{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Michael Fanghella and the decadence that PinnFund led to

I have more money than I could possibly spend in our lifetime

Perched atop a flagpole at One Times Square sat the New Year’s Eve ball, ready for its traditional drop. For this drop, marking the end of the millennium, the famous orb had been sold to Waterford, legendary Irish glassmakers, and re-spangled. It was now the Waterford crystal ball. Such advertising was emblematic of the 1990s: from Tiger Woods’s hat to movie titles on NASA rockets, panoptic exposure seemed valuable at any price. Awaiting the Waterford’s fall, bodies had backfilled midtown Manhattan all day until, at 11:59, nearly one million gleeful voices began counting down the ball’s light-pulsing descent, synchronized to the (now-forgotten) “Anthem for the Millennium.” In that moment, most revelers believed the Y2K scare was bogus and the new year would arrive intact, granting not so much a new age but, what was truly hoped, continuity with the one passing, its incontinent dot-com profits a testament to the prodigal investor. Everywhere people were betting that the American good life had another good act to go.

Earlier that day, ten blocks east of Times Square, San Diego mortgage lender Michael Joseph Fanghella was readying to part with a small portion of his 1990s easy money. In his executive suite at the Palace Hotel, Fanghella (his pronunciation stresses the second syllable — Fang-hell-a) was phoning an escort service, Nici’s Girls, for a New Year’s Eve date. Nici’s “Millionaire Club,” of which he was a member, promises girls “for an intimate evening, a romantic weekend, or maybe even a lifetime. The introduction rate for these spectacular ladies begins at $10,000.” Fanghella used Nici’s often and liked, in particular, their “high-profile porn stars.” As one of San Diego’s nouveau riche, the 48-year-old, with his wife Patrice and the company’s chief executive officer, Keith Grubba, owned a subprime mortgage lending business in Carlsbad called PinnFund, USA, purportedly processing and profiting from $4 billion in home loans each year. Such bounty allowed Fanghella his pick of Nici’s petals as well as other women he met at his multi-city “party-centrals,” the Spearmint Rhino Adult Cabaret in Las Vegas or San Diego’s Deja Vu strip club, where he was known to spend $10,000 per week. He lavished on escorts, prostitutes, porn stars, and their coterie whatever they desired, from jewelry to Las Vegas junkets, from fine wines to limo rides. The massive amounts of monies PinnFund was moving to fund home mortgages would cover it all.

An hour later, ascending in the Palace elevator, came Kelly Jaye Cook. A former Atlanta Hawks cheerleader and one of Playboy’s “Girls of the NBA,” Cook had made adult movies for Sin City and Vivid Video, where, as Kelly Jaye, she starred in Blonde Angel and Bad Girls 4. After a dozen films, she quit hard-core for more lucrative pursuits: magazine spreads and a Playboy strippers pictorial; modeling in bathing suit and high heels at car shows; appearances on Saturdays at adult video stores, earning $2300 by signing “slicks,” posters of her movie boxes (“She looked good on a box,” said one Vivid star); dancing (porn wages pale next to stripper’s tips); and being an escort, the professional date.

Cook herself was not unattached. For one, her divorce from Ken Cook was not yet settled. For another, she was, during the fall of 1999, living in an apartment on West 90th Street, which she and her boyfriend, Charles Spagnola, rented. Cook had been living in Laguna Niguel, a bedroom community above Laguna Beach, with Spagnola, a Garden Grove criminal defense lawyer. Then, after 18 months together, they had separated, apparently due to a fight and because Cook wanted to work in New York. Cook let Spagnola stay in her house on Westfield Drive in Laguna Niguel.

For his part, Fanghella had more than a few worries.

According to his wife Patrice, his personal life had been on a “downhill spiral” for several years — and it was getting worse. After 16 years of marriage, living since 1996 in Rancho Santa Fe, Patrice described the violence that led to their separation in late September 1999. She stated that her husband “has verbally, physically, and sexually assaulted me,” at one point threatening to kill himself and her in front of their daughter. “He has,” she continued, “consistently shoved me, pushed me, slapped me, [and] spit on me.” (She also admits to her “downfall” — being in love with him and thinking he’d change.) In July 1998, an intoxicated Fanghella wrecked his Jaguar and spent a night in jail. In 1999, arrested again for drunk driving, he landed in jail for four nights. His license revoked, from then on he traveled by limo. In September, Patrice initiated an “intervention” at PinnFund’s offices to force him into treatment for his drug and alcohol addictions; his response (though he finally agreed) was to trash his office. During his subsequent 24 days in rehab at Scripps McDonald Center in La Jolla, his conduct was so “volatile and belligerent” that he was “kicked out” of the program. His doctor at Scripps warned Patrice that her husband “posed a very real physical threat and danger to [his] family” and she should “obtain police protection.” Finally, Fanghella’s favorite pastime — the pursuit of sexual stimulation — had mushroomed to a third addiction. Patrice separated from him after this admission of his promiscuity — that, while in New York, he was living with Lisa Spagnuola (no relation to Charles Spagnola); that he was seeing a woman named Denise Marohl; and that he was “cavorting” with “four regular prostitutes.”

Icing on the dysfunctional cake, PinnFund had grown so big, so fast that he was continually anxious about its finances and jettisoned the anxiety by indulging in female toys whenever he wanted.

Unaware of her date’s disorders, Kelly Cook entered Fanghella’s hotel room that New Year’s Eve afternoon: a passerby might have heard a Roy Orbison–like grrrrrrrowl. What did Fanghella see? A perfectly sculpted body. Waist belted tight. Hips like boards, that is, not much of them. Large, hard-jellied implants, anti-gravity floats. Wild mane, cornstalk yellow blond. A glistening, just-wet look. She was elevated: four-inch heels were de rigueur. Perhaps she wore one of her favorite alluring outfits: python-print leather dress, audibly tight; python-print silk blouse, fingertip soft. Sexual enclosure, needing liberation. Would you mind walking in again, Miss Cook?

What did she see? An imperious man, Fanghella. Probing brown eyes; luxuriant brown hair. Gap-toothed, a tad pouty-mouthed. Natty, handsome, but more casual than rugged, one leg crossed over the other, torqued in anticipation like a man on the stand bearing testimony. An air of Napoleonic preoccupation, a trace of mistrust. So you’re a mortgage lender, Mister Fanghella?

They spent an hour together, Fanghella said, “talking, unusually interested in each other right away — admittedly quick but nevertheless true.” (Fanghella’s words are taken, as are Cook’s, from transcribed and videotaped depositions. Almost everything about their relationship is in dispute except a mutual lust for the high life.) Fanghella called Cook “thoughtful, sensitive.” While he had had “dozens of opportunities” to develop relationships with other escorts, Cook surprised him. He liked her vulnerability but believed she sold herself short. “She didn’t feel,” he said, “she had any other ability to gainfully make money if she didn’t go out as an escort or [be] in the porn industry.” Cook said of that first meeting that because she and Spagnola had broken up, she was “available,” i.e., escort-available. Cook said she wanted to accompany Fanghella that evening but had nothing appropriate to wear. Then we’ll shop, Fanghella replied. First, Luca Luca. A rabbit coat. Next, Bergdorf Goodman (where Cook had her sizes on file), shoes, a choker, earrings, a bracelet.

Cook said that from “the first day I met him, I liked him. He was a fun guy to hang out with. But I wasn’t romantic with him.” Did she and Fanghella have sex that first date? For the entire time she knew him, Cook said, “We never had intercourse.” Yes, she was “nude with him, maybe four or five times.” And yes, they would kiss and caress with no clothes on. But they never had sex. “And no, I didn’t have oral sex with him.” (One lawyer, wary of Bill Clinton’s notorious evasion, had asked.) Fanghella’s story? Sex, yes, “the next day,” he said: that was the point of hiring an escort.

That evening Fanghella, Cook, a retinue of “actors and their wives,” and his “entourage,” gourmands and a wine buyer, went to Café Boulud, where, awaiting the triumphal hour, they ate, drank, and danced. And, according to Cook, many went in pairs to a private bathroom where she saw “piles of cocaine” set out for “the Fanghella party.” Though Fanghella couldn’t recall if he had cocaine that night, he did remember that “our dinner was approximately $120,000. We had some significant wines. A Pétrus ’61, a 1900 Châteaux Margaux at the close.” The tip — Zagat, he noted, says one should leave 20 percent — was almost $30,000. As everyone knows, midnight clanged in zone by zone around the world, and nothing crashed. At 7:15 the next morning, Cook left the Palace and Fanghella slept. Later that day he flew back to Carlsbad.

Cook called Fanghella on January 4 from New York saying she wanted to see him. He told her he would fly her out to PinnFund headquarters and the pair would then take a private jet to Las Vegas for a long weekend. Cook agreed, but Fanghella insisted that their relationship would not be escort and date. He wanted to “date her regularly,” expressing remorse that he would be stiffing Nici’s of one of their girls. Cook agreed — no more star-for-hire once she arrived.

It was at this time, Cook said, that she told Fanghella about Charles Spagnola: he was the man she had lived with for almost two years. But, for now, they were not together. Fanghella recollected that she told him she and Spagnola were finished. Spagnola — a delicate, muted man, whose cheeks dimple and whose layered locks nestle thickly onto the collar of his Armani dress shirt — has admitted to being, all along, Cook’s boyfriend and attorney. He said that Fanghella visited their Laguna Niguel house in January and was shown the room, decorated in Barbie motifs, where Spagnola’s daughter stayed on weekends. Everywhere were pictures of Cook, Spagnola, and the daughter. “You’d have to be blind,” not to have seen it, Spagnola said.

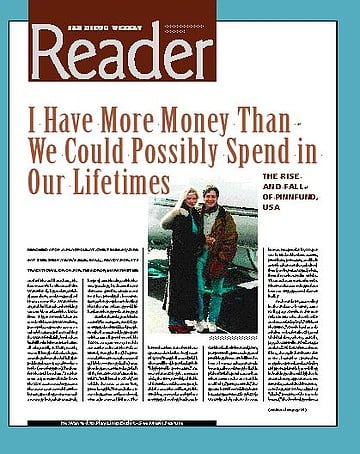

In mid-January Cook and Fanghella went to Las Vegas again, where Cook was shocked to see a “violent fight” between him and an ex-girlfriend, Lee Ann. But still Cook and he and others partied, four days’ worth, in a suite at the Bellagio hotel. Next the pair went to Santa Fe, New Mexico, where Fanghella bought her two shearling coats, a pair of Ugg boots, an emerald ring, a tanzanite ring, and several drawings by John Lennon. Then came ski trips to Beaver Creek, Colorado, ski outfits, four fur coats, a gold rope chain, a portable DVD player. Returning to Southern California, Cook parked in her driveway a 1997 Jaguar XK8, the first of six cars Fanghella would give her over the next six months. (Later he’d present her with a new house with a new driveway in which to park those six cars.) Perhaps embarrassed by the bounty, Cook told him, “You don’t have to do this to have me hang around you.” But it thrilled him, she said, to flash the AmEx card whether she wanted the stuff or not. More than once he told her, “Kelly, I have more money than we could possibly spend in our lifetimes.”

The way Fanghella spent money seemed not Cook’s to question. Instead, she encouraged him: on a cute Care Bear card she wrote, “I love being around you. I think I may be a little boring for your full-time life but I would love to see what happens. The ball’s in your court, sweetie.” Cook, though, had little idea how many courts, let alone balls, Fanghella was juggling. Two problems were gnawing at him. The first, Patrice had discovered her husband’s fling with Cook and, fed up, filed for divorce. She wanted a large portion of the $182,000 a month that she, her husband, and their children had lived on in Rancho Santa Fe. To ensure alimony and her one-third share of PinnFund’s value, Patrice had a forensic accountant catalog her husband’s spending. One discovery was that Fanghella had not paid any income tax since 1995; in fact, his 1040 listed the self-described millionaire’s 1999 income as $36,000. Patrice also learned that the IRS had been investigating her husband since 1997, so she hired a tax attorney to defend herself.

The other problem, Fanghella believed, was less serious. He had heard that someone was sending anonymous letters to several of the big mortgage warehouses from which PinnFund borrowed money to fund home loans. These letters said that two different sets of PinnFund’s financial statement for the years 1997 and 1998, prepared by the San Diego accounting firm Levitz, Zacks and Ciceric, were being disseminated. One set was false, the other set true. Fanghella thought questions about these “competing sets” had been put to rest the previous summer when Levitz, Zacks had discovered its 1997-98 report was falsified and the firm had resigned. But Fanghella’s chief financial officer, John Garitta, expressed concern. Who in PinnFund was circulating these letters and the phony report? Worse, who was falsifying it? Fanghella told Garitta the problem had been taken care of: the phony report and the letters were the work of a “rogue investor” in the company, and he or she had been “terminated,” that is, fired. Garitta should let it alone. Besides, Fanghella assured him, most warehouses had received the true set: that set showed PinnFund had made a healthy after-tax profit of $10 million in 1998 and not lost more than $27 million, which the false one claimed.

Super-Qualified Investors

Long before Michael met Kelly, the mortgage-lending firm PinnFund, USA, was the brainchild of Fanghella and Oakland real estate attorney James Lester Hillman. Today Hillman is a silver-haired 63. He has lived since 1965 with his wife and children in Oakland, where he sold securities in real estate partnerships. Fanghella, though not a lawyer, earned a B.A. degree in business administration from Thiel College in 1973. (He has claimed a “graduate degree in finance” from Monmouth University, but records show he attended only one semester.) Since 1978, Fanghella had sold securities in real estate projects in Illinois and California. He and Hillman met in 1983 and partnered to syndicate real estate. At one time both were licensed to sell securities by the National Association of Securities Dealers.

In 1992, with very few assets, the pair met again in Oakland, and Hillman told Fanghella he had an “innovative idea” — to create a home-mortgage lending business. Instead of borrowing money from banks, they would use money from private investors to fund loans. It was Hillman’s idea to ride the comet of subprime lending. Subprime is synonymous with less-than-perfect credit. The prime, or A, borrower is one with a good credit history, few debts, and no defaults. Subprime borrowers, given A- to C ratings, are a riskier clientele — mostly low-income individuals who are first-time purchasers or are refinancing. Some lenders target such borrowers with excessively high rates.

This business plan is solidly American — profit from consumers’ “credit blemishes.” By the end of 1999, consumer debt had reached $1.4 trillion, while consumer spending had exceeded personal income, creating negative savings. PinnFund would eventually boast in its ads that its rates were “an attractive alternative to the substantially higher interest rates charged by credit card companies.” (PinnFund did not specify how much lower its rates were.) Indeed, subprime lending was booming: home mortgages had grown from $200 to $280 billion during the 1990s, and the subprime sector had more than doubled its share to 20 percent.

Why did Hillman want Fanghella? Simple. Fanghella was, one observer noted, “an excellent salesman,” a talented motivational speaker who could rouse a staff of salespeople on this new idea and have them, in turn, sell mortgages to borrowers in distressed neighborhoods across America. Hillman had his own métier — convincing wealthy friends and relations to invest.

Fanghella set up Pinnacle Funding in 1993, in Del Mar Heights, and in 1998 moved the company to Carlsbad, across from Palomar Airport. He renamed the company PinnFund, USA. His associate, James Hillman — described by insiders as “Mike’s moneyman” — set up Peregrine Funding in Oakland. Hillman brought in the “platform capital” to “securitize” a loan. Under a Spot Loan Funding Agreement between Peregrine and PinnFund, Peregrine funded the loan before PinnFund sold it, in large bundles of loans, to one of the big mortgage buyers like GMAC or Bank of America on the secondary market. To entice borrowers, PinnFund staffed offices in low- and middle-income neighborhoods throughout the country with seasoned salespeople to seek the subprime client and, as one broker described it, “to bother with the paperwork and aggravation of closing.” The goal was to have Peregrine’s money complete the cycle — from origination to sale of the mortgage — three or four times a month. This turnaround was their advantage: the faster they turned the money, the more profit they made.

Each time a loan was sold, a 2 percent premium was earned, divided 75/25 between PinnFund and Peregrine. On a $100,000 mortgage, PinnFund received $2000. PinnFund kept $1500 and sent Peregrine $500 — Hillman got $300 and the investors $200. The investors, though, did receive more. They got an added 10 percent per year. All told, each $100,000 invested made roughly $1500 per month, $18,000 per year.

Eighteen percent per annum drew a lot of players. Dr. Bert Rettner, a 72-year-old physician in Los Gatos, California, said he was in “heaven” for three years, garnering monthly checks based on a $1 million investment. “Like clockwork,” Rettner received a check every 30 days for $15,000. Who else did Hillman solicit? His immediate family poured in $1.7 million and Hillman himself put up nearly $1 million of his retirement fund. Some of the biggest investors — tax attorneys, real estate developers, investment bankers, and accountants, one of whom worked on a multibillion-dollar debt-restructuring deal for Donald Trump — brought individual inflows of $11 and $27 million, while one family ponied up $60 million.

Under Peregrine, Hillman set up three subsidiaries, the “funding entities”: Allied Capital Partners, Grafton Partners, and (later) Six Sigma, which he opened to “super-qualified investors,” those with a $5 million net worth and a first-time $500,000 investment.

Hillman crafted an Exclusive Capital Raising Agreement between the investor entity Peregrine and the mortgage lender PinnFund. This agreement enhanced Hillman’s lucre as the only fund-raiser as well as the investors’ clout, since Peregrine’s money would be the only money that PinnFund could use to fund loans. The sum was kept in a special account, which Fanghella controlled, though Hillman and accountants — those at PinnFund and those hired to perform yearly audits — could review as necessary. When loans sold, Hillman earned a commission: during 2000 his haul rose to $975,000 per month. So flush with cash was Hillman (so in need of cash was Fanghella) that, according to Fanghella, Hillman agreed to loan him money, either from Peregrine or from Hillman’s personal account.

This was the money — an astounding $90 million, more than half of what Hillman had raised through 1999 — that Fanghella claimed Hillman had actually signed over, money on which Fanghella’s opulent lifestyle depended. With Hillman replenishing the trough at a rate of $10 to $15 million every month, Fanghella could respond to his wife’s ongoing divorce filings with blasé candor: “She knew that we had no income from PinnFund and that we were living an inflated lifestyle funded by borrowed money. It was — and is — all smoke and mirrors.” Fanghella’s bluster renewed Patrice’s ire. She rallied her lawyers to dig deeper. After all, as one of three shareholders in the company, some portion of that $90 million was hers.

From Group Sex to Holy Matrimony

By week six of Cook and Fanghella’s affair, mid-February 2000, the pair was aloft again. To New York, where Fanghella bought her a chinchilla coat, a Rolex watch, 20 outfits at Bergdorf Goodman’s, a birthstone ring, a diamond solitaire necklace, and a diamond baguette ring from Nally’s. Then to Paris, where she selected 25 outfits at Gianni Versace, Celine, and other stores, plus a Bulgari watch. Then, the grand prize: at Van Cleef and Arpels he bought her a 5.7-carat diamond ring, worth $350,000, as a promise that they would be married. A day later, a crack in the matrimonial crystal appeared at their Four Seasons suite: Fanghella had gotten drunk in the bar and Cook left, “to go upstairs and sleep.” Barging in at three in the morning and turning on the lights, Fanghella screamed, “How do you like being called Kelly Spagnola?” Cook said he must have rifled through her purse and found her credit cards, one stamped with that name. She recalled Fanghella’s raving and his “frothing-at-the-mouth demeanor”: “ ‘I thought you had cut him off, I thought you were through with him.’ ” The card’s imprint, she said, was mere protection: Spagnola wanted her to have it because her several porn-star aliases — Kelly Jaye, Kelly Lynn, Kelly Sabo — had caused her unwelcome notoriety.

Cook has denied any promise of marriage. Ever. To her, the ring — which she took — meant “his promise to me to change his behavior” — the violent temper she had just witnessed — “so I would want to be with him.” Apparently, even after this incident, she still “wanted to be with him” as much as she “wanted to help him.” Fanghella, on the other hand, has asserted that the promise of marriage was the point of his lavishness. “Somewhere between January and February,” he said, “we both realized we loved each other. I felt comfortable being in love with her, and I believed what she would tell me.” Namely, that as soon as their divorces were finished they would wed.

As their affair ripened, Fanghella said he and Cook enjoyed a few threesomes, that is, group sex. He said Cook liked hiring escorts for that purpose; in fact, she’d enjoyed multi-partner sex in her videos. When asked, during his deposition, just how long it was after he and Cook had group sex that he gave her this ring, Fanghella, with unembarrassable laughter, noted it was about two weeks.

“What happened in those two weeks that made the relationship move from group sex to holy matrimony?”

“That’s quite an assumption, there, counselor,” Fanghella replied. Still, he maintained, marriage did come up, when the two were considering property in Port St. Charles, Barbados. At the door of one condo, Fanghella asked Cook, “Do you like?” She said, “Yes.” So he bought it, a cool million. And, to cinch the pre-nuptial knot, he had another surprise: he was setting up an account with Barclays bank called the Blonde Angel Trust. This trust, promised to be stocked with up to $6.5 million in cash and other assets, would pay Cook an income for life so she would never have to work again. Depending on which of the pair you believe, the gifts of condo and trust did (Fanghella) or did not (Cook) carry a stipulation that they stay together for good.

Cook said Fanghella’s behavior changed after Barbados. He became “violent, crazy, screaming, crying. I assumed he was using drugs.” He felt “nauseated” when he combined his prescription medication for anxiety (Zoloft) with cocaine and then would go off the prescription. “ ‘I’ll stop taking [Zoloft],’ ” Cook recalled his telling her, “ ‘to control my temper because I’m not going to do drugs anymore. And that way you and I will be able to get along.’ ” He also agreed to restart rehab. She said by this time she saw Fanghella only because she “needed to keep him calm. I was extremely concerned about him doing something [bad] to himself,” and she told him she cared for him “as a friend.” Then, in late February, apparently beaten down by Fanghella’s manic life, Cook “ended” their friendship: she and Spagnola had patched things up. But then she called Fanghella back, saying she still wanted to help, maybe one day “be with him.” Fanghella thought they were on once more — and resumed sending her gifts.

During 2000, when Cook was in contact with Fanghella, she accepted every gift and claimed no knowledge that the money he spent on her may not have been his to spend. Fanghella told Cook that PinnFund had made him a multimillionaire; he told Patrice he was worth nothing, leveraged on loans from the trust account. Had this been known by the more than 200 investors who put money into Peregrine…but then it wasn’t known. What no one knew was that Fanghella, Hillman, and others had, according to one court document, “created and operated a classic Ponzi scheme,” bilking investors out of $330 million. In one of the nation’s largest mortgage scams ever, Fanghella and others were looting the investor trust account, falsifying audit reports and other financial records, lying on required filings with the Department of Housing and Urban Development (HUD), and jeopardizing the livelihoods of 450 PinnFund employees in 53 regional and branch offices in 45 states. PinnFund would pancake under its own weight of debt, scattering hundreds of victims and teams of lawyers through family court as well as civil, criminal, and bankruptcy venues of the United States District Court for the Southern District of California. (Dozens of depositions and thousands of pages of court records reveal the story of the fraud.) The company in its eight years never made a profit — a lie kept under wraps by certain PinnFund managers and sent to the warehouses in the form of falsified audits for the last two and a half years of the mortgage lender’s existence.

On March 21, 2001, the Securities and Exchange Commission (SEC) closed PinnFund and, one month later, froze the assets of PinnFund and Peregrine. The SEC wrote that “PinnFund and Peregrine had concealed more than $95 million in losses since 1997 and the transfer of more than $109 million to Fanghella since 1997.” Losses may have been the cost of doing business, but the transfers were illegal. Former acting U.S. Attorney Charles La Bella, known for a 1996 probe into Clinton/Gore fund-raising, was appointed receiver, in charge of retrieving as much money as possible to pay the snookered investors as well as PinnFund employees and creditors. When La Bella looked at the Union Bank trust account, the vault in PinnFund’s house where the investors’ money went, he found that of the $330 million that should have been there, only $1.5 million was left. Scores of the savviest investors had been had.

The SEC has said that Fanghella and “cohorts” falsified the Levitz, Zacks 1997-98 audit, which showed that PinnFund was losing money at a good $20 million per year. But — except for the auditors, the defrauders, and HUD — no one else knew one audit report from the other. Thus, Fanghella could claim that the falsified one was real and the real one (detailing the losses) was false. For many investors who had received checks every month, some for more than six years, the discovery that their funds were spent hit them like a bird flying into a glass window.

Within 24 hours of the SEC’s closure of PinnFund’s offices, Fanghella was on a plane for Barbados, where he had stashed several million dollars. There, he began transferring the assets of the Blonde Angel Trust from Kelly Cook to a Las Vegas flame, Denise Marohl. Within days he was e-mailing Corrina Licardi, a woman with whom he’d been living for several months in his Rancho Santa Fe condo, where he’d left her. “He went out to walk the dog,” she told a friend, crying, “and he never came home.” Fanghella wrote Licardi: “Send money. Sell my ring and send me the money.” This was his father’s diamond ring, which Fanghella’s grown son Vincent had taken — and refused to sell.

Fund or Die

Before the Ponzi collapsed, there was a mortgage-lending business up and running at the company’s 95,000-square-foot headquarters in Carlsbad. The two-story building tops a ridge along a wide, SUV-friendly boulevard, and there PinnFund created its corporate paradise — a nonsmoking, health-savvy organization that paid its workers good salaries and benefits, catered lavish yearly parties, and kept itself tech-current. Recalled one manager, the indefatigable Fanghella loved computers. “He was a geek. He would buy software just for the sake of having it. He liked the whistles and bells — bigger, better, faster, he would always preach.”

One of Fanghella’s corporate hats was tour director of PinnFund’s operation. He would, often with Hillman, who flew potential investors in for visits, usher guests through the building. They began in the basement, at the 5000-square-foot wellness center, with cardiovascular and weight-training equipment, showers and locker rooms, an aerobics floor, two on-site athletic trainers, and a certified nutritionist. There nearly half the 200 employees were “members,” signing up to attend twice weekly. And they did, working the stationary weights with a trainer or getting advice on low-cholesterol diets.

Fanghella and Hillman would show off the 40-seat theater, site of PowerPoint presentations and nutrition classes; the first-floor executive suites with an adjoining living room and its gallery of original oil paintings; and the food court, where employees ordered healthful cuisine, and maybe a glass of wine with dinner, if they were working late. “Long hours,” one employee told me, was “the nature of the job.” Investor tours, passing through hallways with photos of Fanghella speaking at charity events or of Hillman looking solemn, ended in the executive dining room. There food and wine were served and, according to Chris Belaire, Fanghella’s wine buyer, the boss liked to brag about his wine “verticals,” a collection of consecutive vintages from the same producer. (At his wedding Keith Grubba, PinnFund’s CEO, received from Fanghella a vertical of Grace Family Cabernet, valued at $40,000.) If potential investors took a liking to Fanghella’s vino bravado, he told Belaire to “bring out a bottle.” Fanghella would then, the group warming their throats, describe the miracle of Pinnacle Funding, that is, its years of unimpeachable returns. After all, that track record had compelled previous investors to send their buddies, the newest clientele, to the Carlsbad mecca to see the phenomenon for themselves.

Before Fanghella’s driver’s license was revoked, employees knew when he was in — his British racing green Jaguar was parked in its executive slot. Later, in the limo days, he traveled more and was in the office less frequently. When present, he would on occasion assemble the 200 employees below the staircase, and, perched above, he would launch into one of his Tony Robbins–like motivational tune-ups. One lawyer in the company recalled Fanghella’s “very spontaneous rah-rahs to the troops. Basically it was to quell rumors, to get the people to rally ’round the PinnFund flag. In those cases, he admitted that things were tough, but we would get through it. He was very effective.”

However, no matter a company’s amenities, no matter its leadership during crises, the mortgage-lending business is extremely stressful. Case in point was a poster above the water cooler displaying PinnFund’s mantra: “Fund or Die.” On dress-down Fridays, some employees wore their “Fund or Die” T-shirts, the words splattered with bloodstains. Write the loan, approve the loan, fund the loan, bundle and sell the loan — and start all over again. On top of that is a housing market subject to volatile interest rates. On top of that is a subprime clientele whose creditworthiness took time (often failing in the interim) to establish. On top of that is, at its maximum, a 650-employee payroll, the overhead, and the investors’ 1.5 percent by the tenth of every month.

In charge of those payouts was CFO John Garitta, whose primary job was to clean out Fanghella’s financial litter box. When he was first hired in 1996 — from a “temp-to-perm” accountant position, he became CFO in less than a year — it took him three months just to figure out what PinnFund did. Garitta’s primary and thankless task was to make payroll, as PinnFund’s money left the company daily for everything but payroll. An example: one day in late 1999, the comptroller, Valerie Frislie, begged Garitta to deal with the irate Madame Bridgett Girard from Paris, who was yelling at her on the phone. “ ‘Mike promised me this money. Where is it?’ ” “How much?” Garitta asked Frislie — $150,000. “You don’t have to talk to prostitutes,” Garitta told her. “That’s not your job.” During this period, Garitta said, “All Fanghella cared about was the hookers.” No wonder insiders re-christened the company “PornFund.”

Garitta complained that “we were not able to make our bills in December [1999, because] Mike was having his New York Christmas party where he spent $500,000, $600,000.” For that party, Fanghella had flown his wait staff from PinnFund’s catering division and, Garitta said, “bought them $1200 Tag Heuer watches. Do you know how ridiculous it is to see bus boys [in PinnFund’s executive dining room] pushing carts around with $1200 watches?”

Other outrageous expenses included Keith Grubba’s birthday in 1998, for which Fanghella flew 40 strippers with himself, Grubba, and company employees to Las Vegas to celebrate. The dinner at San Diego’s Laurel Restaurant, totaling $31,800 and a $5000 tip. The near-$100,000-per-year limo bills; the white Corvettes given to company brass; Fanghella’s $1 million 75-foot yacht, the Maverick, on which, allegedly, in late 2000, he was going to abandon PinnFund and San Diego.

All this deficit spending drained the coffers. When Garitta was asked if he was ever concerned that he wouldn’t meet operating expenses, he said, “I believe the question was, ‘Were there times when I was not concerned to meet operating expenses?’ It was a normal part of life where I didn’t know how I was going to cover my bills. I lost sleep over it.” During the last year, he went to work thinking each day would be PinnFund’s last. Garitta also said that Fanghella’s approach to PinnFund’s business was to control everything himself — never allow accounting, legal, human resources, executive, health, and other departments know what each other was doing. As to Fanghella’s honesty, Garitta declared, “If Mike told me the sky was blue, the one thing I was sure of was, the sky wasn’t blue.”

Beginning in summer 2000, things at PinnFund spun steadily out of control.

Auditors were in the building constantly. One PinnFund employee who worked in risk-asset management, with the Kafkaesque title of loss mitigation specialist, dealt with wire transfers of money for the loans. The auditors asked him for eight months’ worth of documents, which, after he checked, he discovered were missing. He was told to track this paperwork down, but his superiors stonewalled. On occasion, this employee (who requested anonymity) saw documents being forged. If there was a page from an insurance company, for example, that needed signing, workers would, he said, “forge a signature on it, just so they could get rid of the loan.”

A new crisis emerged in fall 2000 when employees noticed PinnFund’s 401(k) contributions had lapsed: neither the money taken out of the paycheck nor the amount PinnFund had to match was being deposited. A sign of a serious business slowdown, many workers stopped their 401(k) contributions. Some employees quit; others were let go; the turnover rate grew, then abruptly stopped: PinnFund quit hiring altogether. For their part, the employees knew little of the company’s woes. Sure, they questioned the lifestyle of the managers, the uncorked wine, the hookers in Fanghella’s office. But few suspected PinnFund wasn’t making money: in fact, every month management would publicize figures — $350 million one month — to reflect the loan volume.

As to why things were so bad, only Fanghella and a chosen few knew. Garitta has admitted to knowing how bad off the company was, though he told no one. He confessed to staying on only out of loyalty to fellow workers. Many employees suspected that PinnFund was failing but felt renewed effort and a sunny disposition might save the day. So they worked harder, and later, and still got paid: things couldn’t be that bad. They were young, too, the average age, 28. One worker told me that he worked every day for more than two years and “made a good salary” until a month before March 21, 2001. He asked, “How could PinnFund never have made any money and yet I was able to make enough to put a down payment on my first house?” The answer is, the money he was paid was never “made” by the company: it was merely transferred to him (and hundreds of others) from the trust account.

Two things most employees didn’t know. First, PinnFund never made a profit. Second, the entire time PinnFund was in business, the company was violating its own Spot Loan Funding Agreement by using “lines of credit” from warehouses — and not investor money — to fund loans. Financing with lines of credit is the usual means by which subprime and other mortgage lenders do business. The company signs an agreement with a warehouse, which puts up money — in effect, credit — so that the lender can fund the loans for its clientele. It’s called borrowing money to lend money. For example, a warehouse lender would extend to PinnFund enough money to fund dozens of home loans, and then PinnFund would sell a bundle of these loans to a buyer like Saxon Mortgage at a 4 or 5 percent profit. But this profit (it might be higher or lower depending on interest rates) was never enough to pay PinnFund’s and Fanghella’s bills.

It might be argued that Fanghella believed he could make more money by using warehouse lines of credit, an unlimited amount, instead of relying exclusively on the investors’ money. But was Fanghella even interested in PinnFund’s making money? When Garitta told Fanghella that PinnFund “should be cutting checks to him based on profits” and not taking monthly withdrawals from the trust account, “he looked at me like I had two heads. It never occurred to him to make a profit for the company.”

But profit, as differentiated from investor cash, is what Patrice, the investors, Hillman, the employees — everyone — thought PinnFund was generating.

The Possibility of Fraud May Exist

In March 1999, two years before the SEC shuttered PinnFund and all but $1.5 million of $330 million was gone, Hillman set the table for Peregrine and PinnFund’s demise. Incorporated under Peregrine, the three funding entities — Allied Capital, Grafton, Six Sigma — were private investment trusts, which, because of their relatively few participants, were not audited at first. But once these entities’ holdings burgeoned into the many millions, investors clamored for a third party to see whether the money was where it should be and doing what it should be doing — safely funding loans. PinnFund had already been audited by Levitz, Zacks, and, by 1999, several investors were pushing Hillman to have the cash-fat Peregrine partnerships audited. So Hillman hired PricewaterhouseCoopers, one of the Big Five accounting firms, alongside Arthur Andersen and Company, which is facing civil penalties for allegedly constructing complicated partnerships that kept Enron afloat. Hillman asked for a “minor” audit of the funding entities Allied Capital and Grafton, for 1997 and 1998. Minor, Hillman said, meant “to verify that we recorded investor money” properly and “to substantiate when PinnFund sent us money for monthly distribution.”

Pricewaterhouse’s Todd Goldman was the auditor in charge of this account. He told Hillman it shouldn’t take more than three weeks. But, when Goldman looked at what he believed was Levitz, Zacks’ 1997-98 audit report for PinnFund (it is not clear who sent this to him), he discovered a problem. The audit listed a $67 million liability as part of “revolving warehouse facilities.” Goldman requested clarification from Hillman.

According to Forbes magazine, “Hillman sent a second set” of the 1997-98 audit with an added footnote. The footnote stated that the $67 million was part of a $78 million “credit facility, provided by private sources (Allied Capital Partners and Grafton Partners). The unused portion” — $11 million — “of the credit facility is held in trust for PinnFund, USA.” Goldman wondered where this $11 million was. It was not shown as “cash,” where it should have been.

On June 4, 1999, Goldman sent a memo to Peregrine’s director of operations, Peter Kodzis. He wrote, “As you know, there seem to be several versions of the PinnFund financial statements.” Goldman requested that Kodzis ask Levitz, Zacks to send him its numbers directly; Goldman also wrote, “We will not ask questions about any other aspect of PinnFund’s business.” In his memo, there was no mention of fraud. Goldman received yet another report, this time from PinnFund directly, with another explanatory footnote in place, clarifying the missing $11 million.

Still dubious about PinnFund’s books, Goldman called Levitz, Zacks in mid-June and spoke with Kim Ufford, Levitz, Zacks’ senior manager in San Diego, who had helped produce the 1997-98 PinnFund audit. Apparently Goldman told Ufford that PinnFund’s loans were being funded by the two funding entities, Allied and Grafton. Ufford (who along with Stanley Levitz has been contacted repeatedly for this article and has not responded) told Goldman that he didn’t know Peregrine was the funding source for PinnFund’s loans. Ufford believed PinnFund was using warehouse lines of credit. John Garitta testified that Ufford did know about Peregrine: “He knew the entities [Allied and Grafton] because he would see the wires coming in, so he was aware of who they were.” Moreover, in Levitz, Zacks 1997-98 report, the following is stated: “The Company [PinnFund] has also improved its coordination with investors and its underwriting procedures to accelerate the sale of loans after funding.” This sounds as though Levitz, Zacks understood PinnFund and Peregrine’s structure. What Ufford and the firm did and didn’t know at the time of the audit is central to Levitz, Zacks’ civil liability: Did Levitz, Zacks know there were investors who should have been notified of a potential fraud? Certainly Pricewaterhouse knew.

In court documents Ufford said that, during their phone call, he and Goldman “established that none of the pages were the pages associated with the correct audit record [done by Levitz, Zacks] or the correct financial statements.” Goldman had a phony audit.

The original audit for calendar year 1998 included a paragraph that stated the company’s “significant operating losses raise substantial doubt about its ability to continue as a going concern.” The phony audit omitted the paragraph. The original showed a retained deficit of more than $27 million. The phony showed retained earnings of $10 million. A $37 million chasm was too wide for any auditor to ignore.

On or about June 22, 1999, Goldman, with his associate David Chrencik, had a meeting in San Francisco with Kodzis and got Hillman on the line. The gist of that conference comes in an internal memo Chrencik sent to his supervisors and to Goldman. In it Chrencik stated that he and Goldman told Hillman that “as management of Grafton and Allied, [Hillman] should be more concerned than us over the audit report inconsistencies and the apparent inability or unwillingness [of PinnFund] to resolve this, and that this situation indicated that the possibility of fraud (and I used the word ‘fraud’) may exist or that the amounts advanced to PinnFund may not be recoverable.” According to Hillman, Goldman and Chrencik never used the word “fraud.” The memo went on: “Jim’s response was that ‘this is a risk in the business’ and should not be of concern to us.” Hillman then fired Pricewaterhouse and requested all documents the firm had received be returned.

The SEC claims that Hillman not only sent the false financial statements he had on to new investors, but he also told them — knowing the audit of Peregrine had not been completed and the possibility of fraud had been raised by Pricewaterhouse — that “Peregrine’s records were accurate and compliant with standard accounting procedures.… Peregrine maintained effective internal controls over [its] financial reporting.”

In San Diego, attorney Stephen Gentes sent a letter to PinnFund in September 1999 stating that Levitz, Zacks was resigning as PinnFund’s auditor. He charted in detail the differences between Levitz, Zacks’ financial statement and the phony one. Gentes followed up with a similar letter to the Office of the Inspector General, the investigatory arm of the Department of Housing and Urban Development. He sent this letter because Levitz, Zacks had discovered a potential fraud at PinnFund. Gentes received only an acknowledgment from HUD of his 1999 letter and, for months, no word of an investigation. Thirteen months later he sent another letter underscoring HUD’s own guidelines that “if the auditor becomes aware of illegal acts or fraud…the auditor should promptly prepare a separate written report.” The day after this letter went to HUD, October 5, 2000, Gentes sent letters to the three funding entities, notifying them of the fraud. The investors, however, didn’t see these letters until after PinnFund was closed.

Michael Fluharty, public affairs spokesperson for HUD, told me that HUD first certified PinnFund as a “Non-Supervised Mortgagee” in May 1996. PinnFund was exempt from “certain state licensing requirements” and eligible for some FHA loans or programs. HUD decertified PinnFund on October 28, 1999. Fluharty said the decertification was the result of “a deficiency in liquid assets or net worth or both.” Only “subsequently,” he went on, did HUD receive “a memo from the regional Office of the Inspector General in San Francisco forwarding a letter” that Gentes had sent. “It was alleged that PinnFund had submitted bogus audits.”

In Oakland, in July 1999, Hillman replaced Pricewaterhouse with the auditing firm Rooney, Ida, Nolt & Ahern, or RINA, but did not tell the new firm why Pricewaterhouse was fired. Mike Desai was in charge of this audit and, in early 2000, he finished a year-end audit of Peregrine for 1999. During 2000, Desai began seeking Fanghella’s help in completing a more expansive audit of how Peregrine and PinnFund operated together, which several investors had wanted. One of his requests was for 150 loan files and a spreadsheet of those loans by purchaser, that is, companies like Saxon Mortgage who had bought or were buying PinnFund’s bundled loans. According to Desai’s testimony, Fanghella stalled for much of 2000 — it wasn’t until January 2001 that the loan files were sent.

Meanwhile, Desai did verify that investor money was being wired to PinnFund and that the yields PinnFund paid were “properly distributed.” No surprise there. Finally Desai had a 40-page list of loans broken down by eight mortgage buyers — Associates, GMAC, Saxon Mortgage, Household Finance, Greentree, Life Savings Bank, Advanta, and Mortgage Guaranty — which “held…loans for purchase or review from PinnFund.” During a week in February 2001, Desai attempted to fax each of these companies from the list Fanghella had provided. None of the numbers worked. In the subsequent two weeks, new lists came from Fanghella’s office and Desai tried again. “Either the fax wouldn’t go through,” he said, “or I got somebody’s voice mail number or I got a message saying the number doesn’t exist. I was very distraught. I started crying because I had a gut feeling that I had been victimized by Fanghella.”

The Most Expensive Lay in the History of Man

After several trips with Michael Fanghella to luxury destinations in Europe and the United States, Kelly Cook said that by March 2000, her “friendship” with him had waned again. One reason: she began screening his calls and — hearing him rage — she refused to see him until he got help. Transcripts of Fanghella’s phone calls reveal that, as one civil litigator said, he was “pathetically, desperately, in love with her.” On one tape Fanghella said, “I found you as a prostitute but know you now as a beautiful person.” On another, he threatened to put her away for 10 to 15 years and to send copies of her videos to her mother, who, apparently, has never known of her daughter’s career. Despite the storm between them, Cook’s rejection merely supercharged Fanghella’s buying. To woo her back, he had a woman at Bergdorf’s buy clothes Kelly (and he) would like: boxes of skimpy outfits arrived at her home, tags on, prices snipped off. For much of year 2000, he spent $30,000 per month dressing his goddess. He next gave Cook a Porsche Boxster, a BMW X5, a Jaeger-Le Coultre watch, a sapphire-and-ruby tennis bracelet, and a Volkswagen Cabriolet for her housekeeper.

In April, Fanghella invited Cook to Hawaii for a vacation and she met him there, secretly bringing Spagnola. Cook said that when Fanghella found out, he started “screaming,” requiring “security to escort him to his suite.” Supposedly Fanghella stood outside the room of another couple, whom he heard in flagrante delicto. He yelled at the door, “I know that’s you in there, Kelly. What are you trying to do, flaunt it in front of me?” Cook believed Fanghella saw her ongoing relationship with “Chuck” as competition: “If he could do better things for me, buy more things for me, or whatever, I would choose him over Mr. Spagnola, and I said, ‘It’s never been about that. I’ve made a decision that I’m with him. I still like you.’ ” His wrath renewed, Fanghella “would make [Spagnola] pay,” she said. “He would see him in prison, he would kill him if he ever got his hands on him.” Fanghella continued to call, threatening to kill himself, at one point, saying he had cancer and nine months to live. (No evidence has appeared to verify this.) Cook recalled, “I wasn’t as mean to him as I should have been.”

Fanghella decided he could finally hook Cook with one more benefaction. (It’s important to note that most gifts were what he called “shared” and “in contemplation of marriage.”) He would buy a dream house, where they would live forever. It was in Laguna Niguel, in an area called Bear Brand, on a street called Inspiration Point. At 30,000 square feet, the gated, one-acre “Tuscan Country Villa” included seven bedrooms, ten bathrooms, six custom fireplaces, a four-car garage, weight/workout room, theater/game room, wine cellar, office/library, guest wing, pool and spa, sports court with arena seating, and huge entertainment area — not to mention the master bedroom and bathroom done in “rare Azul ~ Macumba Brazilian marble.” Cost: $5 million.

Tim Filer, a PinnFund factotum who often traveled with Fanghella, has been quoted as saying that “Kelly runs cons on people” and that Fanghella knew this and pursued her anyway. The clearest proof for that charge comes from a 19-page letter Cook faxed to Fanghella on May 9, 2000. In it she writes, in wide-ovaled, right-tilting, spacious script, “I would totally understand if you would want out and say it’s not worth it, but I do still like you and I do want the ‘American Dream.’ But right now I don’t trust your behavior.” “Michael, I am not your property. Just because you buy me things does not mean you can control me. Maybe you don’t realize you are controlling me.” “I have told you over and over again that it bothers me when you call me fiancée. I have never ever said that. I, in fact, told you that when you bought the ring, ‘Don’t buy it,’ if that is your intention because I would never, never be engaged to someone who I knew for one and a half months. You absolutely can’t keep pushing me on all these issues if you want a lifelong commitment. It takes more than a couple of days or weeks.”

By mid-letter Cook gets specific. “So answer me honestly, absolutely honestly, to each and every question, and please fax back to me. 1) When do I get all the Blonde Trust info? 2) Where is the $6.5 million you kept telling me is in the Blonde Angel Trust? 3) If the Barbados house deal is complete, why hasn’t the stock [property?] been transferred to the trustee? [the trustee was an attorney-client trust account of Cook and Spagnola’s].… 6) You told me in Hawaii that you were going to put $2 million plus another $1 million you had designated to be put in my account in Barbados. 7) I do not want the Bear Brand house in my trust or name unless first, I have one-year association dues and one-year property tax in escrow and, second, I have what you told me it would take — $1 million — with an interior designer to decorate that house.”

The letter continues. “Michael, I want you and I want to be with you but I feel so worried because I never know what is going to set you off. I want a happy, free-spirited life. I may want a child. I wish you all the best if you want to walk away. But I do care very, very much about you, if not, I would not have stuck around this long.

“By the way…I would like Chuck to be able to talk to you about an agreement [that would express] my intentions in the future regarding you and I. Just in case you wondered, I now feel like I have every car I could ever possibly want, but if you were ever interested, I still am crazy, crazy about the Viper GTS in Red (ha, ha). And maybe eventually, if things work out, we could get a Bentley.”

Amazingly, Fanghella’s response to this letter was to accede to her demands. He wrote on May 11 that “everything I have will be yours in time. That time-frame is based on legalities and ability to put together documents that will protect you and even me. I remain forever in love with you.” He was still busy organizing the Blonde Angel Trust, and he had earmarked money in several different accounts for the Barbados and Laguna Niguel homes to prove his “loyalty and honesty.” He even got her the Dodge Viper GTS, in red, and eventually another one — a Viper RT/10.

Fanghella has denied saying that 2 Inspiration Point would be hers, in toto. Midway through the purchase in early June, Fanghella believed Cook had falsified the escrow papers. She and Spagnola had registered the title in their partnership, Reliance Holdings, and not in Fanghella’s name, as he had directed her. He said that she had signed his name to the “Amended Escrow Instructions” without authorization. To cancel the purchase and their relationship, an enraged Fanghella faxed her a letter. “I believe you have done yourself and those you’ve loved a great disservice,” he wrote. “I was ready to spend eternity, trying to please you, but it seems you would have rather had all of the benefits but none of the responsibilities.” Near the end of the letter he listed most everything he had given her to date — 2 Inspiration Point had not been purchased, but the list ran to more than $2.5 million in cash and gifts — and he commanded her to return it all. He ended with, “Hell, you got something out of it. You were [the] most expensive lay in the history of man.”

Okay, she said, she’d give everything back. Fanghella said fine. But that’s not what happened. Instead, she made up with him (purportedly to “keep him calm,” afraid he would “go off the deep end”) and accepted more charity: $108,000 in cash to pay off the mortgage of Cook’s elderly mother in Georgia and $318,000 to pay off the mortgage on her home, which was still owned by her ex-husband. Then Fanghella gave her a PinnFund American Express card, part of an account that several PinnFund employees used to pay expenses. Fanghella’s orders, now that they had made up: buy only furnishings for the house. Cook launched into the shopping spree of a lifetime. In June 2000, she bought $1.18 million worth of stuff, mostly (but not all) for the house. (The multi-page list — gym equipment, high-end electronics, crystal hollowware, china, a grand piano, Jet Skis, a pair of SunStar Speed 175 Body Tanning Units, a 1985–1996 vertical of Marilyn Monroe Merlot wine — reads like a year’s take on The Price Is Right.) In her eight months on Fanghella’s dole, Cook collected, not including houses and offshore wire transfers, more than $5.5 million. Cook had learned from the master: while she charged $1.18 million in June, Fanghella had charged $778,000 for his personal expenses.

In yet another convolution, Fanghella took Cook’s suggestion that Spagnola draw up an agreement about “Kelly and Michael’s future” because she wanted to protect — read, keep — her many gifts. Fanghella paid Spagnola a retainer of $200,000 to write a “Satisfaction of Debts and Release of Interests” for Cook that would say what he’d given her was hers. Spagnola did so, he testified, believing she owned every gift and 2 Inspiration Point. “I do not expect the return of any of those items listed at any time,” the document reads, because “as a direct result of Kelly’s kind and loving acts, I have regained control of my life after a long period of self-doubt and turmoil.” Fanghella said he signed this declaration in Cook’s presence on June 27, 2000, after hearing Cook tell him, “ ‘I love you, I want to be with you, Mike, trust me.’ ” She had agreed, Fanghella said — Cook denied it — to take the document to Spagnola for changes Fanghella requested.

A week or two prior to June 27, Fanghella had finally suspected Spagnola and Cook of living together — with Spagnola “driving the Beemer” — and Fanghella hired a private investigator to spy on them. A neighbor, Laurence Uyeda, noticed the man watching Cook’s house and spoke with him. Uyeda said that Spagnola had lived with Cook at the “tired-looking” Westfield house continuously for two years. Also, that summer, Uyeda noticed “three new cars in the driveway and a lot of construction going on. We thought she had won the lottery.” Uyeda heard from another neighbor that Kelly had received what that neighbor called an “engagement ring.” Who bought it? the investigator asked. The other neighbor said, “Her benefactor.” Told that Spagnola had been living there, Fanghella met with Uyeda, who, confirming his fear, noticed that the revelation stunned him.

Within the week, a list of Cook’s Vivid videos appeared in neighbors’ mailboxes. Fanghella denied circulating the list. “Miss Cook,” he said, “is a very well-known movie star, and you can find over 15,000 pictures of her on Web sites.” Seemingly, he believed this was common knowledge to anyone with a computer. After the video list appeared, Cook hired a bodyguard.

In July, Uyeda said, Cook and a few other neighbors came to his home and “started calling me names, telling me I’d blown the whole thing.” Cook, he said, called him a “Nazi traitor.” One neighbor told Uyeda that “ ‘Michael’s a bad person; he’s trying to kill Kelly; he’s not stable.’ ” Uyeda told them he wasn’t snitching on anyone. Cook yelled at him: “ ‘It’s all blown up!’ ” And the neighbor added, “ ‘All of it’s falling down!’ ” Soon after, in Uyeda’s mailbox, the Fanghellas’ divorce papers appeared. He said Cook and her housekeeper put them there, telling Uyeda later that they wanted him to know “what type of person Michael is.” (In one of the stranger plot twists, that housekeeper, after leaving Cook’s employment, showed up at Fanghella’s office and offered to provide information on how to break into 2 Inspiration Point. Her price, $100,000. Fanghella didn’t bite.)

In mid-July, Fanghella canceled the American Express card because he had finally seen Cook’s $1.18 million June bill. Fanghella was livid when he saw two nonhouse items, a pair of Jet Skis and two season’s tickets ($12,500 each) to the Mighty Ducks, Anaheim’s pro hockey team. He said Cook threatened him then, saying that if he didn’t give her the use of the card back, it proves “you don’t love me.”

All that summer and into the fall, Cook and Spagnola cozied up at 2 Inspiration Point. To enshrine their treasure, the pair placed, above the living room mantel, a framed, enlarged box cover of Cook’s “workout” video, Malibu Hardbodies 2: Behind the Scenes, a “revealing look” at a woman whose “routine is hardly routine.” The image shows Cook wearing a muscle gym suit, a sort of Spandex bib that barely covers the tips of her nipples and the Y of her crotch. With greased and glowing body, her hair is notably contoured in wisps of softness around her sunken-eyed face. With the gift of a $5 million Tuscan Villa to Cook and Spagnola, plus a million dollars in furnishings, the PinnFund saga had become, as Steve Owen, one of the receiver attorneys, told me, “the story of a man who was taken for everything he wasn’t worth.”

He Was Somehow Able to Delude Himself

One investor, who has known Hillman for 25 years and would become the most suspicious of Hillman and Fanghella’s association, was Tom Frame, a nonpracticing attorney. In the early 1970s, Frame’s business partner, Eric Laub, took a college course from Hillman in buying and selling real estate. Laub was impressed and invited Hillman to join him and Frame in further deals. Frame recalled that the trio “fell into a friendship and a business relationship,” creating TransCentury Property Management in 1973. Together they purchased residential real estate in Texas and California, sold shares to investors, managed the properties, then sold them, usually at a good profit. In 1983, Frame left syndication to focus on managing his residential units. Laub and Hillman, with Tom Hix and Michael Fanghella, started TransGroup Securities in a second real estate syndication. Hillman borrowed $500,000 to fund his interest in TransGroup. In 1986, the entity fell under investigation by the National Association of Securities Dealers, where all four were licensed.

The holding investigated was Burnham Park Plaza, Ltd., a Chicago building that TransGroup was “sponsoring.” The National Association of Securities Dealers found the four guilty of “not depositing investor funds in an escrow account” and of “not return[ing] funds to investors.” They were fined a total of $15,000 and censured. The men had to pay back the investors and relinquished their securities sales licenses. In addition, the censure and fine occurred during the late 1980s, when real estate was overbuilt and a recession imminent. Helping out his friend Hillman, Frame bought Hillman’s interest in TransCentury because “Jim didn’t have the reserves that Eric and I had from previous real estate deals.” Hillman paid his debts by “going back to lawyering.” Frame also recalled Hillman during this debt period to be consumed by work. Often unable to sleep, he’d arrive at the office at three in the morning. Hillman, who filed for bankruptcy protection twice, may have told his friends in 1992, the year before PinnFund and Peregrine began, that he was broke, but his recent SEC declaration indicates that he had $400,000 in several interest-bearing investments in 1993. Fanghella filed Chapter 11 bankruptcy to reorganize his personal finances in 1992, around the time he and Hillman began their venture. Though Fanghella’s bankruptcy was dismissed, he re-opened it in late 1996 but never completed it.

Once Peregrine was incorporated, Frame, who kept a “close friendship” with Hillman, invested $2.8 million in Grafton, one of Peregrine’s three funding entities. In 1999 he put in $3 million more, transferred the funds to Six Sigma, then followed with $1.35 million in late 1999 and again in 2000. Frame said his total, $7.9 million, represented a “major investment,” 30 percent of his assets and nearly all his liquid assets. Frame loved the 18 percent return and was attracted to the business acumen of the two men: “I had a good feeling for both Jim and Mike, and I’d done my homework over the years. I had RINA do a procedures audit,” before adding more money in 1999. Frame discovered from RINA’s report that PinnFund was running on a “fairly thin profit margin.” Frame’s initial concern was that this “thin profit margin” meant that “if Mike had a hiccup, his creditors would come after our [the investors’] funds.” So to help secure the money, Frame suggested tightening the original trust account agreement. Frame called it putting a “Chinese wall” between PinnFund’s operating expenses and the investors’ money. That way, if a problem arose, it would be “a lot harder for PinnFund’s creditors to get the money.” Frame said that Hillman trusted Fanghella to control this account because Fanghella promised to “securitize” with documents any money that went to fund a loan.

Always looking “to see where the risks may arise,” Frame said his suspicions were raised in July 2000 when he received the 1999 year-end report of San Diego’s A.V. Arias, PinnFund’s newest auditor. He composed a spreadsheet to project PinnFund’s growth based on the amount of capital invested. “The numbers [Fanghella] reported as income were way off from the numbers he should have reported as income had he done the volume he was reporting.” For 1999, the volume was purported to be $4 billion. Frame did a quick “back-of-the-envelope calculation” and found PinnFund should have gotten $80 million, that is, the 2 percent premium. PinnFund was reporting half of that. Frame said, “That bothered everybody,” including the biggest players — Eric Laub, who had invested $7.7 million; Bruce Miller, $27.3 million; and the Ronald VandenBerghe family’s six investments, totaling $60 million. “It was not something we wanted to believe.”

During the final months of PinnFund’s operation, Frame decided one day to check the pipeline, the monthly reports that “proved” PinnFund’s volume. At random he sent letters to 25 borrowers, asking each to confirm his or her loan amount. “I got back 17 responses,” he said, “and 7 or 8 of those had envelopes marked ‘Address Unknown.’ ” Fanghella or someone in PinnFund had been padding the pipeline, probably with names scoured from the phone book.

Frame said Hillman should have been “checking the trust account. Because if he [had], he would have shut it down in 1998,” when the first withdrawal (Frame later learned) went to payroll. Such an expense was forbidden by agreement. Frame said if Hillman were checking the trust account he would have seen checks going out to girlfriends, wine purchases, American Express card payments. Obviously, he wasn’t checking.

When the Los Angeles Times reported the closing of PinnFund on March 22, 2001, Frame said, “I almost threw up my breakfast.” The next night he, other investors, and Peter Kodzis met with Hillman, who had returned to Oakland from Borneo, midway through an around-the-world trip. Frame recalled that “everybody was shell-shocked. Hillman said, ‘Everything is secured, the money is in the trust account, we shouldn’t have any problems.’ He was happy everything was being frozen by a receiver.” At first, Frame and other investors consulted RINA’s latest audit, which they had just received, and found their money accounted for. It didn’t dawn on them that the money could be gone until they looked at all of PinnFund’s financial records. Frame described it like this: In one ledger there was, under credit, loans from Peregrine; under debits, “expenses for girlfriends, houses, Barbados, condos. It was obvious it had all been diddled away.” Once the realization sunk in, Frame endured “many days of self-loathing. All of us went through it. For something of this magnitude to have slipped by us — I know, that dented my self-confidence.”

Today Frame believes that Hillman would have been “an absolute mental wreck had he tried to hide this thing, had he really known.” Frame doesn’t know if the fraud worked with or without Hillman. He feels Hillman “hid his head in the sand” but also believes he “actively misled us. Whether it was too trifling a problem and Mike assured him everything was okay” or something else. “I just have a hard time, after knowing the guy, unless he had a mental lapse — if he really knew, he would not have been on vacation.” Frame says he never knew Hillman to have a mental illness, suffer depression, or drink much. “He was never a high liver. I’m guessing he was somehow able to delude himself.”

Sophisticated Victims

At 34, Nicolas Morgan is a lanky, mast-shaped senior counsel at the Los Angeles office of the Securities and Exchange Commission. Morgan began his career in private practice, bringing lawsuits against government agencies like the Army Corps of Engineers. Later he decided to work for the SEC because he is “enthusiastic about going after the kinds of people who deserve the attention they too often don’t get.” Of the 139 employees at the L.A. office, Morgan is one of 59 lawyers, most of whom sue for securities violations. The SEC has two units: investigators, who find violations and issue subpoenas, and trial attorneys, who take violators to court. Morgan has devoted a year of his life to suing James Hillman on behalf of the Peregrine investors. With Fanghella no lawsuit was necessary. When summoned by the SEC, he failed to appear, so a federal judge issued a default judgment for $109 million in missing investor money. The money — and Fanghella — were gone.

Morgan told me that all securities offerings require registration. The majority of these offerings are public, that is, those made to unaccredited investors (you and me) who buy, for example, 50 shares of Microsoft. Securities offerings can also be private. Private sales are for accredited investors, most often individuals but also limited partnerships or the employee benefit plans of institutions. Individuals are accredited under any one of the following rules: $1 million net worth; an annual income of $200,000 or more; or the “knowledge and experience” to evaluate the “merits and risks of the prospective investment.” One might interpret the final rule as the wherewithal to lose one’s money and survive financially. Thus, the SEC’s rules are intended to protect the unaccredited: if there are fewer than 35 unaccredited individual investors in a sale, the securities broker fills out Form D. On it she states her offering is exempt from further registration. In essence, she registers her exemption.

Hillman’s securities sales under the corporation Peregrine were private. But by selling those securities, Hillman had violated two SEC regulations. One, because he had lost his license to sell securities in 1988, Hillman failed to comply with the National Association of Securities Dealers’ requirement to be licensed, a fact no one seems to have checked. And two, because there were more than 100 unaccredited investors who put their money in Peregrine (some as “little” as $5000), Hillman should have had these people registered and told his accredited investors about their status.

Morgan wouldn’t say when his L.A. office got wind of trouble at PinnFund, though he did direct me to several “sophisticated victims” who during the latter half of 2000 were figuring it out for themselves. He did say that the L.A. office filed for subpoena authority on November 13, 2000, and three months later filed a subpoena enforcement action, which got the court involved and the case became public. I asked Morgan whether more disclosure, more enforcement, more investigators, could have ended this Ponzi sooner. “I don’t think so,” he said. “With guys…who could fabricate the truth and withhold information from the investors, I don’t see how [to stop it]. There’ll always be fraud. I suppose we could eliminate exclusions on registration requirements. But these guys would still lie.” The truth is, he said, Hillman and Fanghella “flew beneath our radar. These investors got what they thought were correctly audited financial statements. Hillman and Fanghella, until the end, gave all the right signs. That level of sophistication goes well beyond what we are accustomed to seeing.”

Among the first to alert the SEC was Dr. Abraham Helfenbein, an 81-year-old retired dentist. Helfenbein put $25,000 in Grafton Partners early on and collected a steady 18 percent for five years. In March 2000, he noticed in one of Peregrine’s newsletters that there were only 100 salespeople selling mortgages. “I couldn’t figure out how 100 people could generate all that mortgage money they were financing.” Helfenbein did the math. He discovered that for Peregrine to continue paying 1.5 percent monthly interest, PinnFund had to be (a) selling more than $300 million in mortgages per month (which it claimed) and (b) completing 4800 different mortgages per month at an average of $70,000 per loan (which was never claimed). That many mortgages meant, for Helfenbein, each of PinnFund’s 100 salespeople would have to complete more than two per day. “You’d have to have a staff of 10,000 people” to sell that number, he said.

And yet Helfenbein’s investment, even as he was talking to the SEC, rose to $100,000. Why?

“I realized that I’m greedy,” he told me.

“Weren’t we all in the 1990s?” I replied.

“Aren’t we all still greedy?” he said. “That’s our downfall. I think all of us investors are greedy. You also have to remember that, as a dentist, to save $100,000 to invest — in my day, fillings were $20 at the most. Right? To get $100,000 in profit with an overhead of 65 percent” — Helfenbein practiced for 30 years — “can you imagine how many fillings I had to do to save $100,000? And remember, I started with $50 and a pregnant wife. To think I was stupid enough to think there’s a free pot of gold at the end of the rainbow — and that 15 years before, I lost 100 grand in a similar operation.”

Helfenbein once warned his accountant, Stanley Sloman, about the potential for fraud at PinnFund. An investor, Sloman had toured the offices in Carlsbad, where many of the 200 employees he saw sported the happy faces of satisfied workers. Helfenbein asked Sloman later whether he remembered The Sting, with Robert Redford and Paul Newman. In it the two play swindlers who enact a confidence game on a wealthy investor by creating an elaborate bookie operation with men betting on ponies while the race is called behind a curtain. Sloman said the comparison was nonsensical, reminding Helfenbein that “there are people who’ve got $1 million invested [in PinnFund], more than you and me together. They’ve investigated it.” Fanghella’s company had to be legitimate, Sloman implied, because the richest among us don’t place their money with losers. Another investor, who asked for anonymity, echoed the sentiment: “This was one of the great scam deals of all time.” Smart guys in Oakland were running an operation in which “I had all the trust in the world.”

Even those smart guys might be dumbstruck at how the Ponzi retained its legs. In October 2000, an employee from Impact Warehouse Lending, a company PinnFund had approached for a line of credit, contacted Stephen Gentes, Levitz, Zacks’ counsel. This person told Gentes that she’d received two audited statements, both on Levitz, Zacks letterhead, one showing a 1998 loss of $27 million, the other a 1998 gain of $10 million. The two reports shocked her, so she had contacted Keith Grubba, PinnFund’s CEO. According to Gentes, Grubba told her that the audit with the profit was the true one. Several other parties — three new investors and two warehouse officers — were burning up the lines at PinnFund: they, also, had conflicting sets. Allegedly, Grubba told the woman from Impact that the false financial statements were true and the true financial statements (those prepared by Levitz, Zacks) were false. This evidence showed the fraud was being perpetrated by people other than Hillman and Fanghella. (How easy was it to falsify the audit reports? Fanghella or an understudy, the SEC alleges, removed pages from velo-bound binders that showed the losses of his company and replaced them with altered computer-generated versions that glowed with earnings.)

Further havoc reigned after the San Diego accounting firm A.V. Arias released its 1999 year-end audit report in May 2000. Arias found that PinnFund had lost $59 million in 1999. In October, sundry warehouses and investors still doing business with PinnFund received original and falsified versions of the Arias audit. The false version reflected that PinnFund had earned $12 million in 1999. Once tipped off, Arias resigned as PinnFund’s auditor and, like Levitz, Zacks one year earlier, requested its reports be returned. Also like Levitz, Zacks, Arias did not notify investors of these conflicting financial statements.