{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

USD’s Frank Partnoy might scare you

The inscrutable derivatives

What’s inside a massive American bank? Bunk.

What’s inside a massive American bank? Bunk.

That’s right. Those huge institutions — which we rescued with trillions of our dollars during the 2007–2009 Great Recession — are just as inscrutable, just as opaque, just as incomprehensible as they once were.

Frank Partnoy

That’s the view of Frank Partnoy, professor of law and finance at the University of San Diego and the founding director of the university’s Center for Corporate and Securities Law.

I will never forget his arrival in 1997. I was reading a story in the New York Times about a hot new book, F.I.A.S.C.O., that was roiling Wall Street and scaring the bejeebers out of investors. It was about financial derivatives, something that even many investment sophisticates knew little about. Buried in the story was a mention that the book’s author, Frank Partnoy, was headed to the University of San Diego to join the law faculty. I called the law school, reached Partnoy, interviewed him before he had put chairs in his new office, and had a column about him in the next day’s Union-Tribune.

F.I.A.S.C.O. followed by Infectious Greed.

Shortly, Partnoy was testifying before Congress, writing editorials for the Financial Times and New York Times, and being interviewed on NPR and CBS’s 60 Minutes. Soon, he was writing more books: Infectious Greed (about which I wrote my first Reader column), The Match King (about Ivar Kreuger, who monopolized world match production), and Wait: The Art and Science of Delay (which celebrates long-term thinking and, in some cases, inaction).

In January of 2013, Partnoy and ProPublica financial reporter Jesse Eisinger wrote a lengthy cover story for the Atlantic magazine. Gist: financial statements of America’s big banks are impossible to analyze. Valuations of assets are deliberately hazy. Liabilities are concealed through faulty accounting. The financial reports of those big Wall Street banks are basically unintelligible, and bank managements often like it that way.

Is Dodd-Frank taking root?

I asked Partnoy to update things. The Wall Street Reform and Consumer Protection Act, called Dodd-Frank, signed in 2010, was taking root. Or was it? The Volcker Rule (named for former Federal Reserve chairman Paul Volcker), supposedly banning bank traders from gambling with depositors’ money, finally went into effect in 2014. Was it taming out-of-control young speculators? Can one trust the accounting of the big banks?

Nope, says Partnoy. “It is amazing to look at bank financial statements of today and see how similar they are to statements of several years ago,” he says. “It is almost like a cut-and-paste job in various sections.”

One similarity is really frightening: derivatives. They are contracts between two or more parties that derive their values from an underlying entity — a stock index, an interest rate, a currency, a commodity, or any number of things. Wall Street firms hire math PhDs from Harvard and the Massachusetts Institute of Technology to concoct bewilderingly complex derivatives. They are sold to institutions all around the world. Procter & Gamble, one of America’s smartest companies, said it didn’t understand derivatives that, somehow, it purchased. As Partnoy revealed in F.I.A.S.C.O., Wall Street peddlers of highly complex derivatives often don’t understand them, but brag upon making a sale, “I ripped [the customer’s] face off.”

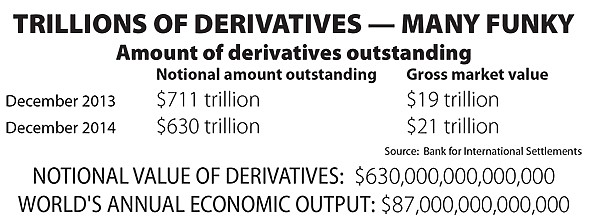

Trillions of derivatives, many funky

The better-known and more simply constructed derivatives, such as “puts” and calls on a stock, are traded on an organized exchange, are regulated, and aren’t particularly dangerous to society. But the often-abstruse over-the-counter derivatives are still traded in what is sometimes a Wild West environment. At the end of last year, there were $630 trillion of these instruments outstanding. That’s $630,000,000,000,000, or $630 million million. Partnoy calls many of them “custom-tailored, funky” derivatives. A comparison: the gross world product, or total annual economic output of all the world’s economies, is around $87 trillion. All that $630 trillion is not at risk, but $21 trillion is the gross market value of over-the-counter derivatives and could be involved in a chain reaction, with financially troubled buyers unable to meet their obligations. World leaders feared that would happen in 2008.

Once Dodd-Frank took effect, “banks lobbied hard,” says Partnoy. The banks convinced politicians and the regulators that regulation should be aimed mainly at what he calls the “plain vanilla” derivatives, such as the simpler ones traded on exchanges, but should not be extended to the “funky” derivatives that are often mysterious and potentially dangerous.

How banks avoid the Volcker Rule

Thanks to Dodd-Frank, the Volcker Rule, and plain common sense, banks are not as exposed to derivatives as they once were, but they are still grossly overexposed, says Partnoy. The banks no longer can have their exuberant youth trading derivatives with depositors’ money, but the banks can engage in “customer accommodation trading.” In essence, the bank is its customer’s counter-party. If a customer “bets that the Chinese currency will go up, the bank bets it will go down,” says Partnoy. Such a maneuver avoids the Volcker Rule “but is still potentially risky.”

To put a value on such a contract, banks will say they use “model-based valuation techniques,” or, realistically, “estimates.” Sometimes, banks will tell their shareholders they arrive at estimates by using “model-based techniques that use significant assumptions not observable in the market.” Huh? “Not observable?” Sounds more like a guess than an estimate.

“It’s impossible to figure out the details of what banks’ positions really are,” says Partnoy. What’s more, “It’s impossible for the chief executive of a bank to understand what the bank is really worth.”

Enron and the special purpose entities

Banks are pulling an accounting ruse similar to that used by the scandal-plagued and now-deceased Enron. That company used so-called special purpose entities to disguise what it was doing. These entities, only partly owned by Enron, sometimes based offshore for tax purposes, were used to hide liabilities: the entity would take on risk, but the debt didn’t show up on Enron’s books.

Banks are using similar “variable interest entities,” in which they may have a controlling interest but not majority voting rights. The financial support may come from an outside source. The banks can borrow money and buy assets, but the liability is not recorded on their books. “There is a lot more detail now than Enron provided, but you still can’t answer crucial and simple questions about risk,” says Partnoy.

Here's something you might be interested in.

USD’s Frank Partnoy might scare you

The inscrutable derivatives

USD’s Frank Partnoy might scare you

The inscrutable derivatives

What’s inside a massive American bank? Bunk.

What’s inside a massive American bank? Bunk.

That’s right. Those huge institutions — which we rescued with trillions of our dollars during the 2007–2009 Great Recession — are just as inscrutable, just as opaque, just as incomprehensible as they once were.

Frank Partnoy

That’s the view of Frank Partnoy, professor of law and finance at the University of San Diego and the founding director of the university’s Center for Corporate and Securities Law.

I will never forget his arrival in 1997. I was reading a story in the New York Times about a hot new book, F.I.A.S.C.O., that was roiling Wall Street and scaring the bejeebers out of investors. It was about financial derivatives, something that even many investment sophisticates knew little about. Buried in the story was a mention that the book’s author, Frank Partnoy, was headed to the University of San Diego to join the law faculty. I called the law school, reached Partnoy, interviewed him before he had put chairs in his new office, and had a column about him in the next day’s Union-Tribune.

F.I.A.S.C.O. followed by Infectious Greed.

Shortly, Partnoy was testifying before Congress, writing editorials for the Financial Times and New York Times, and being interviewed on NPR and CBS’s 60 Minutes. Soon, he was writing more books: Infectious Greed (about which I wrote my first Reader column), The Match King (about Ivar Kreuger, who monopolized world match production), and Wait: The Art and Science of Delay (which celebrates long-term thinking and, in some cases, inaction).

In January of 2013, Partnoy and ProPublica financial reporter Jesse Eisinger wrote a lengthy cover story for the Atlantic magazine. Gist: financial statements of America’s big banks are impossible to analyze. Valuations of assets are deliberately hazy. Liabilities are concealed through faulty accounting. The financial reports of those big Wall Street banks are basically unintelligible, and bank managements often like it that way.

Is Dodd-Frank taking root?

I asked Partnoy to update things. The Wall Street Reform and Consumer Protection Act, called Dodd-Frank, signed in 2010, was taking root. Or was it? The Volcker Rule (named for former Federal Reserve chairman Paul Volcker), supposedly banning bank traders from gambling with depositors’ money, finally went into effect in 2014. Was it taming out-of-control young speculators? Can one trust the accounting of the big banks?

Nope, says Partnoy. “It is amazing to look at bank financial statements of today and see how similar they are to statements of several years ago,” he says. “It is almost like a cut-and-paste job in various sections.”

One similarity is really frightening: derivatives. They are contracts between two or more parties that derive their values from an underlying entity — a stock index, an interest rate, a currency, a commodity, or any number of things. Wall Street firms hire math PhDs from Harvard and the Massachusetts Institute of Technology to concoct bewilderingly complex derivatives. They are sold to institutions all around the world. Procter & Gamble, one of America’s smartest companies, said it didn’t understand derivatives that, somehow, it purchased. As Partnoy revealed in F.I.A.S.C.O., Wall Street peddlers of highly complex derivatives often don’t understand them, but brag upon making a sale, “I ripped [the customer’s] face off.”

Trillions of derivatives, many funky

The better-known and more simply constructed derivatives, such as “puts” and calls on a stock, are traded on an organized exchange, are regulated, and aren’t particularly dangerous to society. But the often-abstruse over-the-counter derivatives are still traded in what is sometimes a Wild West environment. At the end of last year, there were $630 trillion of these instruments outstanding. That’s $630,000,000,000,000, or $630 million million. Partnoy calls many of them “custom-tailored, funky” derivatives. A comparison: the gross world product, or total annual economic output of all the world’s economies, is around $87 trillion. All that $630 trillion is not at risk, but $21 trillion is the gross market value of over-the-counter derivatives and could be involved in a chain reaction, with financially troubled buyers unable to meet their obligations. World leaders feared that would happen in 2008.

Once Dodd-Frank took effect, “banks lobbied hard,” says Partnoy. The banks convinced politicians and the regulators that regulation should be aimed mainly at what he calls the “plain vanilla” derivatives, such as the simpler ones traded on exchanges, but should not be extended to the “funky” derivatives that are often mysterious and potentially dangerous.

How banks avoid the Volcker Rule

Thanks to Dodd-Frank, the Volcker Rule, and plain common sense, banks are not as exposed to derivatives as they once were, but they are still grossly overexposed, says Partnoy. The banks no longer can have their exuberant youth trading derivatives with depositors’ money, but the banks can engage in “customer accommodation trading.” In essence, the bank is its customer’s counter-party. If a customer “bets that the Chinese currency will go up, the bank bets it will go down,” says Partnoy. Such a maneuver avoids the Volcker Rule “but is still potentially risky.”

To put a value on such a contract, banks will say they use “model-based valuation techniques,” or, realistically, “estimates.” Sometimes, banks will tell their shareholders they arrive at estimates by using “model-based techniques that use significant assumptions not observable in the market.” Huh? “Not observable?” Sounds more like a guess than an estimate.

“It’s impossible to figure out the details of what banks’ positions really are,” says Partnoy. What’s more, “It’s impossible for the chief executive of a bank to understand what the bank is really worth.”

Enron and the special purpose entities

Banks are pulling an accounting ruse similar to that used by the scandal-plagued and now-deceased Enron. That company used so-called special purpose entities to disguise what it was doing. These entities, only partly owned by Enron, sometimes based offshore for tax purposes, were used to hide liabilities: the entity would take on risk, but the debt didn’t show up on Enron’s books.

Banks are using similar “variable interest entities,” in which they may have a controlling interest but not majority voting rights. The financial support may come from an outside source. The banks can borrow money and buy assets, but the liability is not recorded on their books. “There is a lot more detail now than Enron provided, but you still can’t answer crucial and simple questions about risk,” says Partnoy.

Comments