{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Wall Street Thrives on Main Street Pain

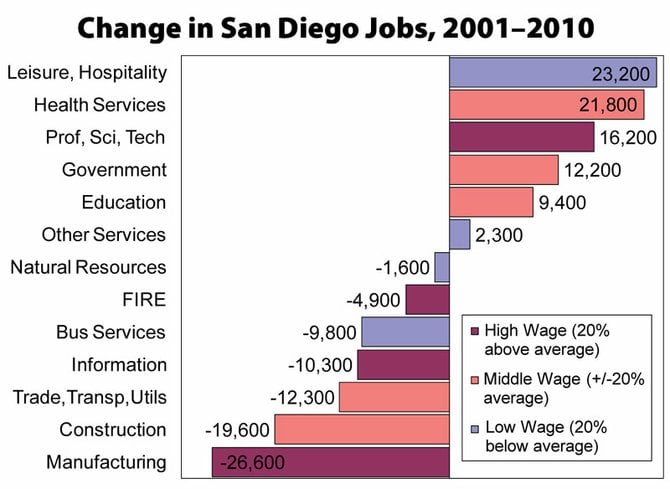

While tourism and health jobs increased over the past decade in

San Diego, manufacturing and construction jobs plummeted.

Over the past two years, the economy and stocks have generally gone in opposite directions. In the economy, we have suffered the steepest downturn and the weakest recovery since the Great Depression, but since early 2009, stocks have doubled.

In short, stocks have zoomed as the economy sputtered — or because it sputtered. As statistical measures of the economy sagged, the Federal Reserve, our central bank, kept handing money to banks at 0 to 0.25 percent interest and using other techniques to flood the financial system with money and credit. Hedge funds borrowed from the banks at very low rates and gobbled up stocks. Other institutions, including the banks, did the same.

Thus, Wall Street thrived because Main Street starved. Ben Bernanke, head of the Federal Reserve, even said that the Fed’s nostrums were working: one index of highly speculative stocks had soared, he boasted. Huh? The Fed is supposed to worry about keeping inflation and unemployment low. Now it wants to keep stocks high. Trouble is, the economy has to stay weak to give Bernanke an excuse to keep short-term interest rates near zero. That’s been the market’s propellant.

In late June, the Fed mournfully predicted that the American economy will grow by only 2.7 percent this year. Just two months earlier, the Fed had pegged growth at 2.9 percent. Similarly, a gloomier Fed said in late June that the unemployment rate would be 7.8 to 8.2 percent this year — far worse than the bank’s April forecast of 7.6 to 7.9 percent.

So, following these dolorous predictions, the stock market soared upward, gaining more than 5 percent that week, although there were other factors involved. What happened is that the Fed had given a covert signal to Wall Street: “Let ’er rip, boys and girls!”

Bernanke has stressed for a considerable time that as long as unemployment remains high, he will keep interest rates around zero. Wall Street would much rather have low interest rates than a healthy consumer. Bad economic news is good investor news: the Fed will keep the spigot flowing. What’s more, companies are not hiring, so as unemployment stays high, profits boom — also boosting the stock market.

Action on Friday, July 8, made the point. Early in the day, the government reported that the economy had had almost no job growth in June; the unemployment rate had gone up. Stocks initially plunged, but by day’s end, they had sliced their losses by well over half and were up for the week: the pros knew that Uncle Ben Bernanke would squirt more liquidity their way.

There is general agreement that the Fed’s $600 billion program to buy Treasury paper boosted stocks but not the economy. In late June, the Fed ended that purchasing program, but it said it would continue buying Treasury paper — about $300 billion worth over a year. That was a liquidity signal: Bottoms up! On July 13, the market celebrated when Bernanke said he was ready to roll out his water hose if the economy suffered. The next day, he seemed to back away from the commitment, and stocks wilted.

Generally, rich people make spending decisions based on how their stocks and bonds are doing. But the richest 10 percent has 70 percent of financial wealth (stocks and bonds); the lower half has a mere 5 percent. Most people plan their consumption around the value of their homes. Those values are down more than 30 percent nationwide, 38 percent in San Diego. Families are no longer borrowing off the equity in their homes.

Meanwhile, banks are lending only to the chosen few. “High-net-worth individuals are able to receive loans, but lower-net-worth individuals are still struggling,” says Bank of America Merrill Lynch. And the middle/low-income folks are getting almost no return on their savings accounts.

Jim Welsh: household debt

is soaring

Even with the economy seemingly getting stronger, people won’t do much borrowing. North County investment advisor E. James Welsh notes that between 1985 and 2008, household debt as a percentage of disposable personal income (spendable money after taxes) soared from 62 percent to 135 percent. Last year it dropped to a still-scary 120 percent, mainly because of defaults on mortgages, credit cards, and auto loans.

Arthur Lipper: tide not lifting all boats.

The bottom line: these years of Wall Street feasting off Main Street’s misery have caused severe long-term afflictions. “We are past the point of a high tide lifting all boats and are increasingly in a zero-sum game of what’s good for one group is bad for another,” says Del Mar’s Arthur Lipper III, a member of one of Wall Street’s most famous families and an international investment banker. “The chasm between the haves and have-nots is widening.”

That’s bad: consumer spending is more than 70 percent of the economy. But Lipper sees another ominous threat resulting from the wealth and income disparity: “There is a widening educational gap,” he says, lamenting “the undereducation of our younger workforce and high school students.” Countries that compete with the United States have “a better educated and more highly motivated workforce.” Long-term, that is a threat to America’s hegemony. Domestically, “Nothing good can come from the shrinking of our middle class.”

W. Erik Bruvold, president of the National University System Institute for Policy Research, points out that in America today, 74 percent of people with college degrees are employed, while only 54.6 percent of high school grads have jobs. In San Diego, workers in life sciences, clean technology, and wireless telecom — generally better educated — have suffered only “mild discomfort” in the post-2007 economy, while others have been reeling.

Between 2001 and 2010, San Diego gained 23,200 jobs in leisure and hospitality — hotel and restaurant jobs, for example. This was the biggest employment rise in the county, but the pay is 20 percent or more below average. By contrast, manufacturing jobs declined the most: 26,600. These are high-paying jobs — at least 20 percent above average.

The only high-paying sector that gained jobs between 2001 and 2010 was professional, scientific, and technical, the ones generally requiring the most education. This category gained 16,200 jobs. One of San Diego’s main tasks is seeing that growth in tech industries benefits those without college degrees, says Bruvold.

Should you ignore the debilitating rich/poor gap and invest in stocks? You can buy solid ones — mainly utilities — that pay good dividends (yields of more than 4 percent, or much better than in bonds or savings accounts). But there are good arguments against stocks, too — such as the possibility of a crash in Europe and/or the United States. Lipper points out that stocks go up most of the time, but when they come down, it’s often hard and fast. Since Wall Street moguls get paid big bucks whether they perform or not, the moneybags have a bad case of complacency, just as they had in precrash 2007.

I would not have more than 30 percent of my portfolio in stocks — about the same percentage, incidentally, that the superrich devote to stocks, according to Merrill Lynch. Your broker or advisor will probably want you to have 60 percent in equities; that’s too much.

Here's something you might be interested in.

Wall Street Thrives on Main Street Pain

Wall Street Thrives on Main Street Pain

While tourism and health jobs increased over the past decade in

San Diego, manufacturing and construction jobs plummeted.

Over the past two years, the economy and stocks have generally gone in opposite directions. In the economy, we have suffered the steepest downturn and the weakest recovery since the Great Depression, but since early 2009, stocks have doubled.

In short, stocks have zoomed as the economy sputtered — or because it sputtered. As statistical measures of the economy sagged, the Federal Reserve, our central bank, kept handing money to banks at 0 to 0.25 percent interest and using other techniques to flood the financial system with money and credit. Hedge funds borrowed from the banks at very low rates and gobbled up stocks. Other institutions, including the banks, did the same.

Thus, Wall Street thrived because Main Street starved. Ben Bernanke, head of the Federal Reserve, even said that the Fed’s nostrums were working: one index of highly speculative stocks had soared, he boasted. Huh? The Fed is supposed to worry about keeping inflation and unemployment low. Now it wants to keep stocks high. Trouble is, the economy has to stay weak to give Bernanke an excuse to keep short-term interest rates near zero. That’s been the market’s propellant.

In late June, the Fed mournfully predicted that the American economy will grow by only 2.7 percent this year. Just two months earlier, the Fed had pegged growth at 2.9 percent. Similarly, a gloomier Fed said in late June that the unemployment rate would be 7.8 to 8.2 percent this year — far worse than the bank’s April forecast of 7.6 to 7.9 percent.

So, following these dolorous predictions, the stock market soared upward, gaining more than 5 percent that week, although there were other factors involved. What happened is that the Fed had given a covert signal to Wall Street: “Let ’er rip, boys and girls!”

Bernanke has stressed for a considerable time that as long as unemployment remains high, he will keep interest rates around zero. Wall Street would much rather have low interest rates than a healthy consumer. Bad economic news is good investor news: the Fed will keep the spigot flowing. What’s more, companies are not hiring, so as unemployment stays high, profits boom — also boosting the stock market.

Action on Friday, July 8, made the point. Early in the day, the government reported that the economy had had almost no job growth in June; the unemployment rate had gone up. Stocks initially plunged, but by day’s end, they had sliced their losses by well over half and were up for the week: the pros knew that Uncle Ben Bernanke would squirt more liquidity their way.

There is general agreement that the Fed’s $600 billion program to buy Treasury paper boosted stocks but not the economy. In late June, the Fed ended that purchasing program, but it said it would continue buying Treasury paper — about $300 billion worth over a year. That was a liquidity signal: Bottoms up! On July 13, the market celebrated when Bernanke said he was ready to roll out his water hose if the economy suffered. The next day, he seemed to back away from the commitment, and stocks wilted.

Generally, rich people make spending decisions based on how their stocks and bonds are doing. But the richest 10 percent has 70 percent of financial wealth (stocks and bonds); the lower half has a mere 5 percent. Most people plan their consumption around the value of their homes. Those values are down more than 30 percent nationwide, 38 percent in San Diego. Families are no longer borrowing off the equity in their homes.

Meanwhile, banks are lending only to the chosen few. “High-net-worth individuals are able to receive loans, but lower-net-worth individuals are still struggling,” says Bank of America Merrill Lynch. And the middle/low-income folks are getting almost no return on their savings accounts.

Jim Welsh: household debt

is soaring

Even with the economy seemingly getting stronger, people won’t do much borrowing. North County investment advisor E. James Welsh notes that between 1985 and 2008, household debt as a percentage of disposable personal income (spendable money after taxes) soared from 62 percent to 135 percent. Last year it dropped to a still-scary 120 percent, mainly because of defaults on mortgages, credit cards, and auto loans.

Arthur Lipper: tide not lifting all boats.

The bottom line: these years of Wall Street feasting off Main Street’s misery have caused severe long-term afflictions. “We are past the point of a high tide lifting all boats and are increasingly in a zero-sum game of what’s good for one group is bad for another,” says Del Mar’s Arthur Lipper III, a member of one of Wall Street’s most famous families and an international investment banker. “The chasm between the haves and have-nots is widening.”

That’s bad: consumer spending is more than 70 percent of the economy. But Lipper sees another ominous threat resulting from the wealth and income disparity: “There is a widening educational gap,” he says, lamenting “the undereducation of our younger workforce and high school students.” Countries that compete with the United States have “a better educated and more highly motivated workforce.” Long-term, that is a threat to America’s hegemony. Domestically, “Nothing good can come from the shrinking of our middle class.”

W. Erik Bruvold, president of the National University System Institute for Policy Research, points out that in America today, 74 percent of people with college degrees are employed, while only 54.6 percent of high school grads have jobs. In San Diego, workers in life sciences, clean technology, and wireless telecom — generally better educated — have suffered only “mild discomfort” in the post-2007 economy, while others have been reeling.

Between 2001 and 2010, San Diego gained 23,200 jobs in leisure and hospitality — hotel and restaurant jobs, for example. This was the biggest employment rise in the county, but the pay is 20 percent or more below average. By contrast, manufacturing jobs declined the most: 26,600. These are high-paying jobs — at least 20 percent above average.

The only high-paying sector that gained jobs between 2001 and 2010 was professional, scientific, and technical, the ones generally requiring the most education. This category gained 16,200 jobs. One of San Diego’s main tasks is seeing that growth in tech industries benefits those without college degrees, says Bruvold.

Should you ignore the debilitating rich/poor gap and invest in stocks? You can buy solid ones — mainly utilities — that pay good dividends (yields of more than 4 percent, or much better than in bonds or savings accounts). But there are good arguments against stocks, too — such as the possibility of a crash in Europe and/or the United States. Lipper points out that stocks go up most of the time, but when they come down, it’s often hard and fast. Since Wall Street moguls get paid big bucks whether they perform or not, the moneybags have a bad case of complacency, just as they had in precrash 2007.

I would not have more than 30 percent of my portfolio in stocks — about the same percentage, incidentally, that the superrich devote to stocks, according to Merrill Lynch. Your broker or advisor will probably want you to have 60 percent in equities; that’s too much.

Comments