate. These extra charges go into a fund that guarantees lenders they won’t have to absorb the bulk of the loss if an FHA loan goes bad.

Location, location, location

The difference in monthly payments buyers must be able to weather is substantial. Let’s take a $400,000 home as an example. For a conventional buyer with 20 percent down and good credit, the monthly payment would be roughly $1931; for an FHA buyer it’s closer to $2354.

As of late July, the average going rate on an FHA loan was around 3.0 percent, effectively 3.85 percent when considering the mortgage insurance on top of the nominal interest rate. What does that buy?

Not a whole lot, unfortunately. Keeping within federal guidelines for an affordable home, a family earning just over $76,000 could buy a house for $320,000 at $1881/month (including property taxes and fire insurance) — that pretty much prices out anything within an hour’s drive of the city core.

But wait — a few more tricks with arithmetic might bring us closer to finding an affordable home for a slightly above-average buyer. For prospective borrowers with exceptional credit who are willing to put it all on the line to realize the dream of home ownership, loans are available allowing a buyer to spend up to 45 percent of their pre-tax income on fixed debts including the cost of the home and any other bills including car payments, student loans, and credit card debt.

Keeping the same numbers as before, our 120-percent-better-than-the-median buyer can now spend up to $2849 per month on housing, provided he or she has no other debts whatsoever — that’s good for a purchase price up to $494,000, and suddenly the map of prospective neighborhoods comes to life!

Median price in the Oak Park/Encanto area is $395,000

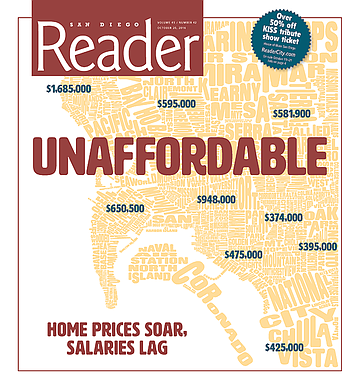

Clairemont ($595,000 median) is still a stretch, though City Heights ($374,000) and Encanto ($395,000) are in. Hillcrest ($948,000) and North Park ($576,000) are still rarefied air, but La Mesa ($487,000-572,000), Lakeside ($458,000), and Lemon Grove ($405,000) are in the picture. Poway ($697,000) and San Carlos ($600,000) are out, but National City ($365,000) and Spring Valley ($420,000-459,000) remain contenders. Going north and south, Vista (as low as $428,000), Escondido (starting at $425,000) and western Chula Vista (from $425,000 up) are players.

It turns out Costa has a pretty good handle on what buyers say they’re looking for in a place to call home.

“Not being on a main, busy street was huge for us — somewhere where we could feel safe with our kids playing out front, and if I had to run inside for a second it’s not like I’d feel scared of something happening to my child,” says Anna Carel, who along with her husband David and two young children, moved into a townhome in Lakeside last May.

“It’s funny, everyone who comes to visit us remarks how they never even knew this neighborhood existed.”

Indeed, the cul-de-sacs off Saddle Ridge Road, each occupied by a handful of twin-homes (treated like a single-family house but with one shared wall), is easy to miss. Flanked on the north by a newer housing tract and the south by mid-century ranch homes, the ’70s-era development is dotted by eucalyptus and palms, with mature oak trees offering patches of shade in a handful of communal grass lawns dotting the complex. Go a quarter-mile in about any direction and you’ll find nothing but open space, hilly patches of southeastern Lakeside as yet untouched by the ever-charging force of suburban development.

For the Carels, moving back home to East County where they grew up from Oceanside (where the family had temporarily relocated to be closer to David’s job at the time) was a bumpy road.

“We’d been working on trying to buy a house for two or three years, saving and getting our credit in order. We’d have actually done it a lot sooner, we just weren’t quite there yet,” says David. The couple’s home, purchased for a little over $330,000 (though homeowners’ association fees drive the cost up above that of a similarly priced single-family home), was made possible through an FHA-guaranteed loan with its mandatory monthly mortgage insurance premium tacked on to the regular payment.

“The older I get the more it becomes clear that you’re only really worth what your credit score and your bank account says about you to a lender, how you look on paper,” adds Anna, 29, who is nonetheless thrilled to be a homeowner. “The tax write-offs and financial benefits are huge, so is knowing that you’re investing in something for the future. “It’s something that definitely makes you feel like you’ve graduated into a more responsible phase of life.”

Aside from the quiet location, I ask what else influenced the Carels’ decision when they were home shopping, and what other parts of town might have appealed to them. Quality of school district is the first thing that comes to mind, and it does so in a big way.

“I did a lot of searching around on different websites, asking friends who were parents at different schools, looking for our best options. But obviously the better the school district, the more expensive the houses are around it,” Anna laments. “For instance, Poway has amazing schools, among the tops in California, but real estate there was entirely out of reach financially. I feel comfortable that we’ve made a good choice with where we are, though — the schools here are rated higher than a lot of other areas in our price range.”

“We wanted to get back to where our friends and family were, and where we could plan on staying for some time without worrying about moving our kids from school to school. That was another big target, to get into a place before our son started kindergarten, so he could stay with the same group of friends throughout his time there,” David adds, though the long process of improving the couple’s credit and amassing a down payment means that first grade, not kindergarten, will be the younger David’s introduction to the school system where the family hopes he’ll stay through high school.

“We looked in Santee, El Cajon, La Mesa, Mira Mesa, Poway, Tierrasanta…” David tells me, counting off neighborhoods both in San Diego and the suburbs the family had been interested in before Anna jumps in again.

“A lot of those areas were kind of, like...we went and looked there because of the school districts, then right away we figured out we weren’t going to be able to really find a viable option financially.”

Not only were high prices a deterrent, poorly ranked education was just as likely to take a neighborhood out of the running.

“Schools were a huge obstacle. We’d find a great house at the right price, but the local schools wouldn’t be rated so well, so that one would be out,” David admits. “There were a lot of houses I wanted to buy but I didn’t want to enroll my kids in the local school system.”

Despite the arduous process, the Carels are convinced they made the right choice by electing to buy.

“Cosmetic things — deciding what to put where, what color paint to use, what you want to do with your yard — that’s really the most exciting part to me,” says Anna.

“I definitely think we made the right choice in becoming homeowners as opposed to remaining renters,” David concludes.

The once-again-high-flying housing market, though, doesn’t seem as rosy to everyone in town.

The corner of University and Fairmount Avenues in the heart of City Heights paints a picture of rebirth that seems to represent urban renaissance idealized. Two corners are occupied by newly built mid-rise office and mixed-use residential/commercial structures. A third is home to a new shopping plaza, the colorful paint still crisp on the façades of Denny’s, McDonald’s, and Panda Express, shade trees planted along the parkways are still years from maturity.

The fourth corner, housing a decades-old strip mall that’s home to a discount shoe store and combination donut shop/Chinese restaurant, may be more indicative of life on the Boulevard, a life that at least some residents will mourn the loss of.

Walking down Polk Avenue, just a block north of University, it feels like an entirely different world. The sounds of reggae, horn-heavy norteño ballads, and mid-morning television talk shows provides the narrow one-way street’s soundtrack. An old mattress slumps against the side of an apartment building, threatening to fold over itself and flop onto the sidewalk.

Properties in the neighborhood are a mix of early-1900s Craftsman-style bungalows and Huffman six-packs, boxy, characterless apartment buildings stuffed onto former single-family lots in the late 1970s and early 1980s with a push from developer Ray Huffman and then-mayor Pete Wilson as a proposed solution to conquering suburban sprawl in the face of a population influx. The landscaping is barren in some spots, mature or overgrown in others. Many front yards have been given over to parking.

Working people have been priced out of Rich Kacmar and Anna Daniels’s City Heights neighborhood.

Amid this scene stands the cozy two-bedroom abode of retired librarians–turned–community activists Anna Daniels and Rich Kacmar. A canopy of climbing roses and vines overtaking black bamboo surround the cottage. A pink trumpet tree grows near the colorfully painted wooden fence out front. Despite their relatively stable footing today, Daniels worries that not only is ownership getting farther out of reach, the simple matter of remaining housed at all in the face of another real estate spike poses a real challenge to some of her neighbors.

“The house was, at the time and relatively speaking, affordable,” Daniels says, speaking of when she and her husband first purchased their home on 45th Street in 1986. I ask her, if she were in the same position today as 30 years ago, would she be considering moving into the same neighborhood?

“Oh, heavens no. This has been a working-class neighborhood since its inception in the ’20s, and while I’d say it’s still a working-class neighborhood the people today have to work a lot harder. I’d probably write off the possibility of buying a house. Even after 30 years my husband’s and my salary never increased at the same rate as the price of real estate in San Diego, particularly the inner-city communities. The reality is this house, that we paid $81,000 for, was a stretch — it would be absolutely, completely out of reach at $350,000 today.”

An estimate from Zillow, a popular automated home-valuation system, estimates the current value of the couple’s home closer to $412,000.

“The big issue here is affordable housing, with a significant ancillary issue being livable wages. You have to remember that City Heights is one of the poorest communities in San Diego — people on my block have about a $3000 monthly household income,” Daniels tells me as we sit on her porch, occasionally interrupted by a passing car or groups of enthusiastically loud chatters walking by. “I talk to people and I’m amazed to hear that they’re paying over a thousand dollars a month for a one-bedroom apartment in City Heights. Is that affordable? I think it’s a relative term; historically, families have been able to make the rent somehow, though it’s usually meant they’re having to double up.”

She mourns the fact that efforts to prop up affordability are often overshadowed by a push to gentrify urban neighborhoods and celebrate newfound affluence while ignoring residents pushed further to the fringe.

“When we moved here, there was a 16-unit apartment complex across the street. They were turned into condos right before the economy tanked. Prior to that, those units were filled with Mexican-Americans who supported a whole economy on the street — everyone from a green grocer to a door-to-door egg man. And these people were displaced when the apartments were turned into condominiums, which the developer tried to sell for around $290,000. The prices kept dropping, though, until the units were eventually rented back out. So we took 16 families who were living in City Heights and displaced them with new renters able to afford higher rents. I’ve kept up with a lot of those families, and a few of them found other neighborhoods nearby, but a lot ended up in El Cajon. And for people without cars who are commuting to work, that adds a lot of extra time to their days.”

Daniels is interested in exploring the possibility of using community-based nonprofit organizations to acquire and maintain a housing stock that’s attainable for lower income families, though she says most of the focus to date is on private investment, where builders are encouraged through subsidies and incentives to maintain a certain percentage of their development as “affordable” housing.

Under the California Redevelopment Act, which governed redevelopment agencies until these bodies were dissolved in 2012, for example, developers had to make at least 15 percent of the units developed in a residential project affordable to people of “low-to-moderate-income households,” defined as those making up to 120 percent of the area’s median income, or $76,080 per year in San Diego.

“When you’re looking at affordability, my sense is that, after having participated in all sorts of community forums and planning committees, turning over the problem to the private sector is not an answer to our crisis. And affordable housing certainly is a crisis,” Daniels warns. “The path that we’ve been following hasn’t been able to provide an adequate number of units.”

Median price in University Heights is $550,000

Licensed real estate agents are bombarded with dozens of promotional emails from other agents daily. A sampling I’ve received: there’s a 676-square-foot Craftsman on the border of North Park and City Heights going for $420,000; a slightly larger two-bedroom, one-bath Spanish adobe house in Kensington for $609,000; a cozy three-bedroom single-story in suburban Rancho Peñasquitos boasting access to the coveted Poway schools is only $580,000. A 4S Ranch “executive home,” really just a nondescript tract home surrounded by hundreds more like it but with considerably more square footage than the others on this list, is priced at $1,150,000.

Despite Daniels’s bleak assessment of the current state of real estate, there are still plenty of hopeful buyers scouring the city for a place they hope to call home. One of them is Angela Clapp, a nurse manager of a surgical department at Scripps Memorial Hospital La Jolla who’s been placing offers since early May.

House hounting “has been tough” for Angela Clapp.

I meet Clapp when her agent leaves town for a few weeks on vacation. We get to know one another a bit when I step in to show her a few condos in case an irresistible deal pops up. She agrees to help me understand her perspective as a first-time, single buyer searching for a home in San Diego’s urban landscape.

“I’ve been shopping for about three and a half months,” Clapp tells me. “Now that I’ve narrowed it down I’m looking mainly around the PB and Bay Park neighborhoods. When I started, I was looking everywhere — Clairemont, North Park, just seeing what was out there. But for me and my lifestyle, I wanted to be closer to the bay. I like to kayak, so having access to recreation is what I’m looking for. Can you just walk out the door and go grab a cup of coffee? Is there a store to walk to? That’s a big appeal to me. That’s a big selling point to me, accessibility of the community.”

Clapp, though, has a problem common to first-time buyers who want to stay close to the urban core and its attendant amenities. Without the significant lump of cash that usually comes from selling another property that’s built up equity over the years, she needs an FHA loan that will let her borrow all but 3.5 percent of the purchase price. And she’s got a spending cap of $400,000, which means she’s almost definitely looking for a condo.

During the last market crash, FHA took two actions that severely limited the available supply of condominium housing eligible for financing. First, they eliminated the “spot approval” process, where a single unit within a larger development could be considered for loan approval, given that the homeowners’ association books showed sufficient cash reserves to cover anticipated repairs and that the building was primarily occupied by the owners of the units. Second, they cancelled the blanket approvals that many complexes had qualified for, which allowed FHA buyers to purchase within a development without jumping through the extra spot-approval hoops. Even half a decade later, few associations have applied for reapproval of their buildings.

“It’s been tough,” Clapp sighs. “It’s certainly been difficult as an FHA buyer when it comes to condos. I’m looking at potential avenues to possibly go conventional. After the market crashed, FHA changed so that there’s so much more that needs to be done to get a condo FHA-approved, so I’ve definitely hit a roadblock.”

I should mention here that many conventional, non-government-backed lenders offer “FHA lookalike” loans that, like FHA loans, allow a buyer to borrow 95 to 97 percent of the money needed to buy a home. These could open the door to condo ownership for some first-timers, but much more stringent credit-score requirements and higher interest rates place them out of reach for many borrowers, Clapp included.

“There have been a couple I’ve found that are approved, but unfortunately I’ve been outbid on the offers I’ve put in,” Clapp says of the few chances she’s had to get in on a condo that fit her loan requirements. “When I’ve put bids in, there have always been other offers and I’ve had to deal with counter offers. Anyone looking to buy should anticipate competition — it’s not going to happen quickly, and when the time is right it’s right.”

She realizes, though, that wherever she ends up probably won’t meet the definition of a “forever” home, and that’s okay.

“For this phase of my life, this is what fits. Whether I’m there for five years, ten years — it’s not a lifelong place. I’d like to keep the place and rent it, even if I don’t live there. I definitely still want to be in San Diego a decade from now. I’m 31; in five or ten years maybe I have a family, I might outgrow a two-bedroom condo.”

Despite months of setbacks, Clapp remains optimistic and keeps in mind the personal motivations that drive her, along with hordes of other hopeful buyers she’s competing with for a slice of the pie, to keep searching.

“I have friends who’ve recently bought homes, and they’re very happy. So I thought, why not me too? I want to be able to have somewhere to call home, and that’s somewhere to share with people that matter to you. That’s my incentive, my push.”

Here's something you might be interested in.

San Diego home price soar, salaries lag

Hot competition for a slice of the American pie

San Diego home price soar, salaries lag

Hot competition for a slice of the American pie

In Grant Hill, “there’s still some affordability.” This house is listed at $475,000.

The median price for a single-family home in San Diego County at the end of 2016’s first quarter, according to the California Association of Realtors, stood at just over $554,000.

Assuming you’ve got access to a 20 percent down payment, sterling credit to qualify for a top-tier loan, and minimal other debt, it would require a household income in excess of $110,000 to afford such a property.

San Diego’s median income, meanFGrabt while, sits at $63,400 for a family of four. For potential homebuyers in this income range, the city’s own website recommends a purchase price no higher than $225,000. Seventy two percent of San Diegans, then, find themselves priced out of affordable ownership. Nationwide, the percentage of individuals who own the home they reside in is at its lowest point in more than 40 years.

Still, recent polling indicates more than four in five Americans believes owning a home is a good investment, ranking homeownership as an even more crucial investment than maintaining a retirement account.

Where, then, can aspirational homeowners turn to find their piece of the American Dream? Does such a place even exist in San Diego proper? Or within county lines, for that matter? I recently set off to find out.

“Clairemont is a good spot for families. Grant Hill, there’s still some affordability in the City Heights neighborhood, but it’s appreciating so fast,” opines local real estate agent Melissa Costa as we spend a Saturday afternoon nibbling pretzel bits and sipping craft beer in a Point Loma eatery near her home. “South Park, Normal Heights, those were great starter neighborhoods a few years ago that I think have now passed beyond the range of average buyer affordability. Golden Hill is getting there, too.”

Head east, advises agent Melissa Costa.

These seem promising — definitive neighborhoods within city limits where Costa says she’s recently worked with first-time buyers. I ask what, in her clients’ eyes, makes a neighborhood an ideal fit.

“I think walkable access to parks and restaurants, especially if you feel safe walking at night, makes a lot of the neighborhood,” says Costa. She’s also a big fan of renovating the existing Craftsman and adobe-style bungalows that line many of San Diego’s more established blocks. “People are revitalizing instead of tearing down these fantastic older homes, and I think that’s something that helps.”

But these urban traits — walkability, access to fine dining and nightlife, and historic preservation are ones that resonate mostly with younger, childless singles and couples. For the first-time family buyer, the situation is different.

“With family buyers, schools are by far the number-one thing they’re looking for. But they’re also interested in quieter neighborhoods with slower traffic, cul-de-sacs, almost a Wisteria Lane kind of feel,” Costa continues, referring to the supposed utopian namesake street that formed the setting of Desperate Housewives, which so far as I can glean from my wife’s obsession with the show was a prime-time soap opera about adultery, backstabbing gossip, and violence whose picturesque suburban landscape apparently made up for all the neighborhood’s drawbacks.

Still, I get what she means — a quiet neighborhood where kids can set up a basketball hoop or ride bikes and skateboards without traffic whizzing past, where the school system receives good reviews, and reported crime rates are relatively low.

Schools, in particular, are among the top concerns cited by a host of both buyers and real estate agents when selecting a community. A veritable smorgasbord of websites, chief among them GreatSchools.org, publish rankings of the most and least desirable schools and compile data on performance of both districts and individual sites for parents to pore over. They largely list schools in the north-of-I-8 communities of Rancho Bernardo and Scripps Ranch as top-ranking destinations, though with median home prices ranging from $665,000 to $929,000, these are well outside the realm of average affordability.

Costa explains that these buyers will sacrifice proximity to amenities and accept that they won’t be leaving the house on foot in exchange for lower traffic levels and stronger school rankings. Many leave the city proper to find what they’re looking for at an affordable price.

“There’s definitely a certain demographic that would benefit from going east — they’re not as concerned about proximity to the beach, they’re not looking for a trendy neighborhood necessarily. And there’s much more affordable property in Lemon Grove, Spring Valley, parts of La Mesa, and El Cajon, even Santee,” says Costa, though in my nearly two decades selling real estate I’ve heard the same desires echoed by buyers heading for North County, South Bay (eastern Chula Vista, in particular), and some even moving to southern Riverside County — Temecula, Murrieta, and surrounding cities— in search of the same suburban bliss.

Median price in Chula Vista is $425,000

We’ve established some baseline traits for what makes a neighborhood desirable. But we still haven’t established a connection with what makes those same neighborhoods affordable, at least to those of us who’d like to occupy homes there. This is where the discussion gets a bit wonkish.

Let’s take a look at some of the common first-time buyer neighborhoods Costa suggests, with numbers provided by Core Logic for average home sale prices as of June 2016.

First off, we’re going to have to sadly conclude that, unless you’re willing to travel to the far extremes of the county such as Boulevard (about 68 miles from downtown San Diego; average recent sales price $252,000) or Borrego Springs (86 miles; $188,000) and spend considerable hours and gas money in the name of ownership, the comfortable definition of affordability is going to need to be stretched a bit.

One way the government does this is by including households making up to 120 percent of an area’s median income (let’s call that $76,080/year) in the pool of buyers eligible for “affordable” housing. Another is the FHA loan-guarantee program, which allows buyers to put as little as 3.5 percent down when buying a home, as most prospective first-time buyers don’t have tens of thousands of cash on hand.

As a hedge against risk based on how little the buyer is investing as compared to a traditional buyer with 20 percent cash on hand, FHA charges both an upfront “mortgage insurance premium” of nearly 2 percent of the loan amount that’s tacked on to the total loan amount as well as “private mortgage insurance” of 0.85 percent, essentially added to the interest rate. These extra charges go into a fund that guarantees lenders they won’t have to absorb the bulk of the loss if an FHA loan goes bad.

Location, location, location

The difference in monthly payments buyers must be able to weather is substantial. Let’s take a $400,000 home as an example. For a conventional buyer with 20 percent down and good credit, the monthly payment would be roughly $1931; for an FHA buyer it’s closer to $2354.

As of late July, the average going rate on an FHA loan was around 3.0 percent, effectively 3.85 percent when considering the mortgage insurance on top of the nominal interest rate. What does that buy?

Not a whole lot, unfortunately. Keeping within federal guidelines for an affordable home, a family earning just over $76,000 could buy a house for $320,000 at $1881/month (including property taxes and fire insurance) — that pretty much prices out anything within an hour’s drive of the city core.

But wait — a few more tricks with arithmetic might bring us closer to finding an affordable home for a slightly above-average buyer. For prospective borrowers with exceptional credit who are willing to put it all on the line to realize the dream of home ownership, loans are available allowing a buyer to spend up to 45 percent of their pre-tax income on fixed debts including the cost of the home and any other bills including car payments, student loans, and credit card debt.

Keeping the same numbers as before, our 120-percent-better-than-the-median buyer can now spend up to $2849 per month on housing, provided he or she has no other debts whatsoever — that’s good for a purchase price up to $494,000, and suddenly the map of prospective neighborhoods comes to life!

Median price in the Oak Park/Encanto area is $395,000

Clairemont ($595,000 median) is still a stretch, though City Heights ($374,000) and Encanto ($395,000) are in. Hillcrest ($948,000) and North Park ($576,000) are still rarefied air, but La Mesa ($487,000-572,000), Lakeside ($458,000), and Lemon Grove ($405,000) are in the picture. Poway ($697,000) and San Carlos ($600,000) are out, but National City ($365,000) and Spring Valley ($420,000-459,000) remain contenders. Going north and south, Vista (as low as $428,000), Escondido (starting at $425,000) and western Chula Vista (from $425,000 up) are players.

It turns out Costa has a pretty good handle on what buyers say they’re looking for in a place to call home.

“Not being on a main, busy street was huge for us — somewhere where we could feel safe with our kids playing out front, and if I had to run inside for a second it’s not like I’d feel scared of something happening to my child,” says Anna Carel, who along with her husband David and two young children, moved into a townhome in Lakeside last May.

“It’s funny, everyone who comes to visit us remarks how they never even knew this neighborhood existed.”

Indeed, the cul-de-sacs off Saddle Ridge Road, each occupied by a handful of twin-homes (treated like a single-family house but with one shared wall), is easy to miss. Flanked on the north by a newer housing tract and the south by mid-century ranch homes, the ’70s-era development is dotted by eucalyptus and palms, with mature oak trees offering patches of shade in a handful of communal grass lawns dotting the complex. Go a quarter-mile in about any direction and you’ll find nothing but open space, hilly patches of southeastern Lakeside as yet untouched by the ever-charging force of suburban development.

For the Carels, moving back home to East County where they grew up from Oceanside (where the family had temporarily relocated to be closer to David’s job at the time) was a bumpy road.

“We’d been working on trying to buy a house for two or three years, saving and getting our credit in order. We’d have actually done it a lot sooner, we just weren’t quite there yet,” says David. The couple’s home, purchased for a little over $330,000 (though homeowners’ association fees drive the cost up above that of a similarly priced single-family home), was made possible through an FHA-guaranteed loan with its mandatory monthly mortgage insurance premium tacked on to the regular payment.

“The older I get the more it becomes clear that you’re only really worth what your credit score and your bank account says about you to a lender, how you look on paper,” adds Anna, 29, who is nonetheless thrilled to be a homeowner. “The tax write-offs and financial benefits are huge, so is knowing that you’re investing in something for the future. “It’s something that definitely makes you feel like you’ve graduated into a more responsible phase of life.”

Aside from the quiet location, I ask what else influenced the Carels’ decision when they were home shopping, and what other parts of town might have appealed to them. Quality of school district is the first thing that comes to mind, and it does so in a big way.

“I did a lot of searching around on different websites, asking friends who were parents at different schools, looking for our best options. But obviously the better the school district, the more expensive the houses are around it,” Anna laments. “For instance, Poway has amazing schools, among the tops in California, but real estate there was entirely out of reach financially. I feel comfortable that we’ve made a good choice with where we are, though — the schools here are rated higher than a lot of other areas in our price range.”

“We wanted to get back to where our friends and family were, and where we could plan on staying for some time without worrying about moving our kids from school to school. That was another big target, to get into a place before our son started kindergarten, so he could stay with the same group of friends throughout his time there,” David adds, though the long process of improving the couple’s credit and amassing a down payment means that first grade, not kindergarten, will be the younger David’s introduction to the school system where the family hopes he’ll stay through high school.

“We looked in Santee, El Cajon, La Mesa, Mira Mesa, Poway, Tierrasanta…” David tells me, counting off neighborhoods both in San Diego and the suburbs the family had been interested in before Anna jumps in again.

“A lot of those areas were kind of, like...we went and looked there because of the school districts, then right away we figured out we weren’t going to be able to really find a viable option financially.”

Not only were high prices a deterrent, poorly ranked education was just as likely to take a neighborhood out of the running.

“Schools were a huge obstacle. We’d find a great house at the right price, but the local schools wouldn’t be rated so well, so that one would be out,” David admits. “There were a lot of houses I wanted to buy but I didn’t want to enroll my kids in the local school system.”

Despite the arduous process, the Carels are convinced they made the right choice by electing to buy.

“Cosmetic things — deciding what to put where, what color paint to use, what you want to do with your yard — that’s really the most exciting part to me,” says Anna.

“I definitely think we made the right choice in becoming homeowners as opposed to remaining renters,” David concludes.

The once-again-high-flying housing market, though, doesn’t seem as rosy to everyone in town.

The corner of University and Fairmount Avenues in the heart of City Heights paints a picture of rebirth that seems to represent urban renaissance idealized. Two corners are occupied by newly built mid-rise office and mixed-use residential/commercial structures. A third is home to a new shopping plaza, the colorful paint still crisp on the façades of Denny’s, McDonald’s, and Panda Express, shade trees planted along the parkways are still years from maturity.

The fourth corner, housing a decades-old strip mall that’s home to a discount shoe store and combination donut shop/Chinese restaurant, may be more indicative of life on the Boulevard, a life that at least some residents will mourn the loss of.

Walking down Polk Avenue, just a block north of University, it feels like an entirely different world. The sounds of reggae, horn-heavy norteño ballads, and mid-morning television talk shows provides the narrow one-way street’s soundtrack. An old mattress slumps against the side of an apartment building, threatening to fold over itself and flop onto the sidewalk.

Properties in the neighborhood are a mix of early-1900s Craftsman-style bungalows and Huffman six-packs, boxy, characterless apartment buildings stuffed onto former single-family lots in the late 1970s and early 1980s with a push from developer Ray Huffman and then-mayor Pete Wilson as a proposed solution to conquering suburban sprawl in the face of a population influx. The landscaping is barren in some spots, mature or overgrown in others. Many front yards have been given over to parking.

Working people have been priced out of Rich Kacmar and Anna Daniels’s City Heights neighborhood.

Amid this scene stands the cozy two-bedroom abode of retired librarians–turned–community activists Anna Daniels and Rich Kacmar. A canopy of climbing roses and vines overtaking black bamboo surround the cottage. A pink trumpet tree grows near the colorfully painted wooden fence out front. Despite their relatively stable footing today, Daniels worries that not only is ownership getting farther out of reach, the simple matter of remaining housed at all in the face of another real estate spike poses a real challenge to some of her neighbors.

“The house was, at the time and relatively speaking, affordable,” Daniels says, speaking of when she and her husband first purchased their home on 45th Street in 1986. I ask her, if she were in the same position today as 30 years ago, would she be considering moving into the same neighborhood?

“Oh, heavens no. This has been a working-class neighborhood since its inception in the ’20s, and while I’d say it’s still a working-class neighborhood the people today have to work a lot harder. I’d probably write off the possibility of buying a house. Even after 30 years my husband’s and my salary never increased at the same rate as the price of real estate in San Diego, particularly the inner-city communities. The reality is this house, that we paid $81,000 for, was a stretch — it would be absolutely, completely out of reach at $350,000 today.”

An estimate from Zillow, a popular automated home-valuation system, estimates the current value of the couple’s home closer to $412,000.

“The big issue here is affordable housing, with a significant ancillary issue being livable wages. You have to remember that City Heights is one of the poorest communities in San Diego — people on my block have about a $3000 monthly household income,” Daniels tells me as we sit on her porch, occasionally interrupted by a passing car or groups of enthusiastically loud chatters walking by. “I talk to people and I’m amazed to hear that they’re paying over a thousand dollars a month for a one-bedroom apartment in City Heights. Is that affordable? I think it’s a relative term; historically, families have been able to make the rent somehow, though it’s usually meant they’re having to double up.”

She mourns the fact that efforts to prop up affordability are often overshadowed by a push to gentrify urban neighborhoods and celebrate newfound affluence while ignoring residents pushed further to the fringe.

“When we moved here, there was a 16-unit apartment complex across the street. They were turned into condos right before the economy tanked. Prior to that, those units were filled with Mexican-Americans who supported a whole economy on the street — everyone from a green grocer to a door-to-door egg man. And these people were displaced when the apartments were turned into condominiums, which the developer tried to sell for around $290,000. The prices kept dropping, though, until the units were eventually rented back out. So we took 16 families who were living in City Heights and displaced them with new renters able to afford higher rents. I’ve kept up with a lot of those families, and a few of them found other neighborhoods nearby, but a lot ended up in El Cajon. And for people without cars who are commuting to work, that adds a lot of extra time to their days.”

Daniels is interested in exploring the possibility of using community-based nonprofit organizations to acquire and maintain a housing stock that’s attainable for lower income families, though she says most of the focus to date is on private investment, where builders are encouraged through subsidies and incentives to maintain a certain percentage of their development as “affordable” housing.

Under the California Redevelopment Act, which governed redevelopment agencies until these bodies were dissolved in 2012, for example, developers had to make at least 15 percent of the units developed in a residential project affordable to people of “low-to-moderate-income households,” defined as those making up to 120 percent of the area’s median income, or $76,080 per year in San Diego.

“When you’re looking at affordability, my sense is that, after having participated in all sorts of community forums and planning committees, turning over the problem to the private sector is not an answer to our crisis. And affordable housing certainly is a crisis,” Daniels warns. “The path that we’ve been following hasn’t been able to provide an adequate number of units.”

Median price in University Heights is $550,000

Licensed real estate agents are bombarded with dozens of promotional emails from other agents daily. A sampling I’ve received: there’s a 676-square-foot Craftsman on the border of North Park and City Heights going for $420,000; a slightly larger two-bedroom, one-bath Spanish adobe house in Kensington for $609,000; a cozy three-bedroom single-story in suburban Rancho Peñasquitos boasting access to the coveted Poway schools is only $580,000. A 4S Ranch “executive home,” really just a nondescript tract home surrounded by hundreds more like it but with considerably more square footage than the others on this list, is priced at $1,150,000.

Despite Daniels’s bleak assessment of the current state of real estate, there are still plenty of hopeful buyers scouring the city for a place they hope to call home. One of them is Angela Clapp, a nurse manager of a surgical department at Scripps Memorial Hospital La Jolla who’s been placing offers since early May.

House hounting “has been tough” for Angela Clapp.

I meet Clapp when her agent leaves town for a few weeks on vacation. We get to know one another a bit when I step in to show her a few condos in case an irresistible deal pops up. She agrees to help me understand her perspective as a first-time, single buyer searching for a home in San Diego’s urban landscape.

“I’ve been shopping for about three and a half months,” Clapp tells me. “Now that I’ve narrowed it down I’m looking mainly around the PB and Bay Park neighborhoods. When I started, I was looking everywhere — Clairemont, North Park, just seeing what was out there. But for me and my lifestyle, I wanted to be closer to the bay. I like to kayak, so having access to recreation is what I’m looking for. Can you just walk out the door and go grab a cup of coffee? Is there a store to walk to? That’s a big appeal to me. That’s a big selling point to me, accessibility of the community.”

Clapp, though, has a problem common to first-time buyers who want to stay close to the urban core and its attendant amenities. Without the significant lump of cash that usually comes from selling another property that’s built up equity over the years, she needs an FHA loan that will let her borrow all but 3.5 percent of the purchase price. And she’s got a spending cap of $400,000, which means she’s almost definitely looking for a condo.

During the last market crash, FHA took two actions that severely limited the available supply of condominium housing eligible for financing. First, they eliminated the “spot approval” process, where a single unit within a larger development could be considered for loan approval, given that the homeowners’ association books showed sufficient cash reserves to cover anticipated repairs and that the building was primarily occupied by the owners of the units. Second, they cancelled the blanket approvals that many complexes had qualified for, which allowed FHA buyers to purchase within a development without jumping through the extra spot-approval hoops. Even half a decade later, few associations have applied for reapproval of their buildings.

“It’s been tough,” Clapp sighs. “It’s certainly been difficult as an FHA buyer when it comes to condos. I’m looking at potential avenues to possibly go conventional. After the market crashed, FHA changed so that there’s so much more that needs to be done to get a condo FHA-approved, so I’ve definitely hit a roadblock.”

I should mention here that many conventional, non-government-backed lenders offer “FHA lookalike” loans that, like FHA loans, allow a buyer to borrow 95 to 97 percent of the money needed to buy a home. These could open the door to condo ownership for some first-timers, but much more stringent credit-score requirements and higher interest rates place them out of reach for many borrowers, Clapp included.

“There have been a couple I’ve found that are approved, but unfortunately I’ve been outbid on the offers I’ve put in,” Clapp says of the few chances she’s had to get in on a condo that fit her loan requirements. “When I’ve put bids in, there have always been other offers and I’ve had to deal with counter offers. Anyone looking to buy should anticipate competition — it’s not going to happen quickly, and when the time is right it’s right.”

She realizes, though, that wherever she ends up probably won’t meet the definition of a “forever” home, and that’s okay.

“For this phase of my life, this is what fits. Whether I’m there for five years, ten years — it’s not a lifelong place. I’d like to keep the place and rent it, even if I don’t live there. I definitely still want to be in San Diego a decade from now. I’m 31; in five or ten years maybe I have a family, I might outgrow a two-bedroom condo.”

Despite months of setbacks, Clapp remains optimistic and keeps in mind the personal motivations that drive her, along with hordes of other hopeful buyers she’s competing with for a slice of the pie, to keep searching.

“I have friends who’ve recently bought homes, and they’re very happy. So I thought, why not me too? I want to be able to have somewhere to call home, and that’s somewhere to share with people that matter to you. That’s my incentive, my push.”