{kind=link}

Here's something you might be interested in.

Ask a Hipster — Advice you didn't know you needed

Big Screen — Movie commentary

Blurt — Music's inside track

Booze News — San Diego spirits

Classical Music — Immortal beauty

Classifieds — Free and easy

Cover Stories — Front-page features

Drinks All Around — Bartenders' drink recipes

Excerpts — Literary and spiritual excerpts

Feast! — Food & drink reviews

Feature Stories — Local news & stories

Fishing Report — What’s getting hooked from ship and shore

From the Archives — Spotlight on the past

Golden Dreams — Talk of the town

The Gonzo Report — Making the musical scene, or at least reporting from it

Letters — Our inbox

Movies@Home — Local movie buffs share favorites

Movie Reviews — Our critics' picks and pans

Musician Interviews — Up close with local artists

Neighborhood News from Stringers — Hyperlocal news

News Ticker — News & politics

Obermeyer — San Diego politics illustrated

Outdoors — Weekly changes in flora and fauna

Overheard in San Diego — Eavesdropping illustrated

Poetry — The old and the new

Reader Travel — Travel section built by travelers

Reading — The hunt for intellectuals

Roam-O-Rama — SoCal's best hiking/biking trails

San Diego Beer — Inside San Diego suds

SD on the QT — Almost factual news

Sheep and Goats — Places of worship

Special Issues — The best of

Street Style — San Diego streets have style

Surf Diego — Real stories from those braving the waves

Theater — On stage in San Diego this week

Tin Fork — Silver spoon alternative

Under the Radar — Matt Potter's undercover work

Unforgettable — Long-ago San Diego

Unreal Estate — San Diego's priciest pads

Your Week — Daily event picks

Local money men Robert Snigaroff, Neil Hokanson, Ross Starr bearish on future

Warning: “wheels come off” the economy within next three years

Where should you invest your money these days? A savings account? You will get almost nothing in interest returns. Bonds? Same problem. Stocks? They soared after the Great Recession ended in early 2009, but the economy has been weak. So even long-term bulls admit stocks are awfully expensive relative to their earnings and prospects. Real estate? Same problem: it’s expensive almost everywhere.

Neil Hokanson

“There is no cheap asset class,” says Neil Hokanson, principal of the Solana Beach office of Aspiriant, a money-management firm. “There is no low-hanging fruit. We just can’t stomach these low yields. It’s a horrible time in terms of finding something really attractive.” He tells his clients to be patient — invest slowly and keep a lot of money in low-yielding money market funds and the like (often called “cash”).

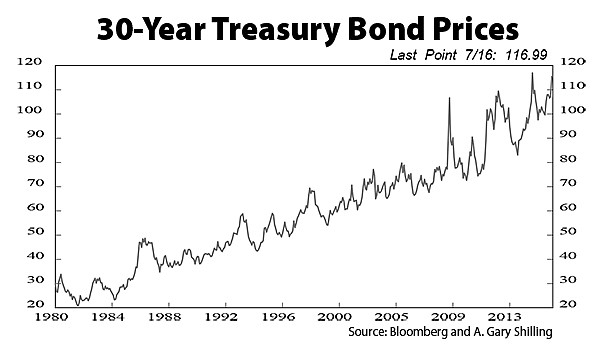

A. Gary Shilling

New Jersey–based economist A. Gary Shilling is widely followed these days because back in 1981 he predicted the “bond rally of a lifetime.” Many thought he was nuts. At the time, long-term bonds were yielding 15 percent. Recently the 30-year Treasury bond has been yielding around a mere 2.3 percent. Because bond prices rise as interest rates go down, Shilling is considered a prophet. Now, he feels United States rates will go even lower, so he is still buying 30-year Treasury bonds, but he admits that this strategy is not suitable for investors who need income.

30-Year-Treasury Bond Prices

Noting that banks in Europe and Japan are paying negative interest rates, he believes rates in the United States could go lower from current levels, although he is not ready to call negative interest rates in the U.S., since negative rates are not boosting economies that try them overseas. “Chronic deflation [prices declining] is increasingly likely,” he says. He would bet that American stocks will drop (a process called “shorting”) and would bet that oil will go even further down from its current level, perhaps as low as $10 to $20 a barrel, as other commodities tumble, too.

So, except for 30-year Treasury bonds, he basically agrees with Hokanson: no potential investment is a sure thing these days. Hokanson disagrees with Shilling on bonds: “After inflation and after taxes, the returns are negative,” he says.

Robert Snigaroff, Mike Stolper, and Neil Hokanson

Robert Snigaroff, president of San Diego’s Denali Advisors, says those claiming that stocks are too expensive are wrong. “Stocks are not outrageously priced, given the low interest rates,” he says. With bonds and savings accounts paying such puny returns, stock+s may be the answer. Money from around the world has been poured into utilities and high-yielding, blue-chip telecoms, such as AT&T and Verizon. Snigaroff, however, is not so bullish on utilities and telecoms: too much money has already been poured into them. Denali doesn’t go fishing for bonds, but Snigaroff thinks it is possible that Shilling may be right: they can rise further.

Ross Starr

Ross Starr, professor of economics at the University of California San Diego, warns of risks in Shilling’s strategy. “Since interest rates are at historic lows, the best guess is that rates will go up within a decade, and when that happens, the market value of existing bonds goes down, so for a conservative investor what looks like a safe bet, the 30-year Treasury bond, looks risky if the investor cashes out before the bond matures. However, it is safe if you don’t cash out.”

Starr says the “really safe” investment is inflation-protected Treasury bonds, called TIPS. “They are also safe in the unlikely event of persistent deflation.” (However, others point out that TIPS can produce tax headaches in some instances, and you can lose if you sell before the bond matures.)

Although he thinks interest rates could go up, he says tax-free California municipal bonds can be attractive. Also, “a portfolio of junk bonds [low-quality, high-yielding bonds] could provide handsome returns.” And what about Shilling’s strategy of buying long-term Treasury bonds? Starr thinks they are “in a bit of a bubble.”

Starr says stocks compared to U.S. Treasury paper are not overpriced, but compared with historic statistical measures they are overpriced. “There is no return without risk,” says Starr. “The conventional portfolio for an investor with a long horizon is an even mix of common stocks and fixed income [bonds].”

Carlsbad’s James Welsh writes a publication, Macro Tides, as well as a weekly technical market/economic review. Today, investors “are assuming more risk than the potential reward” merits, says Welsh. “Nothing looks that good.” Interest rates in the United States can’t go down much more: “We’re getting close to the end of the road” on bonds.

Stocks don’t look so hot, either. The U.S. stock market “is the third-most expensive in the last 100 years,” he says. Sobering, that. Indeed, “In the next month or two, the market will pull back 3 to 7 percent,” he says. Of course, that would be what’s called a “correction.” In bear markets, stocks go down 20 percent or more. The bear visits every 3.4 years, and the average decline in the last 25 bears, dating to 1929, is 35.43 percent. That means for the average investor, a dollar in stocks turns into 64.6 cents. But bull markets arise out of bears, and over time, stock investments have been as good as anything, but you have to have a strong stomach for the roller-coaster rides.

Welsh thinks valuations for the stocks that have done best in this market, telecoms and utilities, are on the high side. Generally, he would wait until the correction takes its bite before jumping back in. “It’s time for a breather,” says Welsh.

He blames the negative interest-rate policies in Europe and Japan for much of the current problems. Negative rates caused the market valuation of European banks to plummet. Those banks are in trouble: “There is $1 trillion of nonperforming loans throughout the European banking system, and one-third of that is in Italy,” which is really in sick bay. The negative interest rates have not helped economies and have caused people to lose confidence in central banks.

Demographics are not positive. The fertility rate has fallen from 2.12 babies per woman in 2007 to 1.86 two years ago — below the replacement rate. His summation: “Sometime in the next one to three years the wheels come off” the markets and the economy because of lousy monetary policy, excessive debt and regulation, poor demographics, too many retirees, poor productivity, and a host of other problems.

Here's something you might be interested in.

Local money men Robert Snigaroff, Neil Hokanson, Ross Starr bearish on future

Warning: “wheels come off” the economy within next three years

Local money men Robert Snigaroff, Neil Hokanson, Ross Starr bearish on future

Warning: “wheels come off” the economy within next three years

Where should you invest your money these days? A savings account? You will get almost nothing in interest returns. Bonds? Same problem. Stocks? They soared after the Great Recession ended in early 2009, but the economy has been weak. So even long-term bulls admit stocks are awfully expensive relative to their earnings and prospects. Real estate? Same problem: it’s expensive almost everywhere.

Neil Hokanson

“There is no cheap asset class,” says Neil Hokanson, principal of the Solana Beach office of Aspiriant, a money-management firm. “There is no low-hanging fruit. We just can’t stomach these low yields. It’s a horrible time in terms of finding something really attractive.” He tells his clients to be patient — invest slowly and keep a lot of money in low-yielding money market funds and the like (often called “cash”).

A. Gary Shilling

New Jersey–based economist A. Gary Shilling is widely followed these days because back in 1981 he predicted the “bond rally of a lifetime.” Many thought he was nuts. At the time, long-term bonds were yielding 15 percent. Recently the 30-year Treasury bond has been yielding around a mere 2.3 percent. Because bond prices rise as interest rates go down, Shilling is considered a prophet. Now, he feels United States rates will go even lower, so he is still buying 30-year Treasury bonds, but he admits that this strategy is not suitable for investors who need income.

30-Year-Treasury Bond Prices

Noting that banks in Europe and Japan are paying negative interest rates, he believes rates in the United States could go lower from current levels, although he is not ready to call negative interest rates in the U.S., since negative rates are not boosting economies that try them overseas. “Chronic deflation [prices declining] is increasingly likely,” he says. He would bet that American stocks will drop (a process called “shorting”) and would bet that oil will go even further down from its current level, perhaps as low as $10 to $20 a barrel, as other commodities tumble, too.

So, except for 30-year Treasury bonds, he basically agrees with Hokanson: no potential investment is a sure thing these days. Hokanson disagrees with Shilling on bonds: “After inflation and after taxes, the returns are negative,” he says.

Robert Snigaroff, Mike Stolper, and Neil Hokanson

Robert Snigaroff, president of San Diego’s Denali Advisors, says those claiming that stocks are too expensive are wrong. “Stocks are not outrageously priced, given the low interest rates,” he says. With bonds and savings accounts paying such puny returns, stock+s may be the answer. Money from around the world has been poured into utilities and high-yielding, blue-chip telecoms, such as AT&T and Verizon. Snigaroff, however, is not so bullish on utilities and telecoms: too much money has already been poured into them. Denali doesn’t go fishing for bonds, but Snigaroff thinks it is possible that Shilling may be right: they can rise further.

Ross Starr

Ross Starr, professor of economics at the University of California San Diego, warns of risks in Shilling’s strategy. “Since interest rates are at historic lows, the best guess is that rates will go up within a decade, and when that happens, the market value of existing bonds goes down, so for a conservative investor what looks like a safe bet, the 30-year Treasury bond, looks risky if the investor cashes out before the bond matures. However, it is safe if you don’t cash out.”

Starr says the “really safe” investment is inflation-protected Treasury bonds, called TIPS. “They are also safe in the unlikely event of persistent deflation.” (However, others point out that TIPS can produce tax headaches in some instances, and you can lose if you sell before the bond matures.)

Although he thinks interest rates could go up, he says tax-free California municipal bonds can be attractive. Also, “a portfolio of junk bonds [low-quality, high-yielding bonds] could provide handsome returns.” And what about Shilling’s strategy of buying long-term Treasury bonds? Starr thinks they are “in a bit of a bubble.”

Starr says stocks compared to U.S. Treasury paper are not overpriced, but compared with historic statistical measures they are overpriced. “There is no return without risk,” says Starr. “The conventional portfolio for an investor with a long horizon is an even mix of common stocks and fixed income [bonds].”

Carlsbad’s James Welsh writes a publication, Macro Tides, as well as a weekly technical market/economic review. Today, investors “are assuming more risk than the potential reward” merits, says Welsh. “Nothing looks that good.” Interest rates in the United States can’t go down much more: “We’re getting close to the end of the road” on bonds.

Stocks don’t look so hot, either. The U.S. stock market “is the third-most expensive in the last 100 years,” he says. Sobering, that. Indeed, “In the next month or two, the market will pull back 3 to 7 percent,” he says. Of course, that would be what’s called a “correction.” In bear markets, stocks go down 20 percent or more. The bear visits every 3.4 years, and the average decline in the last 25 bears, dating to 1929, is 35.43 percent. That means for the average investor, a dollar in stocks turns into 64.6 cents. But bull markets arise out of bears, and over time, stock investments have been as good as anything, but you have to have a strong stomach for the roller-coaster rides.

Welsh thinks valuations for the stocks that have done best in this market, telecoms and utilities, are on the high side. Generally, he would wait until the correction takes its bite before jumping back in. “It’s time for a breather,” says Welsh.

He blames the negative interest-rate policies in Europe and Japan for much of the current problems. Negative rates caused the market valuation of European banks to plummet. Those banks are in trouble: “There is $1 trillion of nonperforming loans throughout the European banking system, and one-third of that is in Italy,” which is really in sick bay. The negative interest rates have not helped economies and have caused people to lose confidence in central banks.

Demographics are not positive. The fertility rate has fallen from 2.12 babies per woman in 2007 to 1.86 two years ago — below the replacement rate. His summation: “Sometime in the next one to three years the wheels come off” the markets and the economy because of lousy monetary policy, excessive debt and regulation, poor demographics, too many retirees, poor productivity, and a host of other problems.

Comments