{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Close to Home — What it’s like on the street where you live

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Patte and Len Purcell – 37 months in federal prison for getting caught up in the real estate market

A cautionary tale of the go-go '80s

Len and Patte Purcell in 1989

Patricia Purcell walked unsteadily into Courtroom 6 in San Diego's federal courthouse. Her face sagged from too little sleep, no makeup, and tension. Supporters in the courtroom for her sentencing hearing did a double-take. The indomitable Patte they knew was not tentative, had not let nearly four months as a federal inmate at the Metropolitan Correctional Center affect her grooming — hair, nails, and makeup were a priority.

Patte and Len Purcell

But Patte had spent the night before this hearing in the hole, her punishment for refusing to submit to the requisite strip-search from one particular guard, whom Patte said was a lesbian. This morning Patte was without a shower, clean underwear, makeup, and was functioning only on nerves.

As the hearing progressed, Patte regained her voice and her unswerving confidence. She repeated her story for the court — as she had at trial and countless times since in pleadings, motions, and writs — that she and her husband had done nothing wrong. Events and institutions had conspired to land them in prison, penniless.

Patte and Len Purcell were sentenced to 37 months in federal prison for getting caught up — and caught in — the overheated Southern California real estate market of the late 1980s.

The specific real estate in question — a $ 1 million home in La Jolla and two condominiums in La Jolla and one in Del Mar—were years ago defaulted upon, returned to the lenders, and resold. The Purcells filed bankruptcy and left San Diego, homeless, in 1992, with only their “beater” 1973 El Dorado, two cats, and two lovebirds.

The Purcells’ crimes, as decided by a federal jury in September of 1994, involved misleading statements on bank loan applications and trying to use lenders’ money to cash in on the real estate boom, since they had none of their own. As they layered 13 different loans involving 40 deeds of trust in 19 months, from 1988 to 1990, each “paper profit” found its way into their informal and oft-changing statements of income or assets.

Was it wrong? Yes, according to the law, because the loan documents they signed clearly stated that misrepresentations that would influence a bank are federal crimes. But, as pointed out after the trial by Alan Nevin, an expert witness, “That also means half of the population of Southern California should be in jail, too.”

Leonard, 50, and Patte, 42, who rarely spent hours apart in their 19 years of marriage, now face being separated by prison bars, in different cities, for the next three-plus years. “If I have to be away from my husband — that’s the hardest part — I will leave it in God’s hands. I am not capable of fighting this entire system by myself,” Patte said a few days after sentencing. “Whatever happens to me will be part of God’s plan.”

A parallel story also unfolds about those late-’80s go-go years, when banks were throwing money at real estate buyers, as in the old “if-you-can-fog-a-mirror-here’s-a-million-dollars” joke. The currency of the day was the EZ-Qual, quick qualification, no-income-verification loan. Stratospheric real estate values were the collateral; income to service those loans was considered secondary.

Loan officers worked on commission and were under intense pressure to close as many loan deals as they could, damn the details. Few if any loans were checked for veracity, and loan officers could help borrowers navigate the red-flag land mines, often filling in portions of the loan forms themselves. No supporting documentation? There was a way around it. No income tax returns? No problem.

Appraisers were in short supply, and sometimes they merely drove past properties to come up with mind-numbing valuations. No one second-guessed them. It was a golden time. Lenders were so frenzied, they ignored policies and procedures and neglected the most basic of banking tenets: Only give them a loan if they can prove they don’t need it.

Leonard and Patte Purcell lived and worked in Omaha, Nebraska, most of their married life. Although neither had any formal education past the high school level, they were known as hard workers and had engaging personalities that made them both excellent salespeople. Patte was the eldest of six children, raised by solid, Roman Catholic parents with bedrock, Midwestern, middle class values. Pam Denfeld, one of Patte’s sisters, recounted a childhood memory of the three sisters rolling down their bobby sox and dancing around the living room like ballerinas.

Len was born and raised in Wahoo, Nebraska. After a hitch in the U.S. Army, he mostly worked in sales and photography. Len has two adult sons from a previous marriage, but he has had no contact with them in years.

Patte and Len met at an Omaha shopping center. “Hello, pretty lady” was his opening line. Friends and relatives describe their relationship as true soul mates. “They depend on one another totally,” said Denfeld. “You don’t find many men who support their wives the way Len supports Patte.”

“She is the stronger of the two. He loves her very much, and he is just lost without her,” said their friend George Brooks, publisher of La Jolla Scene.

The couple wound down Len’s photography business as they took on City Slickers, a 16-page neighborhood tabloid newspaper, in which some of Patte’s family members invested and worked. Over the next five years, they converted it into a slick, four-color, pre-formatted lifestyle magazine and franchised it to a number of markets across the country. As entrepreneurs, they said, they tended to plow most of the earnings back into the business. And, in the great entrepreneurial tradition, they tended to live out of that business as well, with most expenses being charged off to the firm.

City Slickers ran into financial troubles in 1986, having something to do with one of Patte’s siblings, who accepted bad checks into accounts receivable. When the family business died, the Purcells took on the debt and lost their Omaha home.

They decided to start over where it was warm, trading cornfields for palm trees. “I can still remember those early days when we lived in Pacific Beach,” Len recalled during one prison

interview. “It was a scrape coming up with the rent some months, but we did it.” They sold ads for small publications and did other odd jobs.

5405 Calumet, La Jolla

La Jolla acquaintances at the time agreed. The Purcells were as poor as church mice, absolutely crazy about one another, and determined — especially Patte — to make it big. “She really believed she needed to do something for her family,” said one acquaintance. “She has always had this vision and would work nonstop to accomplish it.”

They dabbled in one entrepreneurial project after another until Patte came up with one that had legs. She would acquire videotapes from couture designers’ runway shows, sell advertising around them, and broadcast them on cable television stations. She dubbed the program The Fashion Show. In 1988 it was airing with both investor and advertiser interest. One financial adviser’s projections stated that The Fashion Show could, if properly capitalized and cultivated, gross millions of dollars each month.

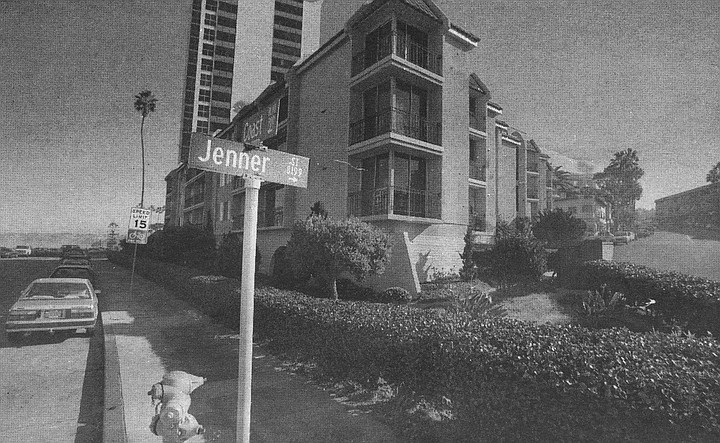

They knew they had to look for undervalued properties in prime locations, and found such a jewel in Unit 20,909 Coast Boulevard, in La Jolla.

Meanwhile, Len was trying to pull together a publication that depended on advertising sales and egos in the village of La Jolla. The maiden effort, Who's Who in La Jolla 1989, was published (it’s available for perusal in the La Jolla branch library), and Len made plans with his friend Brooks to expand the concept.

A chance remark by former banker John McCloskey, “You can make more money in California real estate sitting on your porch than you can working for the rest of your life,” burrowed its way into their psyches. The Purcells read, attended seminars, and bought a series of tapes from one of the many “strike-it-rich” financial gurus to make their mark in real estate.

From these courses, they knew they had to look for undervalued properties in prime locations and found such a jewel in Unit 20, 909 Coast Boulevard, in La Jolla. Because the seller agreed to take back a second trust deed for about $100,000, the Purcells qualified for a $200,000 loan on the $295,000 condominium in December 1988. Immediately they got to work refurbishing the place. Len’s talents included plumbing, electrical work, and a design sense, and Patte loved to paint. For about $20,000, doing all of the work themselves, they upgraded the unit, and by March 1989 they had taken out a third loan on the unit, for $60,000, to tide them over. Their $295,000 condo was now, only four months later, “worth” more than $363,000, at least according to the lenders who financed them.

One Sunday in the summer of 1989, Len filled out his prayer card at church, penciling in their wish to obtain another property like the first — undervalued, easily financed, and ready to be refurbished. Soon a church member buttonholed him and offered to be their partner, should the Purcells find the property of their prayers.

Quickly the Purcells identified another unit in their building with all of the requisites. On August 18, 1989, the Purcells and their churchgoing partner each purchased a 50 percent interest in 909 Coast Boulevard, Unit 2, for $105,000, with the seller taking back $40,000 in paper. Two months later, the Purcells refinanced their half for $160,000, and then another $140,000 was added to the mortgage when they bought out their partner. Voilá. Another $250,000 condominium now “worth” $300,000.

Life was good. Their friendship with publisher Brooks provided them entry to a number of society parties and homes. They breakfasted at The Cottage and pursued their businesses and real estate deals over lunch at the La Valencia Hotel.

That same August, 3000 miles away, the U.S. Congress labored to bring forth a law called the Financial Institutions Reform Recovery and Enforcement Act of 1989 (FIRREA). Congress felt depository institutions — especially savings and loan associations — were playing a bit fast and loose with their assets. So the clock was started for lenders to triple their capital reserves for construction loans, a major portion of asset bases for many of them. Some lenders took the message to heart earlier than others and started reining themselves in. FIRREA was the beginning of the end for the real estate boom and for nearly 800 financial institutions.

The recession took hold first in the East, and although a few signs made their way into the mainstream in the West — hiring slowed down, as classified want ads showed some softness in 1989’s fourth quarter, for example — most of the Golden State was oblivious to the pending downturn.

Indeed, the Purcells had no trouble refinancing their original condo (Unit 20). On an appraisal of more than $500,000, Home Fed anted up $393,000, and MJ Financial handed over a second mortgage of $62,000. Now, mid-November of 1989, less than one year since its purchase, that $295,000 condo was “worth” $455,000. In that loan document, the Purcells’ income was estimated at $15,000 a month and their assets at $870,000.

Yet only three weeks later, on December 6, 1989, on loan documents for the purchase of a third condo, the couple’s income was estimated as $150,000 a month, with other annual income of $250,000 and an unidentified asset worth $1 million. The purchase price on the Stratford Court, Del Mar, condo was $269,000, and two mortgages — backed up by the property’s value — totaled $299,000.

Then the Purcells found the house of their dreams and a tailor-made answer to their growing condo mortgage payments. The Calumet house was more than 5500 square feet of contemporary custom home, one block from the Pacific Ocean in La Jolla, with unobstructed views from any of its four patios. The sellers, a divorcing couple and some partners, were motivated, the month-old bank appraisal was $1.25 million, and a $1 million loan from American Savings Bank was a familiar EZ-Qual, no-income-verification, assumable one, just waiting for someone to walk into. A deal was struck in December 1989.

It took one month for Patte and Len to pull together all the pieces of the transaction, and they enlisted the help of Patte’s brother, Greg Albracht, as an accommodator — legal jargon for a disinterested middleman.

Recorded on January 24, 1990, through two separate escrows, the Calumet estate was “purchased” for $950,000 by Albracht and then “sold” to the Purcells in trade for the majority of the condominium assets for consideration of $1.25 million. The $1 million American Savings loan was the centerpiece of this transaction, the proceeds of which went to the original sellers, to an Omaha bank to satisfy the final City Slickers debt, and into the partner escrow. On the loan document, annual income for the Purcells was estimated at $774,000, assets at $1 million, and $50,000 was listed as cash in a checking account.

909 Coast Boulevard, La Jolla

The recession finally hit. In April of 1990, a major investor pulled out of The Fashion Show, and Patte’s financial adviser warned her not to use his earlier millions-a-month projections unless that capital was replaced. As expert at sales as they were, the Purcells were getting more noes than yeses on their ventures.

The second Calumet mortgage payment — a hefty $7829 a month — bounced, and no further payments were made, even though they lived there another 20 months. They were also behind on their car lease payments, three condo association fees, credit cards, and other bills.

The only way out was to sell their lovely Calumet, which went on the market at $ 1.95 million. But in the intervening six months, American Savings Bank had sobered to the reality of the real estate market and refused all buyers who wanted to assume its $1 million loan. The Calumet estate, the bank now said, was worth only the land value of $600,000. If some other lender wanted to get on the hook, that was fine with American Savings, but the Purcells found that lenders had pulled in their horns on the “jumbo loans,” and the property languished on the market.

Even so, in June 1990, already three months in arrears on their dream home, the Purcells found a lender to refinance the Del Mar condominium for $300,000, another loan of the EZ-Qual variety. Documents estimated their income at $60,000 a month, and the Calumet property was listed as an asset worth $1.8 million.

Five months later, in November of 1990, the Purcells filed Chapter 11 bankruptcy to give themselves more time to sell the house and condos. In that filing, they listed $1.7 million in claims against them, which ran the gamut from real estate loans to 21 different credit cards, property taxes to pool services. A diamond ring ostensibly worth $25,000 had been pawned for $3700. Their bankruptcy petition also stated “debtors have lived off the proceeds of sales of their properties since December 1989.”

In July 1991, U.S. Bankruptcy Court Judge Peter Bowie agreed to let American Savings take back Calumet in a trustee’s sale and judged the property to be worth $ 1.25 million and the debt against it $1.15 million. In October of 1991, American Savings reacquired the property for $829,000.

On November 15, 1991, Patte and Len Purcell closed the door to the Calumet house, handed over the keys to a trusted friend to deliver, and returned to Omaha to lick their wounds. Patte’s mother was doing poorly after the death of her husband. Then she, too, died. “I didn’t work, I didn’t do much of anything then,” Patte recalled. “I was completely burned out from all that had happened in San Diego and the death of my parents. What kept going around in my head was, ‘I failed, I failed, I failed.’ ”

By all rights, this story should end here, with two people who had nothing when they got to San Diego in 1986, leaving the same way five years later. But in April of 1992, the Purcells again heard from San Diego. American Savings, in its mop-up of the go-go years, had filed an adversary proceeding against the couple, stating the bank figured it was still out $358,525 and wanted the bankruptcy court to exclude this debt from bankruptcy protection. Furthermore, the bank stated, the financial information in the loan application was false, misrepresentative, and the bank had “reasonably relied on the Purcells’ statements,” or it wouldn’t have made the loan.

In July 1992, attorney Mark Moore wrote to American Savings, pointing out that it already had the house, the judge had determined the property value exceeded the debt by $90,000, and if they wanted to pursue it, Moore would immediately file for attorney’s fees and costs. American dropped the case. “An essential element of this, as I saw it, was, if there had been some loss to the bank, that’s one thing. If not, go away,” Moore explained in an interview. “Whatever the bank sold the property for was their business, not my clients’.”

As later explained by a non-involved banker, the American Savings filing was pro forma. “When the late 1980s finally got sifted out, all the jumbo lenders had to move into damage-control mode. The only excuse any of them could come up with for their lending behavior was, they were defrauded.” Hauled up short by new capital and lending regulations, savings and loans got religion and had ceased their former practice of “you go after the house or after the borrowers, but not both.”

While Patte and Len were eking out a living in Omaha and Colorado, the Bank Fraud Task Force in San Diego’s U.S. Attorney’s office was preparing for its cleanup. And of the hundreds of files that had made their way to the office, one of the Purcells’ percolated to the top.

Corey Smith, a young Department of Justice prosecutor loaned to the San Diego U.S. Attorney’s office, recalled that because of the dollar amount involved (in the $400,000 Home Federal loan to Patte’s brother, the accommodator, on Unit 2), his supervisor handed him the Albracht file, and “I was given the green light to look deeper,” he said.

What caught the government’s eye was a discrepancy between loan documents and escrow papers on the same transaction. Home Fed’s loan papers were made out for a $500,000 purchase, consisting of its $400,000 loan and a $100,000 cash down payment. However, escrow papers showed that there had been no cash down payment, but rather a 50 percent interest in the Del Mar condominium. Also, not one payment had been made on that Home Fed loan.

Smith had a standard registry of deeds review done on Albracht and found that the previous owners of Unit 2 had been the Purcells, who popped up on the scan as having executed 13 loans from December 1988 through June of 1990. “When we find that many loans and those large amounts of default, with few, if any payments made, we move ahead.”

As he dug into the loan files, Smith said he found “wildly different amounts on them.... Granted, property values are subject to change in the marketplace, but these were huge fluctuations. When you see that, it starts to look less like bad fortune at the hands of an unforgiving real estate market and more like a plan.”

The federal grand jury agreed. In September of 1993, a 14-count indictment was handed down against the Purcells and Greg Albracht, charging violations of a number of U.S. Code Title 18 sections regarding conspiracy, bank fraud, false statements, money laundering, and aiding and abetting.

Early in the morning of September 22, six FBI agents arrested Len and Patte at his brother’s home in Las Vegas. Dazed and unbelieving, they walked through the motions of arrest and arraignment and were released on their own recognizance. Federal defenders were assigned, and the legal wheels were set in motion. Their financial statement for the court as of October 4, 1993, listed income of $600 a month, about $700 in cash, and two old cars.

They returned to Las Vegas, trying to sort out what was happening to them. Their mantra was, “We have nothing, the banks have the houses. We did everything we were told to do. We used their appraisals. Why are they after us?” Then they happened onto Frank Ujalki, an active member of the state Citizenship movement, and in that movement found solace.

As explained by Ujalki, state Citizens believe that when our forefathers added the 13th and 14th Amendments to the U.S. Constitution, which abolished slavery, defined citizenship, and mandated against the abridgement of citizens’ rights, they ended up decreeing two different classes of citizens. The state Citizen interprets that to mean that there are two United States — one geographic and one corporate. The corporate entity, say state Citizens, refers only to ten square miles within Washington, D.C., was declared insolvent in 1933, and has since been under direct control of its creditors, the international banking families, which include the Rockefellers, Rothschilds, and Warburgs.

As such, the argument goes, these international bankers come to their domestic partners’ aid at will, turning on and off the supply of credit, and thus conspiring to create false economies. The recession of 1989 to ’92, they say, was just such an exercise by the “banksters.”

257 Stratford Court, Del Mar

This corporate United States, state Citizens assert, has no jurisdiction over citizens (or slaves) unless they allow it, through Social Security numbers, paying federal taxes, and other such methods. True state Citizens formally revoke all such contracts with the corporate United States.

By the time the Purcells were ready for trial, they had rejected all settlement offers, which in one instance allegedly amounted to as little as six months in a halfway house for a guilty plea. They had renounced their citizenship in the corporate U.S., decided to defend themselves against the charges, and fired their federal defenders. Their opening salvo in July of 1994 was the claim that the federal court lacked jurisdiction “over free citizens of Nevada state.” U.S. District Court Judge Judith Keep — who was to hear that argument countless times in the remaining months of 1994 — ruled that she indeed had jurisdiction and was backed up when the U.S. Court of Appeals also rejected the Purcells’ claim.

Early in the proceedings, the government dismissed all charges against Albracht, since he had filled out none of the loan documents in question, had acted as an accommodator to help his sister, and had profited from all of these machinations to the tune of $10 and change.

Judge Keep appointed standby counsel for the Purcells, Elizabeth Barranco for Patte, and Charles Adair for Len. These experienced defense attorneys had to wear two hats — as advisers to the Purcells, when asked, and as protectors of the court, to avert a potential mistrial at the hands of the inexperienced defendants representing themselves. Both attorneys were fired, rehired, and again fired by their clients through a rocky six-month relationship.

As their own counsel, the Purcells often stumbled over details of court procedure. Their defense was an expanded version of their mantra, and it was an emotional couple of weeks. Len broke down at times. Patte became more and more strident as she was thwarted from presenting some elements of her case. She was a blur of activity, even writing letters to U.S. Attorney General Janet Reno accusing Judge Keep of being a “satanic force.”

When the standby counsel finally took the floor, their only remaining option was to try to make the government prove the Purcells’ income estimates were false. The prosecution, with its 334 pieces of evidence and 33 witnesses, prevailed.

On September 29,1994, the jury found the Purcells guilty of conspiracy to make false statements and of making false statements. They were remanded into MCC custody that day; Judge Keep said she regarded them flight risks, since they disputed the jurisdiction of the U.S. court. A regular courthouse observer noted that immediate federal custody “is the defendant’s punishment for going to trial.”

After the verdict, Adair and Barranco interviewed a couple of the jurors, who told them they liked the Purcells, felt sorry for them, and wished they could have acquitted them of all charges, but the way the law was written and cited to them, they had no choice.

The judge’s jury instructions were made “completely according to law,” said Barranco after trial. “Do I think they were fair? No, I don’t. I just don’t think people should be convicted of a crime for making a statement, when the banks didn’t even bother to demand verification. But what I think and what is legal are two different things.”

Even prosecutor Smith cautiously agreed when pushed on the point of the lender’s responsibility to its depositors and shareholders to exercise some care before handing out money. “From a good business standpoint, it would be prudent to check out what people tell you before granting a loan. But banks rely, in great part, on the fact that people are not lying to them, because federal law backs them up.

“There’s no doubt that the Purcells were very articulate, motivated, hard-working individuals. But the problem was, they would tell stories to get what they wanted and where they wanted to go,” Smith added. “One of the things that sticks out about this case was their propensity to lie and lie over and over again.”

“This whole thing was a fluke,” said expert witness Nevin. “Somebody was on a glory path with this one. The thought that this was brought to trial among the hundreds of cases from those days of profligate lending was absolutely stunning to me.”

“Patte and Len never laid awake at night plotting a crime,” said Barranco. “They’re just not made that way. But Patte is so optimistic, she doesn’t accept defeat, and is so strong...sometimes people like that believe the law can be shaped into their way of thinking. It can’t. And despite what you see on television, the system is not pro-defendant and never has been.”

Added Adair, “On the human side, this is very depressing, frankly, to see two people so devoted to one another, who didn’t start out to commit any criminal acts, being subjected to all of this. When Len would break down, it tended to shock me out of my defense lawyer complacency with the system and really see how this affects people’s lives in a major way.”

Sentencing complete, the Purcells await the Bureau of Prisons’ decision as to their next federal residences, where, with good behavior, about 5 months could be knocked off their 37-month sentences. Their last days at MCC are not easy ones, in that some of their privileges, including their pro per cocounsel visits, have been revoked. Although technically fired, Adair continues to spend time to set their appeals in motion and says he feels they have a shot. Patte is still writing letters, once again telling her story to judges and other officials above Judge Keep’s rank.

“No crime would have been committed if our businesses hadn’t failed,” Patte insisted at her sentencing hearing. “No crime would have been committed if the bank had allowed us to sell our home. We did not make up appraisals or values. How could we? You know what a fighter I am, Judge Keep. Do you think I woke up one day and decided to go bankrupt? To give up everything we had worked so hard to accomplish? Of course I fought tooth and nail to keep everything I had.”

Here's something you might be interested in.

Patte and Len Purcell – 37 months in federal prison for getting caught up in the real estate market

A cautionary tale of the go-go '80s

Patte and Len Purcell – 37 months in federal prison for getting caught up in the real estate market

A cautionary tale of the go-go '80s

Len and Patte Purcell in 1989

Patricia Purcell walked unsteadily into Courtroom 6 in San Diego's federal courthouse. Her face sagged from too little sleep, no makeup, and tension. Supporters in the courtroom for her sentencing hearing did a double-take. The indomitable Patte they knew was not tentative, had not let nearly four months as a federal inmate at the Metropolitan Correctional Center affect her grooming — hair, nails, and makeup were a priority.

Patte and Len Purcell

But Patte had spent the night before this hearing in the hole, her punishment for refusing to submit to the requisite strip-search from one particular guard, whom Patte said was a lesbian. This morning Patte was without a shower, clean underwear, makeup, and was functioning only on nerves.

As the hearing progressed, Patte regained her voice and her unswerving confidence. She repeated her story for the court — as she had at trial and countless times since in pleadings, motions, and writs — that she and her husband had done nothing wrong. Events and institutions had conspired to land them in prison, penniless.

Patte and Len Purcell were sentenced to 37 months in federal prison for getting caught up — and caught in — the overheated Southern California real estate market of the late 1980s.

The specific real estate in question — a $ 1 million home in La Jolla and two condominiums in La Jolla and one in Del Mar—were years ago defaulted upon, returned to the lenders, and resold. The Purcells filed bankruptcy and left San Diego, homeless, in 1992, with only their “beater” 1973 El Dorado, two cats, and two lovebirds.

The Purcells’ crimes, as decided by a federal jury in September of 1994, involved misleading statements on bank loan applications and trying to use lenders’ money to cash in on the real estate boom, since they had none of their own. As they layered 13 different loans involving 40 deeds of trust in 19 months, from 1988 to 1990, each “paper profit” found its way into their informal and oft-changing statements of income or assets.

Was it wrong? Yes, according to the law, because the loan documents they signed clearly stated that misrepresentations that would influence a bank are federal crimes. But, as pointed out after the trial by Alan Nevin, an expert witness, “That also means half of the population of Southern California should be in jail, too.”

Leonard, 50, and Patte, 42, who rarely spent hours apart in their 19 years of marriage, now face being separated by prison bars, in different cities, for the next three-plus years. “If I have to be away from my husband — that’s the hardest part — I will leave it in God’s hands. I am not capable of fighting this entire system by myself,” Patte said a few days after sentencing. “Whatever happens to me will be part of God’s plan.”

A parallel story also unfolds about those late-’80s go-go years, when banks were throwing money at real estate buyers, as in the old “if-you-can-fog-a-mirror-here’s-a-million-dollars” joke. The currency of the day was the EZ-Qual, quick qualification, no-income-verification loan. Stratospheric real estate values were the collateral; income to service those loans was considered secondary.

Loan officers worked on commission and were under intense pressure to close as many loan deals as they could, damn the details. Few if any loans were checked for veracity, and loan officers could help borrowers navigate the red-flag land mines, often filling in portions of the loan forms themselves. No supporting documentation? There was a way around it. No income tax returns? No problem.

Appraisers were in short supply, and sometimes they merely drove past properties to come up with mind-numbing valuations. No one second-guessed them. It was a golden time. Lenders were so frenzied, they ignored policies and procedures and neglected the most basic of banking tenets: Only give them a loan if they can prove they don’t need it.

Leonard and Patte Purcell lived and worked in Omaha, Nebraska, most of their married life. Although neither had any formal education past the high school level, they were known as hard workers and had engaging personalities that made them both excellent salespeople. Patte was the eldest of six children, raised by solid, Roman Catholic parents with bedrock, Midwestern, middle class values. Pam Denfeld, one of Patte’s sisters, recounted a childhood memory of the three sisters rolling down their bobby sox and dancing around the living room like ballerinas.

Len was born and raised in Wahoo, Nebraska. After a hitch in the U.S. Army, he mostly worked in sales and photography. Len has two adult sons from a previous marriage, but he has had no contact with them in years.

Patte and Len met at an Omaha shopping center. “Hello, pretty lady” was his opening line. Friends and relatives describe their relationship as true soul mates. “They depend on one another totally,” said Denfeld. “You don’t find many men who support their wives the way Len supports Patte.”

“She is the stronger of the two. He loves her very much, and he is just lost without her,” said their friend George Brooks, publisher of La Jolla Scene.

The couple wound down Len’s photography business as they took on City Slickers, a 16-page neighborhood tabloid newspaper, in which some of Patte’s family members invested and worked. Over the next five years, they converted it into a slick, four-color, pre-formatted lifestyle magazine and franchised it to a number of markets across the country. As entrepreneurs, they said, they tended to plow most of the earnings back into the business. And, in the great entrepreneurial tradition, they tended to live out of that business as well, with most expenses being charged off to the firm.

City Slickers ran into financial troubles in 1986, having something to do with one of Patte’s siblings, who accepted bad checks into accounts receivable. When the family business died, the Purcells took on the debt and lost their Omaha home.

They decided to start over where it was warm, trading cornfields for palm trees. “I can still remember those early days when we lived in Pacific Beach,” Len recalled during one prison

interview. “It was a scrape coming up with the rent some months, but we did it.” They sold ads for small publications and did other odd jobs.

5405 Calumet, La Jolla

La Jolla acquaintances at the time agreed. The Purcells were as poor as church mice, absolutely crazy about one another, and determined — especially Patte — to make it big. “She really believed she needed to do something for her family,” said one acquaintance. “She has always had this vision and would work nonstop to accomplish it.”

They dabbled in one entrepreneurial project after another until Patte came up with one that had legs. She would acquire videotapes from couture designers’ runway shows, sell advertising around them, and broadcast them on cable television stations. She dubbed the program The Fashion Show. In 1988 it was airing with both investor and advertiser interest. One financial adviser’s projections stated that The Fashion Show could, if properly capitalized and cultivated, gross millions of dollars each month.

They knew they had to look for undervalued properties in prime locations, and found such a jewel in Unit 20,909 Coast Boulevard, in La Jolla.

Meanwhile, Len was trying to pull together a publication that depended on advertising sales and egos in the village of La Jolla. The maiden effort, Who's Who in La Jolla 1989, was published (it’s available for perusal in the La Jolla branch library), and Len made plans with his friend Brooks to expand the concept.

A chance remark by former banker John McCloskey, “You can make more money in California real estate sitting on your porch than you can working for the rest of your life,” burrowed its way into their psyches. The Purcells read, attended seminars, and bought a series of tapes from one of the many “strike-it-rich” financial gurus to make their mark in real estate.

From these courses, they knew they had to look for undervalued properties in prime locations and found such a jewel in Unit 20, 909 Coast Boulevard, in La Jolla. Because the seller agreed to take back a second trust deed for about $100,000, the Purcells qualified for a $200,000 loan on the $295,000 condominium in December 1988. Immediately they got to work refurbishing the place. Len’s talents included plumbing, electrical work, and a design sense, and Patte loved to paint. For about $20,000, doing all of the work themselves, they upgraded the unit, and by March 1989 they had taken out a third loan on the unit, for $60,000, to tide them over. Their $295,000 condo was now, only four months later, “worth” more than $363,000, at least according to the lenders who financed them.

One Sunday in the summer of 1989, Len filled out his prayer card at church, penciling in their wish to obtain another property like the first — undervalued, easily financed, and ready to be refurbished. Soon a church member buttonholed him and offered to be their partner, should the Purcells find the property of their prayers.

Quickly the Purcells identified another unit in their building with all of the requisites. On August 18, 1989, the Purcells and their churchgoing partner each purchased a 50 percent interest in 909 Coast Boulevard, Unit 2, for $105,000, with the seller taking back $40,000 in paper. Two months later, the Purcells refinanced their half for $160,000, and then another $140,000 was added to the mortgage when they bought out their partner. Voilá. Another $250,000 condominium now “worth” $300,000.

Life was good. Their friendship with publisher Brooks provided them entry to a number of society parties and homes. They breakfasted at The Cottage and pursued their businesses and real estate deals over lunch at the La Valencia Hotel.

That same August, 3000 miles away, the U.S. Congress labored to bring forth a law called the Financial Institutions Reform Recovery and Enforcement Act of 1989 (FIRREA). Congress felt depository institutions — especially savings and loan associations — were playing a bit fast and loose with their assets. So the clock was started for lenders to triple their capital reserves for construction loans, a major portion of asset bases for many of them. Some lenders took the message to heart earlier than others and started reining themselves in. FIRREA was the beginning of the end for the real estate boom and for nearly 800 financial institutions.

The recession took hold first in the East, and although a few signs made their way into the mainstream in the West — hiring slowed down, as classified want ads showed some softness in 1989’s fourth quarter, for example — most of the Golden State was oblivious to the pending downturn.

Indeed, the Purcells had no trouble refinancing their original condo (Unit 20). On an appraisal of more than $500,000, Home Fed anted up $393,000, and MJ Financial handed over a second mortgage of $62,000. Now, mid-November of 1989, less than one year since its purchase, that $295,000 condo was “worth” $455,000. In that loan document, the Purcells’ income was estimated at $15,000 a month and their assets at $870,000.

Yet only three weeks later, on December 6, 1989, on loan documents for the purchase of a third condo, the couple’s income was estimated as $150,000 a month, with other annual income of $250,000 and an unidentified asset worth $1 million. The purchase price on the Stratford Court, Del Mar, condo was $269,000, and two mortgages — backed up by the property’s value — totaled $299,000.

Then the Purcells found the house of their dreams and a tailor-made answer to their growing condo mortgage payments. The Calumet house was more than 5500 square feet of contemporary custom home, one block from the Pacific Ocean in La Jolla, with unobstructed views from any of its four patios. The sellers, a divorcing couple and some partners, were motivated, the month-old bank appraisal was $1.25 million, and a $1 million loan from American Savings Bank was a familiar EZ-Qual, no-income-verification, assumable one, just waiting for someone to walk into. A deal was struck in December 1989.

It took one month for Patte and Len to pull together all the pieces of the transaction, and they enlisted the help of Patte’s brother, Greg Albracht, as an accommodator — legal jargon for a disinterested middleman.

Recorded on January 24, 1990, through two separate escrows, the Calumet estate was “purchased” for $950,000 by Albracht and then “sold” to the Purcells in trade for the majority of the condominium assets for consideration of $1.25 million. The $1 million American Savings loan was the centerpiece of this transaction, the proceeds of which went to the original sellers, to an Omaha bank to satisfy the final City Slickers debt, and into the partner escrow. On the loan document, annual income for the Purcells was estimated at $774,000, assets at $1 million, and $50,000 was listed as cash in a checking account.

909 Coast Boulevard, La Jolla

The recession finally hit. In April of 1990, a major investor pulled out of The Fashion Show, and Patte’s financial adviser warned her not to use his earlier millions-a-month projections unless that capital was replaced. As expert at sales as they were, the Purcells were getting more noes than yeses on their ventures.

The second Calumet mortgage payment — a hefty $7829 a month — bounced, and no further payments were made, even though they lived there another 20 months. They were also behind on their car lease payments, three condo association fees, credit cards, and other bills.

The only way out was to sell their lovely Calumet, which went on the market at $ 1.95 million. But in the intervening six months, American Savings Bank had sobered to the reality of the real estate market and refused all buyers who wanted to assume its $1 million loan. The Calumet estate, the bank now said, was worth only the land value of $600,000. If some other lender wanted to get on the hook, that was fine with American Savings, but the Purcells found that lenders had pulled in their horns on the “jumbo loans,” and the property languished on the market.

Even so, in June 1990, already three months in arrears on their dream home, the Purcells found a lender to refinance the Del Mar condominium for $300,000, another loan of the EZ-Qual variety. Documents estimated their income at $60,000 a month, and the Calumet property was listed as an asset worth $1.8 million.

Five months later, in November of 1990, the Purcells filed Chapter 11 bankruptcy to give themselves more time to sell the house and condos. In that filing, they listed $1.7 million in claims against them, which ran the gamut from real estate loans to 21 different credit cards, property taxes to pool services. A diamond ring ostensibly worth $25,000 had been pawned for $3700. Their bankruptcy petition also stated “debtors have lived off the proceeds of sales of their properties since December 1989.”

In July 1991, U.S. Bankruptcy Court Judge Peter Bowie agreed to let American Savings take back Calumet in a trustee’s sale and judged the property to be worth $ 1.25 million and the debt against it $1.15 million. In October of 1991, American Savings reacquired the property for $829,000.

On November 15, 1991, Patte and Len Purcell closed the door to the Calumet house, handed over the keys to a trusted friend to deliver, and returned to Omaha to lick their wounds. Patte’s mother was doing poorly after the death of her husband. Then she, too, died. “I didn’t work, I didn’t do much of anything then,” Patte recalled. “I was completely burned out from all that had happened in San Diego and the death of my parents. What kept going around in my head was, ‘I failed, I failed, I failed.’ ”

By all rights, this story should end here, with two people who had nothing when they got to San Diego in 1986, leaving the same way five years later. But in April of 1992, the Purcells again heard from San Diego. American Savings, in its mop-up of the go-go years, had filed an adversary proceeding against the couple, stating the bank figured it was still out $358,525 and wanted the bankruptcy court to exclude this debt from bankruptcy protection. Furthermore, the bank stated, the financial information in the loan application was false, misrepresentative, and the bank had “reasonably relied on the Purcells’ statements,” or it wouldn’t have made the loan.

In July 1992, attorney Mark Moore wrote to American Savings, pointing out that it already had the house, the judge had determined the property value exceeded the debt by $90,000, and if they wanted to pursue it, Moore would immediately file for attorney’s fees and costs. American dropped the case. “An essential element of this, as I saw it, was, if there had been some loss to the bank, that’s one thing. If not, go away,” Moore explained in an interview. “Whatever the bank sold the property for was their business, not my clients’.”

As later explained by a non-involved banker, the American Savings filing was pro forma. “When the late 1980s finally got sifted out, all the jumbo lenders had to move into damage-control mode. The only excuse any of them could come up with for their lending behavior was, they were defrauded.” Hauled up short by new capital and lending regulations, savings and loans got religion and had ceased their former practice of “you go after the house or after the borrowers, but not both.”

While Patte and Len were eking out a living in Omaha and Colorado, the Bank Fraud Task Force in San Diego’s U.S. Attorney’s office was preparing for its cleanup. And of the hundreds of files that had made their way to the office, one of the Purcells’ percolated to the top.

Corey Smith, a young Department of Justice prosecutor loaned to the San Diego U.S. Attorney’s office, recalled that because of the dollar amount involved (in the $400,000 Home Federal loan to Patte’s brother, the accommodator, on Unit 2), his supervisor handed him the Albracht file, and “I was given the green light to look deeper,” he said.

What caught the government’s eye was a discrepancy between loan documents and escrow papers on the same transaction. Home Fed’s loan papers were made out for a $500,000 purchase, consisting of its $400,000 loan and a $100,000 cash down payment. However, escrow papers showed that there had been no cash down payment, but rather a 50 percent interest in the Del Mar condominium. Also, not one payment had been made on that Home Fed loan.

Smith had a standard registry of deeds review done on Albracht and found that the previous owners of Unit 2 had been the Purcells, who popped up on the scan as having executed 13 loans from December 1988 through June of 1990. “When we find that many loans and those large amounts of default, with few, if any payments made, we move ahead.”

As he dug into the loan files, Smith said he found “wildly different amounts on them.... Granted, property values are subject to change in the marketplace, but these were huge fluctuations. When you see that, it starts to look less like bad fortune at the hands of an unforgiving real estate market and more like a plan.”

The federal grand jury agreed. In September of 1993, a 14-count indictment was handed down against the Purcells and Greg Albracht, charging violations of a number of U.S. Code Title 18 sections regarding conspiracy, bank fraud, false statements, money laundering, and aiding and abetting.

Early in the morning of September 22, six FBI agents arrested Len and Patte at his brother’s home in Las Vegas. Dazed and unbelieving, they walked through the motions of arrest and arraignment and were released on their own recognizance. Federal defenders were assigned, and the legal wheels were set in motion. Their financial statement for the court as of October 4, 1993, listed income of $600 a month, about $700 in cash, and two old cars.

They returned to Las Vegas, trying to sort out what was happening to them. Their mantra was, “We have nothing, the banks have the houses. We did everything we were told to do. We used their appraisals. Why are they after us?” Then they happened onto Frank Ujalki, an active member of the state Citizenship movement, and in that movement found solace.

As explained by Ujalki, state Citizens believe that when our forefathers added the 13th and 14th Amendments to the U.S. Constitution, which abolished slavery, defined citizenship, and mandated against the abridgement of citizens’ rights, they ended up decreeing two different classes of citizens. The state Citizen interprets that to mean that there are two United States — one geographic and one corporate. The corporate entity, say state Citizens, refers only to ten square miles within Washington, D.C., was declared insolvent in 1933, and has since been under direct control of its creditors, the international banking families, which include the Rockefellers, Rothschilds, and Warburgs.

As such, the argument goes, these international bankers come to their domestic partners’ aid at will, turning on and off the supply of credit, and thus conspiring to create false economies. The recession of 1989 to ’92, they say, was just such an exercise by the “banksters.”

257 Stratford Court, Del Mar

This corporate United States, state Citizens assert, has no jurisdiction over citizens (or slaves) unless they allow it, through Social Security numbers, paying federal taxes, and other such methods. True state Citizens formally revoke all such contracts with the corporate United States.

By the time the Purcells were ready for trial, they had rejected all settlement offers, which in one instance allegedly amounted to as little as six months in a halfway house for a guilty plea. They had renounced their citizenship in the corporate U.S., decided to defend themselves against the charges, and fired their federal defenders. Their opening salvo in July of 1994 was the claim that the federal court lacked jurisdiction “over free citizens of Nevada state.” U.S. District Court Judge Judith Keep — who was to hear that argument countless times in the remaining months of 1994 — ruled that she indeed had jurisdiction and was backed up when the U.S. Court of Appeals also rejected the Purcells’ claim.

Early in the proceedings, the government dismissed all charges against Albracht, since he had filled out none of the loan documents in question, had acted as an accommodator to help his sister, and had profited from all of these machinations to the tune of $10 and change.

Judge Keep appointed standby counsel for the Purcells, Elizabeth Barranco for Patte, and Charles Adair for Len. These experienced defense attorneys had to wear two hats — as advisers to the Purcells, when asked, and as protectors of the court, to avert a potential mistrial at the hands of the inexperienced defendants representing themselves. Both attorneys were fired, rehired, and again fired by their clients through a rocky six-month relationship.

As their own counsel, the Purcells often stumbled over details of court procedure. Their defense was an expanded version of their mantra, and it was an emotional couple of weeks. Len broke down at times. Patte became more and more strident as she was thwarted from presenting some elements of her case. She was a blur of activity, even writing letters to U.S. Attorney General Janet Reno accusing Judge Keep of being a “satanic force.”

When the standby counsel finally took the floor, their only remaining option was to try to make the government prove the Purcells’ income estimates were false. The prosecution, with its 334 pieces of evidence and 33 witnesses, prevailed.

On September 29,1994, the jury found the Purcells guilty of conspiracy to make false statements and of making false statements. They were remanded into MCC custody that day; Judge Keep said she regarded them flight risks, since they disputed the jurisdiction of the U.S. court. A regular courthouse observer noted that immediate federal custody “is the defendant’s punishment for going to trial.”

After the verdict, Adair and Barranco interviewed a couple of the jurors, who told them they liked the Purcells, felt sorry for them, and wished they could have acquitted them of all charges, but the way the law was written and cited to them, they had no choice.

The judge’s jury instructions were made “completely according to law,” said Barranco after trial. “Do I think they were fair? No, I don’t. I just don’t think people should be convicted of a crime for making a statement, when the banks didn’t even bother to demand verification. But what I think and what is legal are two different things.”

Even prosecutor Smith cautiously agreed when pushed on the point of the lender’s responsibility to its depositors and shareholders to exercise some care before handing out money. “From a good business standpoint, it would be prudent to check out what people tell you before granting a loan. But banks rely, in great part, on the fact that people are not lying to them, because federal law backs them up.

“There’s no doubt that the Purcells were very articulate, motivated, hard-working individuals. But the problem was, they would tell stories to get what they wanted and where they wanted to go,” Smith added. “One of the things that sticks out about this case was their propensity to lie and lie over and over again.”

“This whole thing was a fluke,” said expert witness Nevin. “Somebody was on a glory path with this one. The thought that this was brought to trial among the hundreds of cases from those days of profligate lending was absolutely stunning to me.”

“Patte and Len never laid awake at night plotting a crime,” said Barranco. “They’re just not made that way. But Patte is so optimistic, she doesn’t accept defeat, and is so strong...sometimes people like that believe the law can be shaped into their way of thinking. It can’t. And despite what you see on television, the system is not pro-defendant and never has been.”

Added Adair, “On the human side, this is very depressing, frankly, to see two people so devoted to one another, who didn’t start out to commit any criminal acts, being subjected to all of this. When Len would break down, it tended to shock me out of my defense lawyer complacency with the system and really see how this affects people’s lives in a major way.”

Sentencing complete, the Purcells await the Bureau of Prisons’ decision as to their next federal residences, where, with good behavior, about 5 months could be knocked off their 37-month sentences. Their last days at MCC are not easy ones, in that some of their privileges, including their pro per cocounsel visits, have been revoked. Although technically fired, Adair continues to spend time to set their appeals in motion and says he feels they have a shot. Patte is still writing letters, once again telling her story to judges and other officials above Judge Keep’s rank.

“No crime would have been committed if our businesses hadn’t failed,” Patte insisted at her sentencing hearing. “No crime would have been committed if the bank had allowed us to sell our home. We did not make up appraisals or values. How could we? You know what a fighter I am, Judge Keep. Do you think I woke up one day and decided to go bankrupt? To give up everything we had worked so hard to accomplish? Of course I fought tooth and nail to keep everything I had.”

Comments