{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

The tanda system of savings among Oceanside immigrants

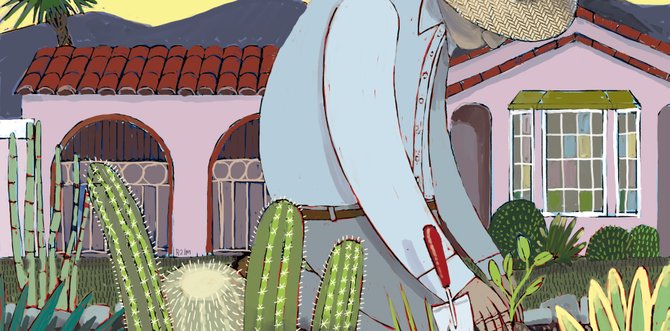

Your gardener could be a banker

Miguel Herrero is just another Mexican.

Six days a week you might drive by him anywhere in the Carlsbad/Oceanside area. You’d see him building fences, planning drainages, wiring timers, and caring for trees. But the most interesting thing about him is what you can’t see.

In his off hours, Miguel is a community banker, an insurer of last resort, and a fixer of problems. A whole community turns to him for advice, and for money. There are even people deep in the Mexican state of Oaxaca, almost all the way down at the border with Guatemala, who give him a call when they have a personal problem, or when, say, the local church needs re-stuccoing but can’t afford the necessary scaffolding to do the job.

On his best day he might hit 5'6", even counting the virile mass of wavy black hair atop his head. He is a neat dresser. The day I meet him for an interview, he’s wearing a stylish black T-shirt with some kind of heavy-metal-looking skeleton design on it.

We meet at Oceanside’s L&L Hawaiian Barbeque. I have no idea why we’re meeting here, except that my brother, who has known Miguel for a decade and a half and who has agreed to translate, told me to show up at 4:30 on a Sunday afternoon.

The mall parking lot is half empty. Actually, a good part of the mall itself is empty. Not only empty of customers, but of tenants. The old Mervyn’s a few doors down from L&L just sits there, empty, month after month. The frozen-yogurt shop is gone. The Hallmark card shop is gone. So is the car dealership across the parking lot.

All over Oceanside, probably all over America, gaps have formed in consumer society. Dead spots. A lot of people are living through their own private financial hells.

Miguel is standing outside the L&L when I get there. My brother is late, so we go inside, order a couple of sodas, and talk in my poor Spanish and Miguel’s poor English about his financial work.

I ask what this money thing he does is called.

“Tandas [or] cundinas,” he says, “it’s the same thing.”

What word does he prefer?

“Tandas.”

He explains that, right now, he is in the second week of a 12-week tanda. Its structure could not be simpler — each member agrees to contribute $100 per week for 12 weeks. They will give the money to Miguel, who will hand it each week to one of the members. When the 12 weeks are over, a new tanda starts. Miguel says membership varies from 10–20 people each time.

Before the first week of each cycle, members choose numbers. The number chosen signifies the week the member will get paid $1100 (and will not have to contribute the weekly $100).

Members can buy one week, two weeks, even partial week arrangements such as one and a half weeks.

Some members ask for an early number, “because they need the money right away,” Miguel says. Such a request is perfectly acceptable.

“Some other people can wait to take their money,” he adds. Such a person can ask for a late number. The member might ask to go last, for example, so that each week constitutes, essentially, a payment into a 12-week savings plan.

In an emergency, a member can tell the group that he or she needs the money on any given week, and the group will rearrange paydays so that the member with the emergency can get paid immediately.

In this way, the tanda acts as a system of savings, of loans, and of insurance for emergencies.

Miguel says that, even if a person has already been paid in, say, week one, and they have an emergency in week nine, they can get paid again immediately, so long as they agree to give up their number in the next round.

“You know the people,” Miguel says. “It’s okay.”

Most of the people in Miguel’s tanda live in or near Oceanside’s Crown Heights neighborhood.

The tightly packed quarter is a short walk to the beach, to Oceanside High School, to the strip mall that has stood across from the high school for ages, and even to the new Fresh & Easy market on Oceanside Boulevard. There are plenty of spots nearby to shop and bank at, but a good percentage of the neighborhood’s banking goes on right here, just as a good percentage of the neighborhood’s shopping is done off the backs of trucks that park for hours along Division Street, or around the corner on Grant Street, down by the community garden.

For as long as there has been an Oceanside, this has been “the barrio” — one of those little Mexican hearts that beat near the center of nearly every beach city in Southern California. Once a seedy spot, Crown Heights today is mostly free of graffiti; the streets are clean and the sidewalks relatively busy. But the little houses and apartment buildings are much more crowded than is typical of Southern California.

You can get vegetables, baked goods, beverages, candies — almost the whole grocery array — off of those trucks. And you can get it without venturing out of Crown Heights, which is important if you don’t have a car or much English vocabulary.

Despite its outside reputation for crime, Crown Heights is a family place. Most of the small communities that make up the neighborhood are peaceful clusters of families, each with its own regional flavor.

Miguel’s flavor, like many people in Crown Heights, is Oaxacan. He figures there are probably 1000 Oaxacans in Oceanside.

If it seems odd that so many people from Oaxaca, one of Mexico’s southernmost states, would end up in Oceanside, one only has to understand a phenomenon that migration researchers call “sister communities.”

Dr. Ramona Pérez, director of the Center for Latin American Studies at San Diego State University, has worked in Oaxaca for two decades. She says, “You could go into any community in Oaxaca at this point and ask them, ‘Where’s your sister community?’ And they’ll say, ‘We go to Los Angeles,’ or ‘We go to San Diego,’ or ‘We go to Vista,’ or ‘We go to Chicago.’”

Many of these sister community relationships date back to the Bracero Program, a U.S. government program from the World War II era, in which Mexican laborers were given a chance to work in the U.S. while homegrown labor was off fighting in Europe or the Pacific. The program lasted until the early ’60s. Many Mexican participants put down roots in the U.S., later serving as helpers for family members and townsfolk who wanted to come to the U.S.

“Once you get a few people that have settled in an area and know the lay of the land, they serve as a hub for other people coming in,” says Dr. Pérez. “Some of them have been able to acquire linguistic skills. Where that doesn’t exist, they still understand transportation, they understand where jobs are, they know where healthcare is, they know where housing is, which landlords will allow them to come in with limited documentation, that kind of thing.”

In the past few decades, Miguel says, more and more Oaxacans have gone to Las Vegas, where they plant flowers and ferns around the big casinos in the morning, then tear out those same plants around midnight, when truckloads of new plants come and the daily cycle of dressing one of the hottest and driest cities in the world in a coat of tropical plants starts all over again.

But if you live in the town of El Trapiche, the people you know, the people you grew up with, they go to Crown Heights.

El Trapiche is a dirt-road farming town just off a sharp bend of highway about 40 miles south of Oaxaca City, which is, itself, about 1400 miles straight south of San Antonio Texas, or about 400 miles southeast of Mexico City.

I’ve never been there, but on Google Maps and Google Earth, El Trapiche compares to Oaxaca City, a city of about 250,000, in the way that Bonsall might compare to San Diego.

Before he first came to the U.S., Miguel was at one time a 12-year-old bull-riding champion from El Trapiche, winning prizes at rodeos all over the area. More than 20 years later, he recalls the bull-riding fondly, but, with three children, he says he would never get on a bull now.

When my brother arrives at L&L, we are able to get into a deeper discussion. I ask Miguel why members of his tandas don’t just go to a bank and start saving that way.

He doesn’t have much of an answer to this. In fact, the question seems, at first, to make little impression on him. In his view, it’s not that the Mexicans — and a few Guatemalans — who are in his tandas are afraid of the bank or unwilling to pay bank fees. They stay out of banks simply because banks are not something they are familiar with. They do not feel confident about walking into a bank, filling out a lot of paperwork that means nothing to them, and handing over their money to people they do not know and whose motives they cannot guess.

In the part of the world they come from, he tells me, loans are made by local patróns, rich men who loan money because they can make a tidy profit by making lots of small loans to their neighbors. And they know they can find you if you don’t make your payments.

“They act like it’s a favor to you,” Miguel says about these local patróns, “but they charge a lot of money.”

Are they like mafiosi, I ask him, searching for a word in my limited Spanish vocabulary, “bandidos”?

“No,” he says, kind of taken aback, they are just “patrones.”

So, without any inclination to walk into a bank, and with an already well-established habit of private financial dealings, many immigrants just naturally bank with Miguel, or with one of the many, many people who play a role like Miguel’s in immigrant communities (and even in some well-established Mexican-American communities) all around the U.S.

This kind of banking has a formal name among the IMF and World Bank types, it’s called ROSCAS: rotating savings and credit associations.

Academics have been studying such associations since the 1950s. The Global Development Research Center says they “can be seen in almost every society around the world, and have been in existence for a considerable period of time. They are flexible and adapt themselves easily to rural and urban peculiarities as well as existing community patterns of grouping/organizing. This flexibility is one reason for their worldwide popularity.”

Despite their informality and flexibility, or maybe because of it, rotating savings and credit associations are powerful little engines of economic activity, ingenious, really, in that they allow for people who either do not want to or cannot access established banking to make and get loans, to build up savings, to help out neighbors who may be facing an emergency, to keep community and family ties intact amidst a foreign culture, and even to maintain ties between members of a community like El Trapiche, who have come to the U.S., and those who have stayed or returned home.

Carlos Vélez-Ibañez wrote the book on these U.S.-based Mexican associations: An Impossible Living in a Transborder World. Part of his thesis is that the entire southwest of the North American continent is becoming one big, integrated economic region; the associations help facilitate the flow of goods and services within the region. They help Mexican nationals, who tend to be poorer and have less access to power, to function efficiently and effectively within this transnational economic reality.

His book is filled with academic jargon, and some Americans might categorize his thinking as the kind of squishy academic denial about border reality that has led to the lawlessness we now see along practically its full length.

For example, Vélez-Ibañez often puts the word “citizenship” in quotes, as if to suggest that the concept is less than real, a figment of the right-wing imagination, perhaps.

His research offers fascinating insights into a profound financial and social reality that, while it is literally right next to them, many Americans are oblivious to. Vélez-Ibañez suggests that this obliviousness to the financial ingenuity of Mexicans in America is part of a broad denial of the personhood and creativity of the Mexicans in our midst. But it could also be simply that linguistic barriers do not allow Mexicans in the U.S. to chat about these things with Americans.

The upshot of the Mexican habit of private, even secret, banking is that an individual who may appear to Americans as just another poor Mexican laborer is responsible, at any given time, for large sums of other people’s money and for facilitating the banking needs of families, clans, even whole neighborhoods.

Tandas may be the most common and obvious of the various off-the-radar financial tools available to Mexican immigrants, but it is only one among many.

Miguel, as a leader among the Oaxacans of Oceanside, provides an example of some other ways that Mexican financial interdependence works in the U.S.

He has made alliances with Americans who are willing to help poorer Mexicans. He has found Oceanside dentists, for example, who provide special rates to Mexicans lacking insurance. He has a well-off American business associate who sometimes puts up money, to be paid back in installments, when a member of the community needs help with an immigration issue or to get a car out of impound or some similar crisis.

Miguel, himself, now has the financial means to act as a patrón for families with medical bills or other sudden needs. And the entire Oaxacan community will help in a pinch by making lots of small donations, as they did when a Oaxacan family recently had a sick child who needed hospital care.

Back in El Trapiche, when the church needed that new stucco job, it was Miguel who got the call and organized the fundraising to pay for the scaffolding. Asked how he acquired this responsibility, Miguel smiles and shrugs innocently.

“He’ll never tell you how important he is in the community,” my brother says.

Miguel came north about 20 years ago, when he was 14. His family is a farming family, and during some of the dry years, the fertility of their land did not match the fertility of Miguel’s mother and father. They sent the boy north with an uncle, so that they could be sure he would eat.

The pair took a bus to Mexico City, a train to Mexicali, another bus to Tijuana, and made what was then a fairly easy crossing into the U.S.

In the U.S., the uncle got Miguel into a taxi and up to Oceanside, where he boarded with Oaxacan cousins.

He went to work for an Encinitas flower grower because he thought he would not only find steady work there, but also a chance to learn the business of horticulture. He moved from job to job, always getting both a paycheck and an education from his employers, until he was ready to start his own landscaping business.

Today he has eight employees.

Certainly, his intelligence and confidence make him an unusual person and have made much of his success possible. But he could not have made it to where he is on his own. Without a network to tap into when he came north, and without systems that aided in his financial success, there is no telling where he would be.

This habit of financial interdependence is what we might call the Mexican way of money, and, along with the many Mexican dishes that have become ubiquitous on American menus, it could be one of the lasting benefits Mexicans have brought into the U.S.

Some of the financial tools that Mexican families have at their disposal might, in fact, be the envy of many lone, struggling, and relatively financially isolated American households.

That is to say, financial cooperation and mutual assistance are far more the norm among Mexican immigrants than among Americans, and this cooperation and mutual assistance offers considerable benefits.

For many Mexicans, money troubles are community troubles. The community has, therefore, developed modes of helping people with money troubles. In contrast, an American with money troubles tends to become more isolated, putting up a brave public face while suffering and worrying alone.

Faced with the need to save and the need to have some insurance for emergency situations, Mexican men and women enter into rotating savings and credit associations together. They help each other save and make allowances for each other in emergency situations. Maybe this kind of thinking about money will one day be thought of as a contribution to American society, a prompt for Americans to be less isolated and more interdependent in terms of finances.

Since 2002, when he started sponsoring tandas for his community, Miguel has collected money hundreds of times, maybe thousands, and only twice has anyone failed to pay. In both cases, the person fled the area. Miguel called family members, seeking help in recouping the money, but none was able to help or to locate the absconders. In time, Miguel did find one of those who failed to pay, and the young man simply said, “I don’t have the money.”

So Miguel covered the losses himself. “As the person in charge, I didn’t get the money, so I had to pay it,” he says, seemingly without resentment.

Thus, no member of Miguel’s tandas, except Miguel himself, has ever lost money. It is this kind of personal responsibility that makes tandas go. “Confianza” — trust in the community — allows for a savings and credit market to be created and sustained.

Miguel says he has no need for tandas anymore; he runs the tandas because other people want him to. It is important that he do so because the trustworthiness of the tanda leader is an essential component of its success. For example, when Miguel was new to the U.S., he began participating in tandas. My brother asks him if he knew the people in the tandas. Miguel says no.

“But I knew the guy in charge,” he says. That contact was enough to allow him entrée into the tanda and allow him to feel confident that no one would rip him off.

Of course, there are Americans who are sick of people like Miguel and his 1000 Oceanside Oaxacans. They take American jobs, they soak up American social services, and if the flood of them is not turned back, they will overwhelm American culture.

But that story may be more about the past than the future. Little by little, a more up-to-date narrative is finding its way into media reports.

As Newsweek pointed out in 2010, most Americans are missing the truly current story of the Mexican immigration problem — that it has become short-term. Writer Arian Campo-Flores argues convincingly that Mexico will not be producing enough offspring to keep sending its young to the U.S. In fact, it has not been producing enough offspring for years: “The fertility rate in Mexico…has undergone one of the steepest declines in history, from about 6.7 children per woman in 1970 to about 2.1 today…. That makes it roughly equal to the U.S. rate….”

In fact, the inflow of Mexican immigrants may have reached its peak several years ago. In the year 2000, apprehensions of people attempting illegal crossings from Mexico was more than 1.6 million, while in recent years, even with improved methods and equipment for catching illegal crossers, such apprehensions have barely topped 600,000.

Apprehensions don’t tell the whole story, of course, but other indicators seem to point in the same direction. Fewer Mexicans are coming. Fewer Mexicans are being born per capita. The Mexican economy is in better shape than most other Latin American nations. And Mexico has relatively rosy prospects in the coming years.

The Mexican economy, with a gross domestic product in the $200–$400 billion range throughout most of the 1980s and ’90s is today more than $1 trillion and growing at a more than 5 percent annual rate.

According to a recent New York Times assessment, the economic slowdown and increased law enforcement in the U.S., combined with changed demographics and improved economic, educational, and political prospects in Mexico, have brought down the total annual increase in Mexican migrants to the U.S. to about 100,000 as of 2010. Some researchers insist that, as of 2011, the real number is zero.

The numbers work this way: slightly more than 400,000 Mexicans leave the U.S. year after year. That number changes very little. So, as the number of Mexicans taking up residence in the U.S. dropped to perhaps around 500,000 in 2010, the total increase of Mexicans in the U.S. for that year was just 100,000. If, when the figures come out from the Department of Homeland Security this summer, we find that the total influx in 2011 was in the 400,000 region, we’re finally at a net zero gain.

And the demographics suggest that we will never again see an influx from Mexico of the kind experienced over the past 30 years.

People have been saying for ages that illegal immigration was a “systemic” problem that could not be solved until the U.S. got serious about law enforcement and Mexico became able to take care of its own. Turns out, that’s exactly what happened.

It may take a few more years for most people to notice, and there are disasters or setbacks that could, at least temporarily, change the trend, but it is now likely that the great migration of Mexicans into the U.S. — which has been a central feature of U.S./Mexican relations for almost the entire post-war period — is past its high-water mark.

What that flood-tide will have left behind is two transformed nations.

For now, it’s left millions of Spanish-speaking, culturally out-of-water Mexicans needing institutions to help them function in a foreign land. (This is, of course, unless we decide to physically remove the Mexicans who are already here — a prospect no political party is currently supporting and would be too expensive.)

Whether the financial habits that Mexicans have brought into the U.S. will survive is an open question. The Mexican way of money may be dying out — even in Mexico.

Miguel says that things are changing in El Trapiche. In former days, farmers worked more cooperatively, maybe banding together to buy a tractor that they could share. Today tractors are more affordable, people have more money, and there is less sharing.

“As people get money, they don’t want to participate in the community stuff anymore,” Miguel says.

Perhaps as Mexico grows wealthier and more urban, communal financial arrangements such as tandas will fade away. A well-established middle-class Mexican may want no more to do with his neighbor’s finances than today’s middle-class American does.

Or, perhaps, the Mexican way of money will persist in some new and creative mode. Time will tell.

For now, tandas make it possible for Mexicans to become self-sustaining in America. Understanding how they work clarifies how a Mexican migrant is not just a lone fieldworker or a landscaper, but a member of a greater whole that puts down roots, builds communal bonds, and establishes systems and practices that bring something new and vital to the U.S.

Miguel, like many who migrated to the U.S. in those peak years, now feels a bit stuck. He hasn’t been to El Trapiche to visit his mother for ten years. He says he won’t cross the U.S./Mexico border illegally again. It has become too difficult and too dangerous.

Noting that he spent the first 14 years of his life in Mexico and the last 20 in the U.S., I ask him whether he considers himself a Mexican or an American. For a moment, he seems to stumble for an answer. The L&L Hawaiian Barbeque has filled up with families and noise. I hear a fairly even mix of Spanish and English.

“No sé,” Miguel says. Then, quietly, with a smile and a shrug, he says, “I don’t know.”

Here's something you might be interested in.

The tanda system of savings among Oceanside immigrants

Your gardener could be a banker

The tanda system of savings among Oceanside immigrants

Your gardener could be a banker

Miguel Herrero is just another Mexican.

Six days a week you might drive by him anywhere in the Carlsbad/Oceanside area. You’d see him building fences, planning drainages, wiring timers, and caring for trees. But the most interesting thing about him is what you can’t see.

In his off hours, Miguel is a community banker, an insurer of last resort, and a fixer of problems. A whole community turns to him for advice, and for money. There are even people deep in the Mexican state of Oaxaca, almost all the way down at the border with Guatemala, who give him a call when they have a personal problem, or when, say, the local church needs re-stuccoing but can’t afford the necessary scaffolding to do the job.

On his best day he might hit 5'6", even counting the virile mass of wavy black hair atop his head. He is a neat dresser. The day I meet him for an interview, he’s wearing a stylish black T-shirt with some kind of heavy-metal-looking skeleton design on it.

We meet at Oceanside’s L&L Hawaiian Barbeque. I have no idea why we’re meeting here, except that my brother, who has known Miguel for a decade and a half and who has agreed to translate, told me to show up at 4:30 on a Sunday afternoon.

The mall parking lot is half empty. Actually, a good part of the mall itself is empty. Not only empty of customers, but of tenants. The old Mervyn’s a few doors down from L&L just sits there, empty, month after month. The frozen-yogurt shop is gone. The Hallmark card shop is gone. So is the car dealership across the parking lot.

All over Oceanside, probably all over America, gaps have formed in consumer society. Dead spots. A lot of people are living through their own private financial hells.

Miguel is standing outside the L&L when I get there. My brother is late, so we go inside, order a couple of sodas, and talk in my poor Spanish and Miguel’s poor English about his financial work.

I ask what this money thing he does is called.

“Tandas [or] cundinas,” he says, “it’s the same thing.”

What word does he prefer?

“Tandas.”

He explains that, right now, he is in the second week of a 12-week tanda. Its structure could not be simpler — each member agrees to contribute $100 per week for 12 weeks. They will give the money to Miguel, who will hand it each week to one of the members. When the 12 weeks are over, a new tanda starts. Miguel says membership varies from 10–20 people each time.

Before the first week of each cycle, members choose numbers. The number chosen signifies the week the member will get paid $1100 (and will not have to contribute the weekly $100).

Members can buy one week, two weeks, even partial week arrangements such as one and a half weeks.

Some members ask for an early number, “because they need the money right away,” Miguel says. Such a request is perfectly acceptable.

“Some other people can wait to take their money,” he adds. Such a person can ask for a late number. The member might ask to go last, for example, so that each week constitutes, essentially, a payment into a 12-week savings plan.

In an emergency, a member can tell the group that he or she needs the money on any given week, and the group will rearrange paydays so that the member with the emergency can get paid immediately.

In this way, the tanda acts as a system of savings, of loans, and of insurance for emergencies.

Miguel says that, even if a person has already been paid in, say, week one, and they have an emergency in week nine, they can get paid again immediately, so long as they agree to give up their number in the next round.

“You know the people,” Miguel says. “It’s okay.”

Most of the people in Miguel’s tanda live in or near Oceanside’s Crown Heights neighborhood.

The tightly packed quarter is a short walk to the beach, to Oceanside High School, to the strip mall that has stood across from the high school for ages, and even to the new Fresh & Easy market on Oceanside Boulevard. There are plenty of spots nearby to shop and bank at, but a good percentage of the neighborhood’s banking goes on right here, just as a good percentage of the neighborhood’s shopping is done off the backs of trucks that park for hours along Division Street, or around the corner on Grant Street, down by the community garden.

For as long as there has been an Oceanside, this has been “the barrio” — one of those little Mexican hearts that beat near the center of nearly every beach city in Southern California. Once a seedy spot, Crown Heights today is mostly free of graffiti; the streets are clean and the sidewalks relatively busy. But the little houses and apartment buildings are much more crowded than is typical of Southern California.

You can get vegetables, baked goods, beverages, candies — almost the whole grocery array — off of those trucks. And you can get it without venturing out of Crown Heights, which is important if you don’t have a car or much English vocabulary.

Despite its outside reputation for crime, Crown Heights is a family place. Most of the small communities that make up the neighborhood are peaceful clusters of families, each with its own regional flavor.

Miguel’s flavor, like many people in Crown Heights, is Oaxacan. He figures there are probably 1000 Oaxacans in Oceanside.

If it seems odd that so many people from Oaxaca, one of Mexico’s southernmost states, would end up in Oceanside, one only has to understand a phenomenon that migration researchers call “sister communities.”

Dr. Ramona Pérez, director of the Center for Latin American Studies at San Diego State University, has worked in Oaxaca for two decades. She says, “You could go into any community in Oaxaca at this point and ask them, ‘Where’s your sister community?’ And they’ll say, ‘We go to Los Angeles,’ or ‘We go to San Diego,’ or ‘We go to Vista,’ or ‘We go to Chicago.’”

Many of these sister community relationships date back to the Bracero Program, a U.S. government program from the World War II era, in which Mexican laborers were given a chance to work in the U.S. while homegrown labor was off fighting in Europe or the Pacific. The program lasted until the early ’60s. Many Mexican participants put down roots in the U.S., later serving as helpers for family members and townsfolk who wanted to come to the U.S.

“Once you get a few people that have settled in an area and know the lay of the land, they serve as a hub for other people coming in,” says Dr. Pérez. “Some of them have been able to acquire linguistic skills. Where that doesn’t exist, they still understand transportation, they understand where jobs are, they know where healthcare is, they know where housing is, which landlords will allow them to come in with limited documentation, that kind of thing.”

In the past few decades, Miguel says, more and more Oaxacans have gone to Las Vegas, where they plant flowers and ferns around the big casinos in the morning, then tear out those same plants around midnight, when truckloads of new plants come and the daily cycle of dressing one of the hottest and driest cities in the world in a coat of tropical plants starts all over again.

But if you live in the town of El Trapiche, the people you know, the people you grew up with, they go to Crown Heights.

El Trapiche is a dirt-road farming town just off a sharp bend of highway about 40 miles south of Oaxaca City, which is, itself, about 1400 miles straight south of San Antonio Texas, or about 400 miles southeast of Mexico City.

I’ve never been there, but on Google Maps and Google Earth, El Trapiche compares to Oaxaca City, a city of about 250,000, in the way that Bonsall might compare to San Diego.

Before he first came to the U.S., Miguel was at one time a 12-year-old bull-riding champion from El Trapiche, winning prizes at rodeos all over the area. More than 20 years later, he recalls the bull-riding fondly, but, with three children, he says he would never get on a bull now.

When my brother arrives at L&L, we are able to get into a deeper discussion. I ask Miguel why members of his tandas don’t just go to a bank and start saving that way.

He doesn’t have much of an answer to this. In fact, the question seems, at first, to make little impression on him. In his view, it’s not that the Mexicans — and a few Guatemalans — who are in his tandas are afraid of the bank or unwilling to pay bank fees. They stay out of banks simply because banks are not something they are familiar with. They do not feel confident about walking into a bank, filling out a lot of paperwork that means nothing to them, and handing over their money to people they do not know and whose motives they cannot guess.

In the part of the world they come from, he tells me, loans are made by local patróns, rich men who loan money because they can make a tidy profit by making lots of small loans to their neighbors. And they know they can find you if you don’t make your payments.

“They act like it’s a favor to you,” Miguel says about these local patróns, “but they charge a lot of money.”

Are they like mafiosi, I ask him, searching for a word in my limited Spanish vocabulary, “bandidos”?

“No,” he says, kind of taken aback, they are just “patrones.”

So, without any inclination to walk into a bank, and with an already well-established habit of private financial dealings, many immigrants just naturally bank with Miguel, or with one of the many, many people who play a role like Miguel’s in immigrant communities (and even in some well-established Mexican-American communities) all around the U.S.

This kind of banking has a formal name among the IMF and World Bank types, it’s called ROSCAS: rotating savings and credit associations.

Academics have been studying such associations since the 1950s. The Global Development Research Center says they “can be seen in almost every society around the world, and have been in existence for a considerable period of time. They are flexible and adapt themselves easily to rural and urban peculiarities as well as existing community patterns of grouping/organizing. This flexibility is one reason for their worldwide popularity.”

Despite their informality and flexibility, or maybe because of it, rotating savings and credit associations are powerful little engines of economic activity, ingenious, really, in that they allow for people who either do not want to or cannot access established banking to make and get loans, to build up savings, to help out neighbors who may be facing an emergency, to keep community and family ties intact amidst a foreign culture, and even to maintain ties between members of a community like El Trapiche, who have come to the U.S., and those who have stayed or returned home.

Carlos Vélez-Ibañez wrote the book on these U.S.-based Mexican associations: An Impossible Living in a Transborder World. Part of his thesis is that the entire southwest of the North American continent is becoming one big, integrated economic region; the associations help facilitate the flow of goods and services within the region. They help Mexican nationals, who tend to be poorer and have less access to power, to function efficiently and effectively within this transnational economic reality.

His book is filled with academic jargon, and some Americans might categorize his thinking as the kind of squishy academic denial about border reality that has led to the lawlessness we now see along practically its full length.

For example, Vélez-Ibañez often puts the word “citizenship” in quotes, as if to suggest that the concept is less than real, a figment of the right-wing imagination, perhaps.

His research offers fascinating insights into a profound financial and social reality that, while it is literally right next to them, many Americans are oblivious to. Vélez-Ibañez suggests that this obliviousness to the financial ingenuity of Mexicans in America is part of a broad denial of the personhood and creativity of the Mexicans in our midst. But it could also be simply that linguistic barriers do not allow Mexicans in the U.S. to chat about these things with Americans.

The upshot of the Mexican habit of private, even secret, banking is that an individual who may appear to Americans as just another poor Mexican laborer is responsible, at any given time, for large sums of other people’s money and for facilitating the banking needs of families, clans, even whole neighborhoods.

Tandas may be the most common and obvious of the various off-the-radar financial tools available to Mexican immigrants, but it is only one among many.

Miguel, as a leader among the Oaxacans of Oceanside, provides an example of some other ways that Mexican financial interdependence works in the U.S.

He has made alliances with Americans who are willing to help poorer Mexicans. He has found Oceanside dentists, for example, who provide special rates to Mexicans lacking insurance. He has a well-off American business associate who sometimes puts up money, to be paid back in installments, when a member of the community needs help with an immigration issue or to get a car out of impound or some similar crisis.

Miguel, himself, now has the financial means to act as a patrón for families with medical bills or other sudden needs. And the entire Oaxacan community will help in a pinch by making lots of small donations, as they did when a Oaxacan family recently had a sick child who needed hospital care.

Back in El Trapiche, when the church needed that new stucco job, it was Miguel who got the call and organized the fundraising to pay for the scaffolding. Asked how he acquired this responsibility, Miguel smiles and shrugs innocently.

“He’ll never tell you how important he is in the community,” my brother says.

Miguel came north about 20 years ago, when he was 14. His family is a farming family, and during some of the dry years, the fertility of their land did not match the fertility of Miguel’s mother and father. They sent the boy north with an uncle, so that they could be sure he would eat.

The pair took a bus to Mexico City, a train to Mexicali, another bus to Tijuana, and made what was then a fairly easy crossing into the U.S.

In the U.S., the uncle got Miguel into a taxi and up to Oceanside, where he boarded with Oaxacan cousins.

He went to work for an Encinitas flower grower because he thought he would not only find steady work there, but also a chance to learn the business of horticulture. He moved from job to job, always getting both a paycheck and an education from his employers, until he was ready to start his own landscaping business.

Today he has eight employees.

Certainly, his intelligence and confidence make him an unusual person and have made much of his success possible. But he could not have made it to where he is on his own. Without a network to tap into when he came north, and without systems that aided in his financial success, there is no telling where he would be.

This habit of financial interdependence is what we might call the Mexican way of money, and, along with the many Mexican dishes that have become ubiquitous on American menus, it could be one of the lasting benefits Mexicans have brought into the U.S.

Some of the financial tools that Mexican families have at their disposal might, in fact, be the envy of many lone, struggling, and relatively financially isolated American households.

That is to say, financial cooperation and mutual assistance are far more the norm among Mexican immigrants than among Americans, and this cooperation and mutual assistance offers considerable benefits.

For many Mexicans, money troubles are community troubles. The community has, therefore, developed modes of helping people with money troubles. In contrast, an American with money troubles tends to become more isolated, putting up a brave public face while suffering and worrying alone.

Faced with the need to save and the need to have some insurance for emergency situations, Mexican men and women enter into rotating savings and credit associations together. They help each other save and make allowances for each other in emergency situations. Maybe this kind of thinking about money will one day be thought of as a contribution to American society, a prompt for Americans to be less isolated and more interdependent in terms of finances.

Since 2002, when he started sponsoring tandas for his community, Miguel has collected money hundreds of times, maybe thousands, and only twice has anyone failed to pay. In both cases, the person fled the area. Miguel called family members, seeking help in recouping the money, but none was able to help or to locate the absconders. In time, Miguel did find one of those who failed to pay, and the young man simply said, “I don’t have the money.”

So Miguel covered the losses himself. “As the person in charge, I didn’t get the money, so I had to pay it,” he says, seemingly without resentment.

Thus, no member of Miguel’s tandas, except Miguel himself, has ever lost money. It is this kind of personal responsibility that makes tandas go. “Confianza” — trust in the community — allows for a savings and credit market to be created and sustained.

Miguel says he has no need for tandas anymore; he runs the tandas because other people want him to. It is important that he do so because the trustworthiness of the tanda leader is an essential component of its success. For example, when Miguel was new to the U.S., he began participating in tandas. My brother asks him if he knew the people in the tandas. Miguel says no.

“But I knew the guy in charge,” he says. That contact was enough to allow him entrée into the tanda and allow him to feel confident that no one would rip him off.

Of course, there are Americans who are sick of people like Miguel and his 1000 Oceanside Oaxacans. They take American jobs, they soak up American social services, and if the flood of them is not turned back, they will overwhelm American culture.

But that story may be more about the past than the future. Little by little, a more up-to-date narrative is finding its way into media reports.

As Newsweek pointed out in 2010, most Americans are missing the truly current story of the Mexican immigration problem — that it has become short-term. Writer Arian Campo-Flores argues convincingly that Mexico will not be producing enough offspring to keep sending its young to the U.S. In fact, it has not been producing enough offspring for years: “The fertility rate in Mexico…has undergone one of the steepest declines in history, from about 6.7 children per woman in 1970 to about 2.1 today…. That makes it roughly equal to the U.S. rate….”

In fact, the inflow of Mexican immigrants may have reached its peak several years ago. In the year 2000, apprehensions of people attempting illegal crossings from Mexico was more than 1.6 million, while in recent years, even with improved methods and equipment for catching illegal crossers, such apprehensions have barely topped 600,000.

Apprehensions don’t tell the whole story, of course, but other indicators seem to point in the same direction. Fewer Mexicans are coming. Fewer Mexicans are being born per capita. The Mexican economy is in better shape than most other Latin American nations. And Mexico has relatively rosy prospects in the coming years.

The Mexican economy, with a gross domestic product in the $200–$400 billion range throughout most of the 1980s and ’90s is today more than $1 trillion and growing at a more than 5 percent annual rate.

According to a recent New York Times assessment, the economic slowdown and increased law enforcement in the U.S., combined with changed demographics and improved economic, educational, and political prospects in Mexico, have brought down the total annual increase in Mexican migrants to the U.S. to about 100,000 as of 2010. Some researchers insist that, as of 2011, the real number is zero.

The numbers work this way: slightly more than 400,000 Mexicans leave the U.S. year after year. That number changes very little. So, as the number of Mexicans taking up residence in the U.S. dropped to perhaps around 500,000 in 2010, the total increase of Mexicans in the U.S. for that year was just 100,000. If, when the figures come out from the Department of Homeland Security this summer, we find that the total influx in 2011 was in the 400,000 region, we’re finally at a net zero gain.

And the demographics suggest that we will never again see an influx from Mexico of the kind experienced over the past 30 years.

People have been saying for ages that illegal immigration was a “systemic” problem that could not be solved until the U.S. got serious about law enforcement and Mexico became able to take care of its own. Turns out, that’s exactly what happened.

It may take a few more years for most people to notice, and there are disasters or setbacks that could, at least temporarily, change the trend, but it is now likely that the great migration of Mexicans into the U.S. — which has been a central feature of U.S./Mexican relations for almost the entire post-war period — is past its high-water mark.

What that flood-tide will have left behind is two transformed nations.

For now, it’s left millions of Spanish-speaking, culturally out-of-water Mexicans needing institutions to help them function in a foreign land. (This is, of course, unless we decide to physically remove the Mexicans who are already here — a prospect no political party is currently supporting and would be too expensive.)

Whether the financial habits that Mexicans have brought into the U.S. will survive is an open question. The Mexican way of money may be dying out — even in Mexico.

Miguel says that things are changing in El Trapiche. In former days, farmers worked more cooperatively, maybe banding together to buy a tractor that they could share. Today tractors are more affordable, people have more money, and there is less sharing.

“As people get money, they don’t want to participate in the community stuff anymore,” Miguel says.

Perhaps as Mexico grows wealthier and more urban, communal financial arrangements such as tandas will fade away. A well-established middle-class Mexican may want no more to do with his neighbor’s finances than today’s middle-class American does.

Or, perhaps, the Mexican way of money will persist in some new and creative mode. Time will tell.

For now, tandas make it possible for Mexicans to become self-sustaining in America. Understanding how they work clarifies how a Mexican migrant is not just a lone fieldworker or a landscaper, but a member of a greater whole that puts down roots, builds communal bonds, and establishes systems and practices that bring something new and vital to the U.S.

Miguel, like many who migrated to the U.S. in those peak years, now feels a bit stuck. He hasn’t been to El Trapiche to visit his mother for ten years. He says he won’t cross the U.S./Mexico border illegally again. It has become too difficult and too dangerous.

Noting that he spent the first 14 years of his life in Mexico and the last 20 in the U.S., I ask him whether he considers himself a Mexican or an American. For a moment, he seems to stumble for an answer. The L&L Hawaiian Barbeque has filled up with families and noise. I hear a fairly even mix of Spanish and English.

“No sé,” Miguel says. Then, quietly, with a smile and a shrug, he says, “I don’t know.”

Comments