{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

San Diego brokers on Wall Street

"Pick one stock and watch it”

Monday, July 22, 2002, 9:38 a.m. The Dow Jones Industrial Average is down 284.52 points to 7734.74. I push on a glass door and enter into a small lobby. This is the downtown Charles Schwab office, located on the corner of Fifth Avenue and A Street. Sitting behind a circular counter is Warren, the receptionist. He looks to be in his mid-30s, with dark hair and a ruddy, clean-shaven face.

Set next to a bank of windows facing A Street are five chairs and an end table. Against the opposite wall, inside semi-private cubicles, are two computers. A man stands in front of each computer, or, more precisely, crouches in front of each computer. Two keyboards click-click-click as the pair retrieves stock quotes. Sometimes in unison, sometimes alternating, the men exhale an “Oh” or an “Ah,” followed by another gush of keyboard clicks.

“How long have you been in the market?”

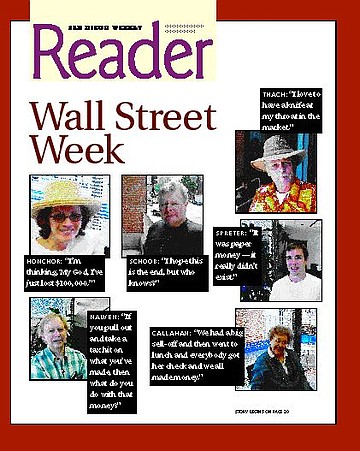

“About ten years.” Speaking is Jeff Spreter, 23, five foot ten, 175 pounds, with recently trimmed brown hair, dressed in a white cotton T-shirt and jeans.

“Did you see this coming?” “This” being the recent 2500-point drop in the Dow.

“I kind of saw it falling apart, but not to this extent.”

Spreter lives in Coronado and graduated from San Diego State this year. “How much money have you lost?” Might as well get right to it.

“Probably 15 [thousand dollars].” Spreter does not flinch.

Mere collateral damage. “Do you ever think about what you might have done with that money?”

“Not really. It was paper money — it really didn’t exist.”

Spreter tells me he’s studying for law school. I flee from the topic. “Have you changed your plans about vacations or purchases?”

“Not really.”

“Was there one particular stock that trashed you more than others?”

Spreter laughs. “Oh, yeah, Enron and Global Crossing.” Now we both laugh. “I bought them at $8…”

Enron is selling for 9 cents today, down from $90.75. Global Crossing is bid 5 cents, down from $64.25. “Have you ever taken classes about the stock market?”

“Yeah, I’m a finance major. I just graduated.”

Okay, here we are: free, qualified advice. “What’s your take? How long is this slide going to last?”

“There’s psychological support, maybe, at 7500, 6800.”

I do not feel comforted. “How much money do you have in the market today?”

“About $20,000.”

“So, being young, you’re not worried?”

“I make $400 a year on GE dividends, so I’m not too worried.”

I hate young people. “Where would the market have to go before you started to sweat?”

“Oh, 6500, 6800. That would be ugly.”

It’s 9:58 a.m. and the Dow is down 232 points.

A short — five-foot, six-inch, say — 35-year-old man with curly red hair, horn-rimmed glasses, and an expression of eternal displeasure, is huffing and puffing in front of a computer monitor. He makes a loud grunt, throws up his hands, and stomps out the front door.

I catch up, introduce myself, and ask, “How long have you been in the market?”

The man answers using a stage whisper, so no one can overhear, yet everyone will understand he is saying something important. “Twelve years.”

“Did you see this coming?”

“Yeah.”

“Have you been selling short and making money?”

The short guy nods his head, looks over his shoulder to see if anyone is coming out of the Schwab office. I figure the guy for a short seller. Typically, a short seller borrows, say, 100 shares of Microsoft from his broker, betting that Microsoft will drop, let’s say, $10. He then sells those shares on the open market. Let’s say Microsoft cooperates and drops $10. Then the short seller buys 100 shares on the open market and uses them to replace the stock he borrowed from the broker. He pockets the difference between the price at which he sold and the price at which he bought, minus commissions, interest, and every other fee the broker can dream up.

Short selling is one of those legal but culturally disapproved of activities, like selling tobacco to retarded, pregnant teenage girls. You’ll never see a newspaper headline scream, “Dow Down 500 Points, Great Day for Short Sellers.” When the market is going up, you’ll never see interviews with short sellers who have lost their homes and life savings. There is a cultural bias, one pushed hard by the stock market–industrial complex, to root for the home team, home team being defined as a stock market going up.

But if you believe, and a lot of people do, that the stock market is casino gambling all the way down to the fat house edge, then being a short seller is just another way to play the game. Here’s the weird part: even knowing this, short sellers, in the backs of their minds, believe they’re doing something wrong. And so, short sellers, like gamblers everywhere, speak in whispers and look over their shoulders. In fact, short sellers, as a rule, look like this fellow, they look like they’re doing something illegal.

I say softly, so as not to ruffle delicate psyche feathers, “You’ve been selling short. You must be having a good time?”

“I’m having a good time.”

I detect not a single nuance of pleasure in his voice. “When did you recognize that the fall was coming?”

“About two years ago.”

“You’ve been selling short this whole time?”

“Yes.”

Again, not a flicker of satisfaction in his voice. “Can you give me a hazy figure of your winnings? Have you made $1000 or $100,000?”

“I don’t think that’s relevant.”

“What is more relevant?” The short, short seller’s face freezes in an expression of outrage. No gambler will tell the truth about his winnings or losings. Indeed, it is a terrible breach of etiquette to solicit personal information. I hurry forward. “I take it you don’t worry about the stock market?”

“Not at all.”

“Do you worry it might go up?”

“No, I’m in cash now.”

I should mention that short sellers tend to be smart, which doesn’t mean they can predict the future better than anyone else, only that they can talk about the future better than most. We’ll come back to the short seller after a while.

The lobby is empty save for Warren and me. I put down Schwab’s copy of the Wall Street Journal and inquire, “Are people calling in sounding genuinely distressed?”

“A lot of people are very concerned about where the market is heading. Especially compared to where they were one year ago, six months ago. Definitely.”

“Have you heard panic?”

“People are coming in and saying, ‘I need to sell everything right now.’ ”

That’s a long way from panic. “I was visiting Washington, D.C., in ’87 when the Dow dropped 508 points in one day, except then, 508 points was 22 percent of the Dow. That morning, I went to the Schwab office on I Street. You couldn’t telephone. Schwab had so many phone calls, their switchboard imploded. When I arrived, there must have been 50 people milling around on the sidewalk trying to get in the front door. Women were crying. People who had made it inside the lobby couldn’t see a broker. It was…”

“No, it’s not that bad.” Warren smiles as if I’ve been explaining how covered wagons are built. “The closest I’ve seen to that is a 10-, 15-minute phone wait to get through to a broker.”

“How long have you been in the market?”

“About four or five years,” says Steve Schoob, a truck driver from Cottonwood, Arizona. Schoob’s in town visiting his parents and stopped by to check his stocks. I ask the usual. “Did you see this coming?”

“The guy who sells to me did.” Schoob is wearing a navy blue T-shirt, jeans, and a huge silver necklace with what, I swear, looks to be a trout fish lure minus the hook as a pendant. “We’re in electric and water stocks and all that stuff now. We didn’t get hurt bad, but we’ve lost some.” Schoob thinks for a moment. “I’ve got a friend who’s $1,500,000 down.”

Hey, it’s only paper money. “Have you reconsidered any plans or purchases?”

“Nope, not at all.”

I believe him. “How did you first come into the market?”

“Bank of America. Through mutual funds. Then I started getting into it more.”

Captain Crunch breakfast cereal, Coca-Cola, marijuana, heroin, and then the stock market. It’s a straight line to hell in a handbasket. “Is this the beginning, middle, or end of the bear market?”

“I hope this is the end, but who knows?” Schoob makes a cowboy shrug. “It might go a little bit lower.”

“Do you ever worry about the market?”

“Heck, no.”

“Have you spent any time studying the market, researching it?”

“Not really. I have a friend who does that for me. I just give him money and he takes care of it. This guy really studies the market and we’ve made money.”

There is, at the end of the day, no argument to that. “What do you think caused the Dow to crash?”

“I think 9/11 had something to do with it. And all the executives taking off the top.”

I note a trace of cowboy anger. “What should be done with them?”

“I hope they hang them. I think they should be hung.”

10:28 a.m. and the Dow is down 168 points.

“How long have you been in the market?”

Joe Nalven says, “Since the early ’70s.”

Mr. Joe Nalven is middle-aged and could pass as a twin of Senator Joe Lieberman, if, that is, Senator Joe was born with blond hair and raised on the West Coast. Citizen Joe lives in Poway. I ask, “What got you started in the market?”

“My in-laws thought it would be a good place to put extra money from time to time.”

“What was your first stock?”

“Warner [one of the sires of AOL Time Warner] and General Motors.”

“So you’ve seen this before?”

“Oh, yeah, the cycles of depression and elations are quite familiar.”

“Where are we along the axis of despair and joy?” Pretty damn poetic question.

“I’d like to believe, and I think all of us are hedging our bets, but I’d like to believe we’re near a low.” I note Joe speaks like Joe Lieberman. “Looking at the overall robustness of the economy, it doesn’t make sense to be this low. But, then again, listening to the news, the highs weren’t probably where we ought to have been either.

“The big question is, if you pull out and take a tax hit on what you’ve made, even if it was not as much as you would like to have made, then what do you do with that money? Do you put it in your mattress? The market forces you to balance risk in a number of different ways. And that’s suddenly one of the problems we have now, because it’s hard to gauge the kind of risk we’re in.”

Nalven poses a question many of us need not answer since one is not required to pay taxes on losses, only on gains. I say, “The Dow P/E is over 20, indicating to people who believe P/Es are important that the stock market is still overvalued.” P/E, or price-earnings ratio, is the price of a stock divided by its earnings per share. For instance, a $60 stock price divided by $3 of earnings per share gives you a P/E ratio, or P/E, of 20.

Nalven isn’t buying. “But you have other stocks, like Microsoft, which has always had a P/E in the 30s, 40s, and 50s, and it’s held its ability to grow. Still, the market may force us to go more towards value.

“Where is the real value in putting your money in the stock market?” Now he really sounds like Joe Lieberman. “Say you hold Johnson & Johnson. Well, that’s a good stock. And I emphasize good stock. And now you read about how they are having accounting problems. If bedrock firms start having problems, how do you make sense of that? What’s real?”

Theft and fraud. “What do you think ought to be done with Enron and WorldCom executives?”

“I think jail is a very good place. We need to ramp up the integrity of the marketplace. If self-policing were okay, we wouldn’t need a police force.” Nalven stops for a breath. “I’m an attorney. I represent people. I have a skeptical view on human nature. I’m an anthropologist as well. So on two counts I’m very skeptical about human nature. What we see now is more punishment as a way to make the marketplace more secure, but, then again, is that really a guarantee? We trade one illusion for another.”

Yes, well, maybe, perhaps. “Let me have your stock tip of the day.”

“I often listen to Bill Holland on the radio, and he’s saying the stock market is going to go with the rest of the country. If the country is going to go in the tubes, then what’s the point of having stocks anyway?”

Sitting military straight, in the far chair, is a nervous, pensive-looking man. I assume he’s waiting for an appointment. The man has a smooth oval face and pursed lips and is bald save for a streak of cropped gray hair above his ears. I say hello. We chat a bit. I learn he’s here to put money into the market. His name is Craig Christiansen. He’s been working as a transportation assistant on North Island and lives in Normal Heights.

Christiansen says, “I don’t know anything about investing or nothing. I’m kind of the, what do you call it, the green…things are green, or whatever they call it when you’re new at something.”

“Greenhorn?”

“Yeah.” We laugh. Christiansen says, tentatively, “I have to withdraw this money by August 23. I guess I retired at the wrong time. What they tell me to do is open an IRA, which is the only thing my 401(k) can do. It’s going to be a rollover-type IRA. My dad’s been saying, ‘We’ll just keep it in a money market right now, and when this market gets better we’ll see about stocks and bonds and all that.’ ”

I ask, “Has your 401(k) lost money?”

“Lost $1000 in a month.” Christiansen is suddenly decisive. “My ending balance in May was $42,000, and my ending balance in June was $41,000.”

“That’s not bad, to be only $1000 down.” In fact, that’s a better record than anyone I know.

“No, it’s not. But, see, that’s government bonds and stock. But now I have to take it out by August 23, because the system is going over to a new computer and I don’t want to wait, and who knows what might happen with a new computer system? So I’m trying to get it done now.”

Either he knows a great deal about computers or he knows nothing about computers. “Well, you’re maintaining your capital. A lot of people have lost a lot of money.”

“My dad said he’s lost some, but not a lot. He keeps telling me about diversification, because you have to put the money in different spots.”

“Have you studied the market?”

“No, I haven’t. In fact, I’m one of these who would rather have someone else do it for me. I can’t balance my checkbook, let alone anything else.”

I can feel sharks circling. “Do you worry about the stock market and what might happen?”

“Well, right now, I’m kind of worried, but I’m not in it yet. I didn’t worry about it when I was working. But now that I have all this money, I need to find a place, someplace where it will get me more bang for my buck.”

Christiansen leans toward me. “This has to last. I’m a young retiree with a disability. I need this money for when I get older, because I’m not a normal retiree who retires at age 62 or whatever. I am retiring at 43. My retirement will be a lot longer. This 40-some thousand has to last me, because I have nothing else except for the annuity I get for my disability.”

One bad break would cost $40,000. Easy. “What’s wrong?”

“Diabetic neuropathy. I have no feeling from my knees down. Losing it in my hands as well. Now I’m stuck on the bus. I can’t drive anymore.”

And again. “How long have you been in the stock market?”

“Over 30 years. I belonged to an investment club.”

I’m talking to Helen “My mother gave me a short name in case I had bad handwriting” Callahan. Mrs. Callahan is a happy-looking woman in her 70s. I make her for five foot six. She has curly auburn hair, an easy smile, and wonderful laugh lines around her eyes. I ask, “Are you in a fund or individual stocks?”

“Individual stocks.”

“How is that going?”

“I don’t know. I don’t care. I don’t look. We don’t need the money now. If you don’t need the money, your losses are only on paper. I spoke to my daughter in Berkeley last night. She said, ‘Mom, I’ve lost $10,000.’ I said, ‘Nancy, that’s only on paper. Wait, it will go up.’ And it will go up.”

Nobody has actually lost money. I ask, “Are you continuing to buy stocks?”

“No. He [Callahan nods to her husband in the next chair] is going to be 80, I’m 79, and there’s not enough money to buy.”

Helen was trained as a nurse. “I graduated from the Columbia Presbyterian School of Nursing in New York, but I never worked. My husband was a single-engine carrier pilot in the Navy. And then he had his own tax and bookkeeping business. We’ve lived in Coronado for 40 years.”

Sounds quite pleasant. “When you were in the investment club, did you study the market?”

“We never bought anything if it didn’t go through our study group. We never took more than 20 people in the club, all women in the club. We used to have meetings once a year. We disbanded two years ago.”

“How come?”

“Because we were old, we were tired, and the market was high. We’d been going on for 30 years. We got down to 15 members — people had died, moved away. We decided to disband. That was 2 years ago. We had a big sell-off and then went to lunch and everybody got her check and we all made money.”

“Nice going.” Exactly two years ago the Dow closed at 10,733.

“How are you doing in the market?”

“I’m frustrated,” says Norbert Seufert, a tall, red-faced, blond-haired man with linebacker shoulders and a fighter’s chest. “I’m still hopeful that in time, things will turn around. There have been nine recessions since WWII and nine recoveries, so I’m trying to be mindful of that. I have to imagine that there is only so much further it can go down.”

“Have you seen a bear market before?”

“Indirectly. My parents have been in the market for an awfully long time. I guess the ’70s was, essentially, a bear market, going nowhere for ten years, but not like this.”

“Have you gotten hurt yet?”

“I’m deeply in the red, yes. My parents are heavily invested in blue chips. I’m an only child, so I know that one day those stocks will make their way over to me through inheritance. I’ve recognized that tech is, probably, our future, so I’ve been heavily invested in tech. I’ve obviously taken quite a beating. I owned bellwether techs and that hasn’t protected me.”

Today, Intel will close at $18.26, down from an August 31, 2000, close of $74.875. Oracle will close at $9.23, down from a March 27, 2000, close of $44.218. “How low can Nasdaq go?”

“Well, I’m 40 now — maybe 25 years until things turn around.” Seufert laughs. “A lot sooner than that. I’m hoping within the next two or three years. I can’t imagine who’s selling at these levels.”

“You said you are in the red. Are you on margin?”

“I am on margin. I thought Intel, with a dip, would be a brilliant buy. I’ve seen it dip another 50 percent since that point, so…”

I wince. “What caused the market to drop?”

“Obviously the accounting scandals. There’s a hysteria that feeds on itself. I am someone who fancies himself as a long-term investor, and even I have had thoughts of ‘Well, let’s sell and salvage something.’ But now I am of a mind to say, ‘I think, maybe, this represents a better buying opportunity than has ever presented itself in the past 15 years.’ ”

I do not reach for my wallet. “How much time per day do you spend studying the market?”

“Anywhere from 15 minutes checking Yahoo Finance, to two hours reading publications like Business Week and Smart Money, trying to get a handle on which moves I ought to be making.”

“Do you think anybody knows where the market will go?”

“That’s very interesting. We’ve heard stories about analysts who were promoting a stock heavily at 40 and who are now telling you to sell it at $3. You have to wonder if anybody did know. If someone knew, then there’d be a formula for success and then everybody would be on board. Then it would no longer be a formula for success.

“Having been an investor now for close to 20 years, you want to know what your money is doing. You can’t rely on other people, necessarily, to manage your money. A lot of very smart mutual fund managers have taken a critical beating. So who’s to say? And market psychology is not something anybody can get their hands on. It’s mass psychology. You have to recognize that nobody truly knows. You make as educated a guess as you can.”

This is called investing. “Did you see the slide coming?”

“Obviously not. There was a point when it started to dip. It dipped 10 and then 15 percent. But unless it hits a 28 percent dip, I’d take a tax hit by selling and buying back into it. So, even when the dip started, I felt like it was just a correction.

“I can tell you, from personal experience, that business publications were not telling everybody, ‘This is the start of something very big.’ They were saying, ‘Hey, here’s a little dip, it’s a buying opportunity.’

“Well, that dip was Nasdaq at 4000 and the next dip was Nasdaq at 3000. Now we’re seeing Nasdaq at 1200 and change. Nobody’s been predicting this dip in all the publications I’ve been reading, and I’m pretty well read in the subject.”

The media as responsible adult. “Has the crash caused you to defer any purchases?”

“Absolutely. Not buying a new car. Not remodeling our house. Making travel a little more modest than I might have otherwise.”

“What do you do?”

“I’m in advertising.”

There is a period of impolite quiet. Finally, I ask, “Do you have a stock tip?”

“I’ve been buying Elan Pharmaceuticals, because I’ve been reading about them for four years and everybody talks about what a terrific company it is. They’re in the space of making generic drugs, and I know, with the graying of the population, drugs are gonna make out. I have to imagine that that company has been hurt more than it deserves.”

Elan will close today at $1.84, down from the August 13, 2001, price of $57. “Do you have a favorite stock horror story?”

“I’d have to say buying Intel on margin at $49. I bought a couch that I felt was too expensive. I said to myself, ‘Okay, let me take a big margin position in Intel, and when it goes back up two points, I’ll sell and make $2000 profit. That way I can buy the couch for what I think it was really worth.’ Now I’m sitting on Intel at $19 and, every night, sitting on a $35,000 couch.”

“I’ve been in the market since 1953.”

Speaking is Richard Wright. It’s Wednesday morning, July 24, and I’m back in the window chair at Schwab’s. I ask, “Did you see this coming?”

Wright, who looks like a tall Ernest Hemingway without the egomania, answers, “Yes, I was pessimistic a year ago.”

“How about two years ago? What did you think about the market then?”

“Techs started crumbling two years ago, but the Dow was still going strong, as if it were business as usual. I didn’t see any downward forecast from the media. They didn’t talk about earnings, didn’t talk about the solidness of stocks.”

Media as responsible adult, part II. “When you saw the Nasdaq go, did you take defensive measures?”

“I did, but not enough. I had options that went south on me. I should have cashed them in at the time. I had a large block of options in Unisys. It fell apart about a week before they were due.”

“Have you had to cut back on any plans, vacations, purchases?”

“No, because the money I used was discretionary money. I never got into my personal assets.”

“So you were playing with house money?”

“Exactly.” Wright smiles like a man who just got something for nothing.

“Which stocks are you in now?”

“Lucent. I just picked up some Lucent and I’m looking at a health-care stock. I like that one and GE.”

(As I write this, GE is selling for $32.05, up from $23.02, its price at the time of this conversation.) “You said you started in the market in 1953, almost 50 years ago. What was your first stock?”

“I was 20-some years old. My barber told me about penny stocks from Canada. I got into the stock market then. I had a Merrill Lynch, Pierce, Fenner and Bean account. Remember those days?”

I don’t. I nod yes. “How did you do?”

“It went up a couple of pennies. I thought I was in heaven.”

Wright tells me that three or four years ago he was a swing trader. Says he took classes in swing trading and day trading up in Orange County. I ask, “What did you learn?”

“The instructor’s message, frankly, was to stay out of techs. He said stocks undulate; read the undulations and play them. He also told us we were competing with the big boys who were doing the very same thing.”

Nothing to it. “I’ve read stories that say 90 percent of day traders lost money.”

“Oh, I can believe that.”

“What separated you from them?”

“You lose money for a while and then you learn not to make those same mistakes again. Then you start making money and that’s where I was. When I hung up my spurs, I was making money, but I paid the price. The price is, you let your emotions take over and make a purchase and then you shoot your toe off.” Wright laughs. “Now you only have nine toes left.

“Pretty soon, you say, ‘All right, I’m done doing that. I’m just going to use the old formula. I’m going to use the mechanics of it. I’m going to read the charts. I’m going to read the news. I’m going to get up at four in the morning and do all the research.’ Even then, you get the rug pulled out from underneath you by something you didn’t know about.”

“How many hours a day did you put into it?”

“It was easy to put six or eight hours in a day. You had to do research at night. You’d quit at two in the morning and get up at four because you were so excited by what you’d found the night before.”

I can see how you would wind up doing that. “When you say ‘research,’ what did you find that an ordinary investor would not find?”

“You can plug into various Internet sources. Some of them are pretty legitimate. You may look at the Chicago Board Options Exchange and see which way the options are going. There are chat rooms. You have to filter out the chaff, but there are usually a couple gems that come through. Pretty soon, after a year or so, you get to recognize which names are more accurate and which ones are puff.”

Thin gruel. “How was it, financially?”

“It was good. However, I’m a good real estate guy. I make more money in real estate.”

“Less work?”

“Less risk. That’s the key.”

“I have ten accounts here, even though I’m dressed like a bum,” says Brian K. Tomlinson Sr.

I’m not sure if the man is speaking to Warren or to the lobby. What’s sure is that he has a cashier’s check in his hand and needs that require immediate attention.

Mr. Tomlinson has short black hair and a round brown face and is wearing a white T-shirt, jeans, brown moccasins, and…excuse me, his cell phone is ringing.

Tomlinson retrieves the phone from his pocket, listens to a greeting, says, “I’m fine. How are you doing?” Pause. “Right.” Pause. “Basically, you need to call back in an hour.”

The cell phone is slapped shut. Tomlinson moves toward Warren and begins a spiel about his cashier’s check.

Ring-ring.

Tomlinson answers and complains, “Some lady called me, but she was supposed to call my secretary.” Pause. “Call me later.”

There is a seamless reentry into cashier’s-check talk with Warren. Warren appears puzzled.

Ring-ring.

Tomlinson says, “I need to get to L.A. I’ll call you on the car phone.”

Warren, standing now, politely points to a red telephone hung on the wall. This is a direct line to a Schwab specialist who, he says, can answer every question.

Tomlinson engulfs the telephone and, very quickly, is into hard schmoose with a Schwab specialist lady. “Oh, you’re from Nigeria.” Pause. “Living in New York now?” Pause. “So, I have 1.8 million shares.” Pause. “If this goes to $1 in the next couple of weeks, I can sell this immediately, right?” Pause. “Do you come up with good deals every day?” Pause. “Wow. Can you e-mail me every day with different deals?”

Thirty minutes pass. Tomlinson ends his conversation, gets up, and, looking like a head of state making his farewells on the airport tarmac, engages in a series of good-byes with Warren.

I follow him outside and begin at the beginning. “How long have you been in the market?”

“Twenty years.”

“Did you see the market drop coming?”

“Definitely. Because everything is going electronic now. Companies that used to do things in the old way, it wasn’t working. That’s why the Internet crashed, because people weren’t ready for it. But now, all the Internet stuff is coming back.”

What…is…he…talking…about? “What exactly is coming back?”

“Well, you’re going to see a lot of things, from lottery to gaming to Visa and MasterCard. You’re going to see a lot of things like that. If you look at Starbucks or something like that, their stock has stayed strong because of revenue. People are looking for companies that have strong revenue and earnings.

“I believe you’ve got to know the trend and the future. It’s like Compaq. They’re never going out of business. Microsoft is good. They’re going to have ups and downs, but they’re always going to go back up because they plan for the technology of the future. That’s the key to the market.”

“Do you swing trade or day trade?” He’s going to say yes.

“Both.”

“You must be having a great summer.”

“That’s right. I gave you a tip just a minute ago.” Tomlinson produces a loud, utterly mirthless “Ha, ha, ha.”

I surmise he’s talking about one of the many obscure stocks he loudly referred to while performing on the phone. “Okay, how about a stock tip?”

“Right now — and it’s going to go through the roof, because I’m involved — is ECNT. [Three weeks after this conversation, pinksheets.com shows the best bid for ECNT as one penny per share.] It’s on the pink sheets. They’re going to [be listed on] Nasdaq in around 90 days. They control all the Mexicans and Europeans who use credit cards. You know how much it costs to send money through Western Union? This company has come out with a credit card with no Social Security number.”

“Which makes it easier for illegal immigrants to send money home?”

“And their mothers and fathers.” Tomlinson beams.

“I’ve read that 90 percent of the people who actively trade lose money. What makes you different?”

“Number one, I know what I’m doing. I took my time, I did my investigations. I’ve been dealing with the Internet 20 years. I own an international computer company. You have to do research. You have to know the trend, the future. You have to know the announcements. You need to know what the company is doing. You need to be actively involved in the company. Not what they say, but really do due diligence. Go into the company, check the employees, look at customer service, because that has a lot to do with the sales of the company.”

“Have you always made money?” He’s going to say yes.

“Yes, because I always buy penny stocks. I never buy stocks that are worth a lot of money. I always buy low, and I always check the company out before I buy. And then the stock goes through the roof. I bought this stock for 10 cents and it went to $22. And just this morning, I bought a stock for one penny and it’s going, today, to $2. And next week it’s going to $30. You’ve seen how many shares I bought?”

“Well, I overheard you say that you bought 900,000 shares.”

“I bought two million.” Tomlinson explodes with a great and genuine hustler’s laugh. Tears well up in his eyes as the hustler laugh cascades upward from his diaphragm, traveling the length of his throat, finally expelled through his mouth into the hot afternoon air. “That’s right. I always buy low. If you buy low and you know what’s going on with the company, it’s going to work.” Tomlinson’s expression is one of childlike wonderment at the prospect of gaining so much in return for risking so little.

I say, “If I bought two million shares of anything, I would be in front of a computer screen until I sold it. But you’re out on the street laughing and talking to me.”

“I know what I’m doing!” says Tomlinson at near-scream volume. “See, that’s what I’m saying, You gotta know what you’re doing. That’s the key.”

That’s the third key I’ve been given today. “What do you do besides the stock market?”

“I’m the CEO of Space Booth Enterprises and CEO of JC and Telephone. I own a telephone company. I have a church. I feed the poor. I feed the hungry all over the world. I’m a pastor.”

“Day trading as Christian calling?”

“Yeah. I mean, hey, it’s honest money and nobody knows.”

“What got you started in penny stocks?”

“My buddy taught me that. My buddy has been buying stocks for 40 years. He invested $15 million into my company. My stock went from $1 to $30 and it’s privately held. I own 60 Internet cafés, and I’m getting ready to roll out 1000 of them. That’s why I know this company [ECNT] is going somewhere. I’m like Starbucks or Kinko’s, but I’m private.”

Apostle Tomlinson tells me he’s 40 years old and single and has lived in San Diego for 20 years. He reaches into his wallet and hands me two business cards, says, “If you want to make some extra money, help me out with the Reader. I want to put some ads in the Reader, because, I tell you what, my banking card, every Mexican, every Vietnamese, every foreigner wants this card, because they can put up to $5000 on this card. If you help me put the ad in the Reader, I’ll put you free in the company.”

Thursday morning, July 25, and the Dow is 7911.12. I have a routine in place. I drive in just after rush hour, park at the Fifth Avenue ACE lot, grab a coffee-to-go from an adjacent deli, enter Schwab, say good morning to Warren, find the office Wall Street Journal, settle in, and wait.

I’d seen the man yesterday and talked to him briefly, just long enough to get his name, Bruce Thach. He’s back again, looking up stock quotes on the Schwab computer.

I decide to wait outside. Shortly, Thach steps out the door. He’s a slight man, somewhere near 60 years of age, 145 pounds, has a pale face with a dandy gray mustache set underneath a jaunty straw hat. But that’s merely pish-posh. What counts is the shirt. Thach is wearing a BLAZING red-and-yellow Hawaiian/Oaxacan/Peruvian/Ralph Steadman, altogether LOUD, eye-hurting loud, roast-the-pig festive, short-sleeved shirt.

I ask if he has a theory of the stock market. He says it occurred to him after a horrendous drunk. He woke up on the floor, and “just watch the ticker tape. You’ll see the stock going at the same price and the guy is just distributing stock all day long.”

Perhaps meaning will come in time. “When you say ‘distributing stock,’ what do you mean?”

“Well, the specialists, or whoever is running it, they are either stimulating or distributing.”

“How can you tell what they’re doing?”

“I check before 11 o’clock and see what they’ve done. They go on a lunch break between 11:00 to 12:00 and…”

Meaning is a long time coming. “When you say, ‘I check before 11 o’clock and see what they’ve done,’ who is ‘they’ and how do you know what they’ve done?”

“Oh, they’re specialists and they have the books. All the books, all the orders on the buy and sell above and below the market. All the stop losses.”

“And how do you know what ‘they’ve’ done?”

“Oh, you want to read the tape. They’ll bring the market up to whichever way they’re going to around 11, New York time. And then they’ll go on break. So the market tends to go the other way. And then when they come back at 12, they’ll reverse it again. So that will tell you if the specialists are accumulating or distributing.”

I see, the market is left unattended during lunchtime. “And you would know whether to buy or sell from that?”

“Well, it will give you an idea. And there are the weekly traders who come in on Monday. They’ll be out by Friday at the latest. They generally start coming on Wednesday. If you start watching the market, you’ll notice that it will reverse, usually on Wednesday. Sometimes it starts out in the morning and goes one way, occasionally.”

“What else?”

“Volume. Volume is your key.”

Another key. My key chain runneth over. “And a lot of volume means?”

“It takes volume to push a stock up, but it will drop of its own weight, because the market is an auction. You throw one share of General Motors up there, and if there isn’t any bid, that one share can, theoretically, bring the whole market down to zero. Because of no volume.”

It’s a problem. “What happens on days when the market drops 400 points?”

“Well, volume on selling. It is a little tough. You want to watch for the volume to dry up on the downside. Normally, that works, but not always. Sometimes, on low volume, the bottom will totally drop out.”

And then everybody goes to lunch. “What is your play today?”

“I would look for it to crash. My best thing is Investor’s Business Daily. I buy that every single day. They teach you in there. That’s one of the best magazines in the world.”

“Are you actively trading now?”

“Oh, oh, yeah, yeah.” Thach sounds hesitant.

“Are you selling short?”

“No. I did last week a little bit. I run in gold-mine stocks now. I’ve just been in gold-mine stocks.”

All I want to do is ask Thach to turn his shirt off. But instead, I chant, “How long have you been in the market?”

“About 40 years.”

“Long time.”

Thach grins. “Well, if I knew what I was doing, it would be different. It’s a guessing game. It’s gambling, there’s no doubt.”

“Are you ahead of the game?”

“Oh, totally, yeah. There have been years when I was wiped out. One time I was one of the best on Wall Street. The next year I was wiped out.” I hear a mirthless chuckle. “The old-timers, they don’t have any qualms with admitting that this is gambling.”

The best kind of gambling: no cops, available by modem or telephone from any place on the planet. “You must have a system.”

“Well, you can dissect the market in as many ways as there are people. I play by putting all my eggs in one basket and watching it close. The minute you diversify, it’s a formula for mediocrity. It’s hard enough when you’re looking for one big winner. If you dilute yourself into four or five other positions…”

If you had four or five different stocks, then when one stock crashed, you wouldn’t necessarily lose everything. But what’s the fun in that? “You said earlier that you were exclusively in gold-mine stocks. That’s because we’re in a bear market, right?”

“Yeah, yeah, yeah. I would look for a breaking of resistance levels in gold. I can say this much, once it breaks $800, there’s no telling where the high is.”

“But gold is only a little over $300 now, hasn’t been above $500 in 20 years or more, and has never hit $800.”

“Yeah, yeah.”

Okay. Moving on. “How old are you and where do you live?”

“I’m 58. Right now I’m staying downtown at the Golden West Hotel. I’ll be going back to Northern California very shortly.”

“You said the way to win in the market is to pick one stock and watch it.”

“Yeah, one stock, just one stock.”

“What happens if you’re margined to the tits and you guessed wrong? This must have happened at least once over 40 years?”

“Best thing in the world. Best thing in the world, because they’ll sell you out if the stock goes down low enough to where their equity is threatened. That takes the decision. I love to have a knife at my throat in the market. If I can find a way for somebody else to put a knife at my throat, wonderful. Generally the knife is smarter than you are and they’ll get you out. The worst thing that can happen is to try and meet a margin call. You’re better off if you don’t have money, then you can’t meet it.”

“I got in the stock market about four years ago.” The soft, unhurried voice belongs to Adele Honchor. Honchor is an elegant woman; think summertime East Hampton before the bad publicity. She has neck-length brown hair, a Roman face, thin lips, and an expression that suggests there’s more underneath.

I ask, “You were buying stocks?”

“Oh, yeah, I was buying a lot.”

“Tech stocks?”

“Oh, sure.” Honchor smiles as if remembering a long-ago summer. Which fits perfectly with her ash-colored cashmere sweatshirt and raffia hat.

We are sitting in the Schwab lobby next to an elderly couple. Warren is on the phone. All is easy. Honchor tells me she was raised in New York, attended Hunter College and then Columbia University. She moved to San Diego 30 years ago, works as a real estate broker, and lives in a downtown condominium.

She has come in this morning because “I have three accounts and I’m here to take half of it out and pay off a loan because I’m paying $70,000 a year in interest on loans. I said to myself, ‘That’s crazy.’ ”

“You must have a stock-market story.”

“Well, yeah. I’ve never studied the market. I depended on a friend, originally. We’d buy $1, $2 stocks and the stocks were going up to 20-something dollars. I’d buy $20,000 worth of these low-priced stocks. We were making so much money.” Honchor smiles. “It was such a euphoria.”

Must have been a fantastic time. “Must have been a fantastic time.”

“I felt so smart and rich.”

I can almost smell money cooking. “How many different stocks did you trade?”

“Oh, a lot. I kept track of them in two notebooks. Every day, I would write my little numbers in. It was an obsession.”

I can see her at work. “The feeling you have is, ‘This is the way life should be.’ ”

“Yes. Exactly. Yes!” Honchor laughs. “It was like, ‘What’s the matter with you, why aren’t you taking risks?’ I had one woman — she’s a friend of mine, she’s almost 80 — beg me to take her money so she could make money the way I was making it. Thank goodness I didn’t.”

“You were playing the market at high tide.” The Nasdaq topped out at 5048.62 on March 10, 2000.

“Yeah, I day-traded, had loads of fun making money with an engineer friend. He was disciplined. He’d say, ‘If it goes up two points, sell it.’ But of course you get emotional; you don’t want to sell, and you hold on to it. It’s everybody’s story, I suppose. You fall in love with the stock.”

“When did you realize that the party was over?”

“Last year, but I was still in on it. We started buying blue chips, getting out of all that” — Honchor sounds a soul-warming chuckle — “trashy stock that was worth 67 cents a share. I’m thinking, ‘My God, I’ve just lost $100,000.’ About three months ago, I said, ‘I want out.’ ”

“Exquisite timing.” Three months ago the Dow closed at 10,035.06.

“I finally convinced my husband, who is a financial planner. I said, ‘Just sell it. I don’t care, sell it all.’ And he did and it hurt. You know, it hurts to lose money, but I beat a terrible depression.

“I hated the feeling that my life was dependent on those numbers. I felt it wasn’t worth it. I’d rather be peaceful. Of course, I loved the excitement and euphoria, but then there’s the crash. I didn’t want to live that way anymore.”

“When you signed off, were you ahead, behind, or even?”

Honchor closes her eyes. “I am certain I lost quite a bit of money. I don’t want to look at it, but I know I did.”

“What was your high point? It must have been seven figures.”

“No, it wasn’t that high. Maybe I made a couple hundred thousand. I didn’t make like some of the stories you hear. You see, stocks go up and down. A stock may go up and then it goes all the way down, so you bought some more. Even now, I think, ‘Whoa, these great companies — they’ve got to go back up.’ I’m so tempted to get in on it.”

“Do you think the market will be a temptation a year from now?”

“Yes.”

“Or when the Dow gets down to 5800?”

“Yes,” Honchor laughs. “I don’t know if it will get down that low.”

“Sixty-eight hundred?”

“I don’t know. I think I’d tell my children if it gets that low, because they need to make money. But I think people who are in their business, whether it’s a little store or whatever, they should stay in their business. You need to have so much knowledge to be in the market, and even with all the knowledge you can’t…”

“…predict the market.”

“I don’t think anybody can predict anything.”

Time to go. “How would you describe the last three years of your life?”

“It’s made me humble and amused. I understand my own weaknesses for greed. It’s put a perspective on my life.”

I’ll close with a bit more of the conversation I had with the short seller we met earlier. We’ll pick up at the point I asked for his assessment of the market.

“I think it’s a tough game anymore. I think the correct hedge is being in cash and staying out of the melee.

“There is one thing that is true about this market: a lot of people are long and can’t get out. You can look at individual cases and there might be something to buy, but the dynamic of the market is inextricably down. And, in fact, the market is so overvalued. We’re basically in a crash.”

“What is fair value of the Dow?”

The short seller laughs. “Asset value and accounts receivable, that’s the book value of a company. Everything else is goodwill. There are different conventional points people use to measure. [He’s referring to the P/E, or price-earnings ratio. As mentioned earlier, the P/E is the price of a stock divided by its earnings per share.] I would say, in general, the normal value for the market, when it’s high, is about 12 times earnings. Then the normal value for the market, when it’s okay, is about 8 times earnings. We’re still looking at 20 to 30 times earnings. [As I write this, the Dow has a P/E of 23.89.]

“People don’t have a lot of risk tolerance at this point. They had unlimited risk tolerance a mere three years ago. Now, I would suppose, investors would want to be under the conventional P/E earnings number. So I think we would bottom out around 5 times earnings.”

“That would make the…”

“Well, it would make the Nasdaq in the 600s or 700s, make the Dow somewhere in the few thousands, which is where it should be.”

Soft, my heart. “The Dow should be 2500, 3000?”

“Yeah, we’re doing a reset. We’re working our way back to 1982. We haven’t even seen the beginning. This is brutal. This is the real deal. We’ve had such huge misbehavior, the equity markets themselves have been abused. People have used them ad nauseam. Now the idea is to hang CEOs or something.” I hear a full-throated laugh. “Nobody wants to look within. Unbridled greed.

“The macro assumption about telecommunications was so palpably idiotic. CMGI is down to 40 cents, it was $400 [CMGI had one 3-for-2 stock split in March 1995 and five 2-for-1 stock splits since then]. Obviously a lot of telecom companies never had any value. They were air. When people started talking about black cable having value that exceeds white cable.…”

“What is black cable?”

“Telecommunications optical cable that was being strung but hadn’t been fired up. So it didn’t have any information in it, so, therefore, the value of it was better than white cable, because white cable already had information transmitting through it and you could calculate some kind of general value. Of course, it was a value based on the convention of the time, where 30 times earnings is normal and 100 times earnings is where we should be because we’re in a new economic era.

“Everything was so crazy. People were talking such incredible nonsense. Paradigm shifts and the New Economy and the new way of doing accounting.”

“So, the crash is on?”

“You can still have manic rises, but in the end, the market will mark itself to value. And value is, unfortunately, a lot lower.”

“Well, yeah, 2500 points on the Dow is a lot lower.”

“Well, maybe it will only be 4000. I don’t know. It’s certainly going to be a lot lower. Not a problem.”

Here's something you might be interested in.

San Diego brokers on Wall Street

"Pick one stock and watch it”

San Diego brokers on Wall Street

"Pick one stock and watch it”

Monday, July 22, 2002, 9:38 a.m. The Dow Jones Industrial Average is down 284.52 points to 7734.74. I push on a glass door and enter into a small lobby. This is the downtown Charles Schwab office, located on the corner of Fifth Avenue and A Street. Sitting behind a circular counter is Warren, the receptionist. He looks to be in his mid-30s, with dark hair and a ruddy, clean-shaven face.

Set next to a bank of windows facing A Street are five chairs and an end table. Against the opposite wall, inside semi-private cubicles, are two computers. A man stands in front of each computer, or, more precisely, crouches in front of each computer. Two keyboards click-click-click as the pair retrieves stock quotes. Sometimes in unison, sometimes alternating, the men exhale an “Oh” or an “Ah,” followed by another gush of keyboard clicks.

“How long have you been in the market?”

“About ten years.” Speaking is Jeff Spreter, 23, five foot ten, 175 pounds, with recently trimmed brown hair, dressed in a white cotton T-shirt and jeans.

“Did you see this coming?” “This” being the recent 2500-point drop in the Dow.

“I kind of saw it falling apart, but not to this extent.”

Spreter lives in Coronado and graduated from San Diego State this year. “How much money have you lost?” Might as well get right to it.

“Probably 15 [thousand dollars].” Spreter does not flinch.

Mere collateral damage. “Do you ever think about what you might have done with that money?”

“Not really. It was paper money — it really didn’t exist.”

Spreter tells me he’s studying for law school. I flee from the topic. “Have you changed your plans about vacations or purchases?”

“Not really.”

“Was there one particular stock that trashed you more than others?”

Spreter laughs. “Oh, yeah, Enron and Global Crossing.” Now we both laugh. “I bought them at $8…”

Enron is selling for 9 cents today, down from $90.75. Global Crossing is bid 5 cents, down from $64.25. “Have you ever taken classes about the stock market?”

“Yeah, I’m a finance major. I just graduated.”

Okay, here we are: free, qualified advice. “What’s your take? How long is this slide going to last?”

“There’s psychological support, maybe, at 7500, 6800.”

I do not feel comforted. “How much money do you have in the market today?”

“About $20,000.”

“So, being young, you’re not worried?”

“I make $400 a year on GE dividends, so I’m not too worried.”

I hate young people. “Where would the market have to go before you started to sweat?”

“Oh, 6500, 6800. That would be ugly.”

It’s 9:58 a.m. and the Dow is down 232 points.

A short — five-foot, six-inch, say — 35-year-old man with curly red hair, horn-rimmed glasses, and an expression of eternal displeasure, is huffing and puffing in front of a computer monitor. He makes a loud grunt, throws up his hands, and stomps out the front door.

I catch up, introduce myself, and ask, “How long have you been in the market?”

The man answers using a stage whisper, so no one can overhear, yet everyone will understand he is saying something important. “Twelve years.”

“Did you see this coming?”

“Yeah.”

“Have you been selling short and making money?”

The short guy nods his head, looks over his shoulder to see if anyone is coming out of the Schwab office. I figure the guy for a short seller. Typically, a short seller borrows, say, 100 shares of Microsoft from his broker, betting that Microsoft will drop, let’s say, $10. He then sells those shares on the open market. Let’s say Microsoft cooperates and drops $10. Then the short seller buys 100 shares on the open market and uses them to replace the stock he borrowed from the broker. He pockets the difference between the price at which he sold and the price at which he bought, minus commissions, interest, and every other fee the broker can dream up.

Short selling is one of those legal but culturally disapproved of activities, like selling tobacco to retarded, pregnant teenage girls. You’ll never see a newspaper headline scream, “Dow Down 500 Points, Great Day for Short Sellers.” When the market is going up, you’ll never see interviews with short sellers who have lost their homes and life savings. There is a cultural bias, one pushed hard by the stock market–industrial complex, to root for the home team, home team being defined as a stock market going up.

But if you believe, and a lot of people do, that the stock market is casino gambling all the way down to the fat house edge, then being a short seller is just another way to play the game. Here’s the weird part: even knowing this, short sellers, in the backs of their minds, believe they’re doing something wrong. And so, short sellers, like gamblers everywhere, speak in whispers and look over their shoulders. In fact, short sellers, as a rule, look like this fellow, they look like they’re doing something illegal.

I say softly, so as not to ruffle delicate psyche feathers, “You’ve been selling short. You must be having a good time?”

“I’m having a good time.”

I detect not a single nuance of pleasure in his voice. “When did you recognize that the fall was coming?”

“About two years ago.”

“You’ve been selling short this whole time?”

“Yes.”

Again, not a flicker of satisfaction in his voice. “Can you give me a hazy figure of your winnings? Have you made $1000 or $100,000?”

“I don’t think that’s relevant.”

“What is more relevant?” The short, short seller’s face freezes in an expression of outrage. No gambler will tell the truth about his winnings or losings. Indeed, it is a terrible breach of etiquette to solicit personal information. I hurry forward. “I take it you don’t worry about the stock market?”

“Not at all.”

“Do you worry it might go up?”

“No, I’m in cash now.”

I should mention that short sellers tend to be smart, which doesn’t mean they can predict the future better than anyone else, only that they can talk about the future better than most. We’ll come back to the short seller after a while.

The lobby is empty save for Warren and me. I put down Schwab’s copy of the Wall Street Journal and inquire, “Are people calling in sounding genuinely distressed?”

“A lot of people are very concerned about where the market is heading. Especially compared to where they were one year ago, six months ago. Definitely.”

“Have you heard panic?”

“People are coming in and saying, ‘I need to sell everything right now.’ ”

That’s a long way from panic. “I was visiting Washington, D.C., in ’87 when the Dow dropped 508 points in one day, except then, 508 points was 22 percent of the Dow. That morning, I went to the Schwab office on I Street. You couldn’t telephone. Schwab had so many phone calls, their switchboard imploded. When I arrived, there must have been 50 people milling around on the sidewalk trying to get in the front door. Women were crying. People who had made it inside the lobby couldn’t see a broker. It was…”

“No, it’s not that bad.” Warren smiles as if I’ve been explaining how covered wagons are built. “The closest I’ve seen to that is a 10-, 15-minute phone wait to get through to a broker.”

“How long have you been in the market?”

“About four or five years,” says Steve Schoob, a truck driver from Cottonwood, Arizona. Schoob’s in town visiting his parents and stopped by to check his stocks. I ask the usual. “Did you see this coming?”

“The guy who sells to me did.” Schoob is wearing a navy blue T-shirt, jeans, and a huge silver necklace with what, I swear, looks to be a trout fish lure minus the hook as a pendant. “We’re in electric and water stocks and all that stuff now. We didn’t get hurt bad, but we’ve lost some.” Schoob thinks for a moment. “I’ve got a friend who’s $1,500,000 down.”

Hey, it’s only paper money. “Have you reconsidered any plans or purchases?”

“Nope, not at all.”

I believe him. “How did you first come into the market?”

“Bank of America. Through mutual funds. Then I started getting into it more.”

Captain Crunch breakfast cereal, Coca-Cola, marijuana, heroin, and then the stock market. It’s a straight line to hell in a handbasket. “Is this the beginning, middle, or end of the bear market?”

“I hope this is the end, but who knows?” Schoob makes a cowboy shrug. “It might go a little bit lower.”

“Do you ever worry about the market?”

“Heck, no.”

“Have you spent any time studying the market, researching it?”

“Not really. I have a friend who does that for me. I just give him money and he takes care of it. This guy really studies the market and we’ve made money.”

There is, at the end of the day, no argument to that. “What do you think caused the Dow to crash?”

“I think 9/11 had something to do with it. And all the executives taking off the top.”

I note a trace of cowboy anger. “What should be done with them?”

“I hope they hang them. I think they should be hung.”

10:28 a.m. and the Dow is down 168 points.

“How long have you been in the market?”

Joe Nalven says, “Since the early ’70s.”

Mr. Joe Nalven is middle-aged and could pass as a twin of Senator Joe Lieberman, if, that is, Senator Joe was born with blond hair and raised on the West Coast. Citizen Joe lives in Poway. I ask, “What got you started in the market?”

“My in-laws thought it would be a good place to put extra money from time to time.”

“What was your first stock?”

“Warner [one of the sires of AOL Time Warner] and General Motors.”

“So you’ve seen this before?”

“Oh, yeah, the cycles of depression and elations are quite familiar.”

“Where are we along the axis of despair and joy?” Pretty damn poetic question.

“I’d like to believe, and I think all of us are hedging our bets, but I’d like to believe we’re near a low.” I note Joe speaks like Joe Lieberman. “Looking at the overall robustness of the economy, it doesn’t make sense to be this low. But, then again, listening to the news, the highs weren’t probably where we ought to have been either.

“The big question is, if you pull out and take a tax hit on what you’ve made, even if it was not as much as you would like to have made, then what do you do with that money? Do you put it in your mattress? The market forces you to balance risk in a number of different ways. And that’s suddenly one of the problems we have now, because it’s hard to gauge the kind of risk we’re in.”

Nalven poses a question many of us need not answer since one is not required to pay taxes on losses, only on gains. I say, “The Dow P/E is over 20, indicating to people who believe P/Es are important that the stock market is still overvalued.” P/E, or price-earnings ratio, is the price of a stock divided by its earnings per share. For instance, a $60 stock price divided by $3 of earnings per share gives you a P/E ratio, or P/E, of 20.

Nalven isn’t buying. “But you have other stocks, like Microsoft, which has always had a P/E in the 30s, 40s, and 50s, and it’s held its ability to grow. Still, the market may force us to go more towards value.

“Where is the real value in putting your money in the stock market?” Now he really sounds like Joe Lieberman. “Say you hold Johnson & Johnson. Well, that’s a good stock. And I emphasize good stock. And now you read about how they are having accounting problems. If bedrock firms start having problems, how do you make sense of that? What’s real?”

Theft and fraud. “What do you think ought to be done with Enron and WorldCom executives?”

“I think jail is a very good place. We need to ramp up the integrity of the marketplace. If self-policing were okay, we wouldn’t need a police force.” Nalven stops for a breath. “I’m an attorney. I represent people. I have a skeptical view on human nature. I’m an anthropologist as well. So on two counts I’m very skeptical about human nature. What we see now is more punishment as a way to make the marketplace more secure, but, then again, is that really a guarantee? We trade one illusion for another.”

Yes, well, maybe, perhaps. “Let me have your stock tip of the day.”

“I often listen to Bill Holland on the radio, and he’s saying the stock market is going to go with the rest of the country. If the country is going to go in the tubes, then what’s the point of having stocks anyway?”

Sitting military straight, in the far chair, is a nervous, pensive-looking man. I assume he’s waiting for an appointment. The man has a smooth oval face and pursed lips and is bald save for a streak of cropped gray hair above his ears. I say hello. We chat a bit. I learn he’s here to put money into the market. His name is Craig Christiansen. He’s been working as a transportation assistant on North Island and lives in Normal Heights.

Christiansen says, “I don’t know anything about investing or nothing. I’m kind of the, what do you call it, the green…things are green, or whatever they call it when you’re new at something.”

“Greenhorn?”

“Yeah.” We laugh. Christiansen says, tentatively, “I have to withdraw this money by August 23. I guess I retired at the wrong time. What they tell me to do is open an IRA, which is the only thing my 401(k) can do. It’s going to be a rollover-type IRA. My dad’s been saying, ‘We’ll just keep it in a money market right now, and when this market gets better we’ll see about stocks and bonds and all that.’ ”

I ask, “Has your 401(k) lost money?”

“Lost $1000 in a month.” Christiansen is suddenly decisive. “My ending balance in May was $42,000, and my ending balance in June was $41,000.”

“That’s not bad, to be only $1000 down.” In fact, that’s a better record than anyone I know.

“No, it’s not. But, see, that’s government bonds and stock. But now I have to take it out by August 23, because the system is going over to a new computer and I don’t want to wait, and who knows what might happen with a new computer system? So I’m trying to get it done now.”

Either he knows a great deal about computers or he knows nothing about computers. “Well, you’re maintaining your capital. A lot of people have lost a lot of money.”

“My dad said he’s lost some, but not a lot. He keeps telling me about diversification, because you have to put the money in different spots.”

“Have you studied the market?”

“No, I haven’t. In fact, I’m one of these who would rather have someone else do it for me. I can’t balance my checkbook, let alone anything else.”

I can feel sharks circling. “Do you worry about the stock market and what might happen?”

“Well, right now, I’m kind of worried, but I’m not in it yet. I didn’t worry about it when I was working. But now that I have all this money, I need to find a place, someplace where it will get me more bang for my buck.”

Christiansen leans toward me. “This has to last. I’m a young retiree with a disability. I need this money for when I get older, because I’m not a normal retiree who retires at age 62 or whatever. I am retiring at 43. My retirement will be a lot longer. This 40-some thousand has to last me, because I have nothing else except for the annuity I get for my disability.”

One bad break would cost $40,000. Easy. “What’s wrong?”

“Diabetic neuropathy. I have no feeling from my knees down. Losing it in my hands as well. Now I’m stuck on the bus. I can’t drive anymore.”

And again. “How long have you been in the stock market?”

“Over 30 years. I belonged to an investment club.”

I’m talking to Helen “My mother gave me a short name in case I had bad handwriting” Callahan. Mrs. Callahan is a happy-looking woman in her 70s. I make her for five foot six. She has curly auburn hair, an easy smile, and wonderful laugh lines around her eyes. I ask, “Are you in a fund or individual stocks?”

“Individual stocks.”

“How is that going?”

“I don’t know. I don’t care. I don’t look. We don’t need the money now. If you don’t need the money, your losses are only on paper. I spoke to my daughter in Berkeley last night. She said, ‘Mom, I’ve lost $10,000.’ I said, ‘Nancy, that’s only on paper. Wait, it will go up.’ And it will go up.”

Nobody has actually lost money. I ask, “Are you continuing to buy stocks?”

“No. He [Callahan nods to her husband in the next chair] is going to be 80, I’m 79, and there’s not enough money to buy.”

Helen was trained as a nurse. “I graduated from the Columbia Presbyterian School of Nursing in New York, but I never worked. My husband was a single-engine carrier pilot in the Navy. And then he had his own tax and bookkeeping business. We’ve lived in Coronado for 40 years.”

Sounds quite pleasant. “When you were in the investment club, did you study the market?”

“We never bought anything if it didn’t go through our study group. We never took more than 20 people in the club, all women in the club. We used to have meetings once a year. We disbanded two years ago.”

“How come?”

“Because we were old, we were tired, and the market was high. We’d been going on for 30 years. We got down to 15 members — people had died, moved away. We decided to disband. That was 2 years ago. We had a big sell-off and then went to lunch and everybody got her check and we all made money.”

“Nice going.” Exactly two years ago the Dow closed at 10,733.

“How are you doing in the market?”

“I’m frustrated,” says Norbert Seufert, a tall, red-faced, blond-haired man with linebacker shoulders and a fighter’s chest. “I’m still hopeful that in time, things will turn around. There have been nine recessions since WWII and nine recoveries, so I’m trying to be mindful of that. I have to imagine that there is only so much further it can go down.”

“Have you seen a bear market before?”

“Indirectly. My parents have been in the market for an awfully long time. I guess the ’70s was, essentially, a bear market, going nowhere for ten years, but not like this.”

“Have you gotten hurt yet?”

“I’m deeply in the red, yes. My parents are heavily invested in blue chips. I’m an only child, so I know that one day those stocks will make their way over to me through inheritance. I’ve recognized that tech is, probably, our future, so I’ve been heavily invested in tech. I’ve obviously taken quite a beating. I owned bellwether techs and that hasn’t protected me.”

Today, Intel will close at $18.26, down from an August 31, 2000, close of $74.875. Oracle will close at $9.23, down from a March 27, 2000, close of $44.218. “How low can Nasdaq go?”

“Well, I’m 40 now — maybe 25 years until things turn around.” Seufert laughs. “A lot sooner than that. I’m hoping within the next two or three years. I can’t imagine who’s selling at these levels.”

“You said you are in the red. Are you on margin?”

“I am on margin. I thought Intel, with a dip, would be a brilliant buy. I’ve seen it dip another 50 percent since that point, so…”

I wince. “What caused the market to drop?”

“Obviously the accounting scandals. There’s a hysteria that feeds on itself. I am someone who fancies himself as a long-term investor, and even I have had thoughts of ‘Well, let’s sell and salvage something.’ But now I am of a mind to say, ‘I think, maybe, this represents a better buying opportunity than has ever presented itself in the past 15 years.’ ”

I do not reach for my wallet. “How much time per day do you spend studying the market?”

“Anywhere from 15 minutes checking Yahoo Finance, to two hours reading publications like Business Week and Smart Money, trying to get a handle on which moves I ought to be making.”

“Do you think anybody knows where the market will go?”

“That’s very interesting. We’ve heard stories about analysts who were promoting a stock heavily at 40 and who are now telling you to sell it at $3. You have to wonder if anybody did know. If someone knew, then there’d be a formula for success and then everybody would be on board. Then it would no longer be a formula for success.

“Having been an investor now for close to 20 years, you want to know what your money is doing. You can’t rely on other people, necessarily, to manage your money. A lot of very smart mutual fund managers have taken a critical beating. So who’s to say? And market psychology is not something anybody can get their hands on. It’s mass psychology. You have to recognize that nobody truly knows. You make as educated a guess as you can.”

This is called investing. “Did you see the slide coming?”

“Obviously not. There was a point when it started to dip. It dipped 10 and then 15 percent. But unless it hits a 28 percent dip, I’d take a tax hit by selling and buying back into it. So, even when the dip started, I felt like it was just a correction.

“I can tell you, from personal experience, that business publications were not telling everybody, ‘This is the start of something very big.’ They were saying, ‘Hey, here’s a little dip, it’s a buying opportunity.’

“Well, that dip was Nasdaq at 4000 and the next dip was Nasdaq at 3000. Now we’re seeing Nasdaq at 1200 and change. Nobody’s been predicting this dip in all the publications I’ve been reading, and I’m pretty well read in the subject.”

The media as responsible adult. “Has the crash caused you to defer any purchases?”

“Absolutely. Not buying a new car. Not remodeling our house. Making travel a little more modest than I might have otherwise.”

“What do you do?”

“I’m in advertising.”

There is a period of impolite quiet. Finally, I ask, “Do you have a stock tip?”

“I’ve been buying Elan Pharmaceuticals, because I’ve been reading about them for four years and everybody talks about what a terrific company it is. They’re in the space of making generic drugs, and I know, with the graying of the population, drugs are gonna make out. I have to imagine that that company has been hurt more than it deserves.”

Elan will close today at $1.84, down from the August 13, 2001, price of $57. “Do you have a favorite stock horror story?”

“I’d have to say buying Intel on margin at $49. I bought a couch that I felt was too expensive. I said to myself, ‘Okay, let me take a big margin position in Intel, and when it goes back up two points, I’ll sell and make $2000 profit. That way I can buy the couch for what I think it was really worth.’ Now I’m sitting on Intel at $19 and, every night, sitting on a $35,000 couch.”

“I’ve been in the market since 1953.”

Speaking is Richard Wright. It’s Wednesday morning, July 24, and I’m back in the window chair at Schwab’s. I ask, “Did you see this coming?”

Wright, who looks like a tall Ernest Hemingway without the egomania, answers, “Yes, I was pessimistic a year ago.”

“How about two years ago? What did you think about the market then?”

“Techs started crumbling two years ago, but the Dow was still going strong, as if it were business as usual. I didn’t see any downward forecast from the media. They didn’t talk about earnings, didn’t talk about the solidness of stocks.”

Media as responsible adult, part II. “When you saw the Nasdaq go, did you take defensive measures?”

“I did, but not enough. I had options that went south on me. I should have cashed them in at the time. I had a large block of options in Unisys. It fell apart about a week before they were due.”

“Have you had to cut back on any plans, vacations, purchases?”

“No, because the money I used was discretionary money. I never got into my personal assets.”

“So you were playing with house money?”

“Exactly.” Wright smiles like a man who just got something for nothing.

“Which stocks are you in now?”

“Lucent. I just picked up some Lucent and I’m looking at a health-care stock. I like that one and GE.”

(As I write this, GE is selling for $32.05, up from $23.02, its price at the time of this conversation.) “You said you started in the market in 1953, almost 50 years ago. What was your first stock?”

“I was 20-some years old. My barber told me about penny stocks from Canada. I got into the stock market then. I had a Merrill Lynch, Pierce, Fenner and Bean account. Remember those days?”

I don’t. I nod yes. “How did you do?”

“It went up a couple of pennies. I thought I was in heaven.”

Wright tells me that three or four years ago he was a swing trader. Says he took classes in swing trading and day trading up in Orange County. I ask, “What did you learn?”

“The instructor’s message, frankly, was to stay out of techs. He said stocks undulate; read the undulations and play them. He also told us we were competing with the big boys who were doing the very same thing.”

Nothing to it. “I’ve read stories that say 90 percent of day traders lost money.”

“Oh, I can believe that.”

“What separated you from them?”

“You lose money for a while and then you learn not to make those same mistakes again. Then you start making money and that’s where I was. When I hung up my spurs, I was making money, but I paid the price. The price is, you let your emotions take over and make a purchase and then you shoot your toe off.” Wright laughs. “Now you only have nine toes left.

“Pretty soon, you say, ‘All right, I’m done doing that. I’m just going to use the old formula. I’m going to use the mechanics of it. I’m going to read the charts. I’m going to read the news. I’m going to get up at four in the morning and do all the research.’ Even then, you get the rug pulled out from underneath you by something you didn’t know about.”

“How many hours a day did you put into it?”

“It was easy to put six or eight hours in a day. You had to do research at night. You’d quit at two in the morning and get up at four because you were so excited by what you’d found the night before.”

I can see how you would wind up doing that. “When you say ‘research,’ what did you find that an ordinary investor would not find?”

“You can plug into various Internet sources. Some of them are pretty legitimate. You may look at the Chicago Board Options Exchange and see which way the options are going. There are chat rooms. You have to filter out the chaff, but there are usually a couple gems that come through. Pretty soon, after a year or so, you get to recognize which names are more accurate and which ones are puff.”

Thin gruel. “How was it, financially?”

“It was good. However, I’m a good real estate guy. I make more money in real estate.”

“Less work?”

“Less risk. That’s the key.”

“I have ten accounts here, even though I’m dressed like a bum,” says Brian K. Tomlinson Sr.

I’m not sure if the man is speaking to Warren or to the lobby. What’s sure is that he has a cashier’s check in his hand and needs that require immediate attention.

Mr. Tomlinson has short black hair and a round brown face and is wearing a white T-shirt, jeans, brown moccasins, and…excuse me, his cell phone is ringing.

Tomlinson retrieves the phone from his pocket, listens to a greeting, says, “I’m fine. How are you doing?” Pause. “Right.” Pause. “Basically, you need to call back in an hour.”

The cell phone is slapped shut. Tomlinson moves toward Warren and begins a spiel about his cashier’s check.

Ring-ring.

Tomlinson answers and complains, “Some lady called me, but she was supposed to call my secretary.” Pause. “Call me later.”

There is a seamless reentry into cashier’s-check talk with Warren. Warren appears puzzled.

Ring-ring.

Tomlinson says, “I need to get to L.A. I’ll call you on the car phone.”

Warren, standing now, politely points to a red telephone hung on the wall. This is a direct line to a Schwab specialist who, he says, can answer every question.

Tomlinson engulfs the telephone and, very quickly, is into hard schmoose with a Schwab specialist lady. “Oh, you’re from Nigeria.” Pause. “Living in New York now?” Pause. “So, I have 1.8 million shares.” Pause. “If this goes to $1 in the next couple of weeks, I can sell this immediately, right?” Pause. “Do you come up with good deals every day?” Pause. “Wow. Can you e-mail me every day with different deals?”

Thirty minutes pass. Tomlinson ends his conversation, gets up, and, looking like a head of state making his farewells on the airport tarmac, engages in a series of good-byes with Warren.

I follow him outside and begin at the beginning. “How long have you been in the market?”

“Twenty years.”

“Did you see the market drop coming?”